Professional Credit Repair for Business Owners: A Strategic Guide to Capital Access in 2026

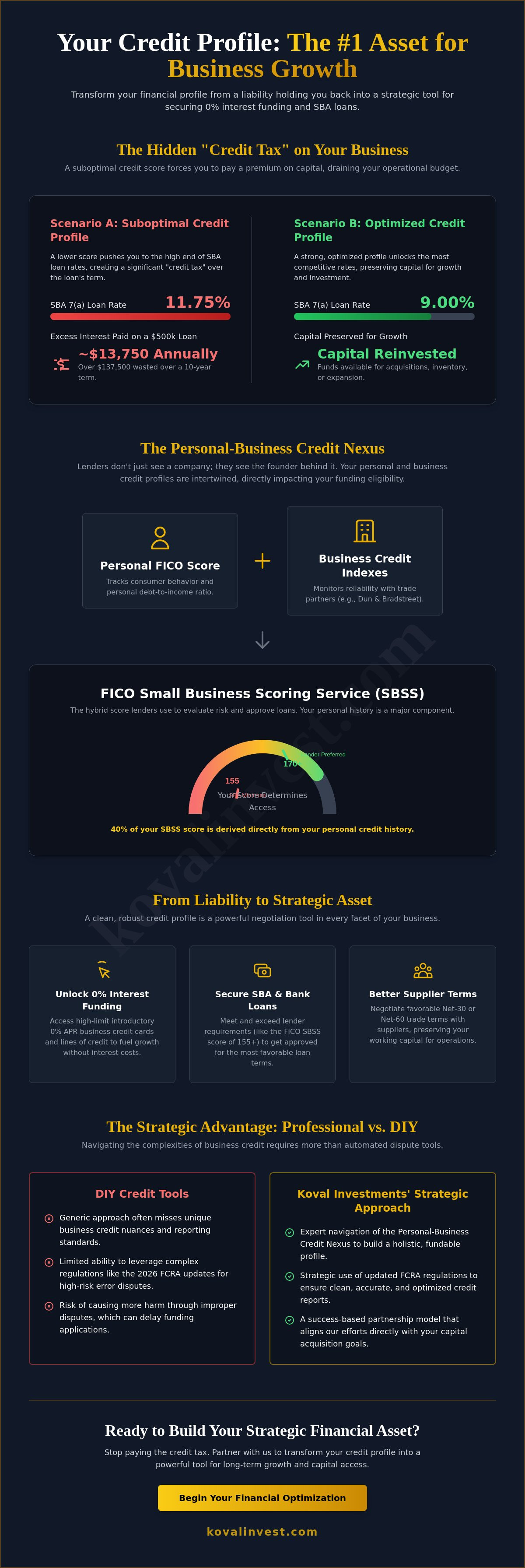

What if the 11.75% interest rate on your current capital isn't a market reality, but a "credit tax" you're paying for a profile that doesn't reflect your true business potential? Many entrepreneurs find themselves stuck with high rates or outright loan denials despite having strong revenue, often because they haven't prioritized credit repair for business owners as a core growth strategy. With the SBA requiring a minimum FICO SBSS score of 155 for most applications, your personal financial health is directly linked to your ability to scale.

It's frustrating to watch high interest rates eat into your margins while you navigate the confusing overlap between your personal and business scores. We believe your financial profile should be a powerful tool for securing 0% interest funding and SBA loans rather than a liability. In this guide, you'll discover how to leverage the 2026 FCRA updates to clean up your record and build a profile that banks trust. We outline a logical, step-by-step approach to transform your credit from a roadblock into a strategic asset for long-term capital access.

Key Takeaways

- Learn why viewing your credit profile as a primary business asset can significantly improve your company's valuation and lower your long-term cost of capital.

- Understand the "Personal-Business Nexus" and how professional credit repair for business owners bridges the gap between personal FICO scores and business indexes like Dun & Bradstreet.

- Identify the specific credit benchmarks required to unlock high-limit 0% interest funding solutions and secure approval for SBA loans.

- Evaluate the strategic limitations of DIY credit tools when navigating the unique complexities and reporting standards of business credit bureaus.

- Discover how a success-based partnership model aligns credit restoration efforts with your specific objectives for capital acquisition and strategic growth.

Beyond the Score: Why Strategic Credit Repair is a Business Necessity

Many entrepreneurs view their credit score as a personal metric, similar to a health checkup or a driving record. This perspective is outdated. In a professional context, your credit profile functions as a primary business asset. It is the foundation upon which you build leverage. As we move through 2026, the lending environment has shifted toward extreme precision. With the 2026 FCRA updates mandating a 10-day preliminary investigation for high-risk errors and higher verification standards, lenders now expect a flawless financial narrative. Strategic credit repair for business owners isn't just about fixing past mistakes; it's about "Financial Optimization." This approach treats your credit report as a living document that determines your access to the 0% interest funding solutions and SBA loans that fuel expansion. It's the difference between being a passive participant in the economy and being a proactive strategist.

The Hidden Cost of Suboptimal Credit

The financial impact of a mediocre credit score is often invisible until you calculate the interest rate spread. For instance, as of May 2026, variable rates for SBA 7(a) loans range from 9.00% to 11.75%. A founder with a slightly lower score might be pushed toward the higher end of that bracket. On a $500,000 loan, a 2.75% difference results in thousands of dollars in excess interest every year. Over a ten-year term, this "credit tax" can drain your operational budget. Beyond the direct cost, poor credit creates a friction point that causes funding delays. These delays often mean missing out on time-sensitive acquisitions or bulk inventory buys that could have secured your market position. Even your vendor relationships suffer. Suppliers are less likely to offer favorable net-30 or net-60 trade terms if they perceive risk in your profile, forcing you to use cash that should be earmarked for growth.

Credit as a Lever for Strategic Growth

A clean credit profile does more than just lower your borrowing costs. It serves as a powerful negotiation tool in every facet of your operations. When you approach suppliers with a strong financial standing, you gain the upper hand in requesting better trade terms, which preserves your working capital. This is particularly vital for those pursuing mergers and acquisitions. In these scenarios, the owner's credit health is often factored into the overall business valuation. A tarnished record can lead to a lower purchase price or more restrictive "earn-out" clauses that limit your exit potential. By understanding the credit repair process, you can begin treating your credit report like a corporate balance sheet. This mindset shift ensures that when a growth opportunity arises, your financial profile is ready to act as a catalyst rather than a hurdle. At Koval Investments, we see this as the first step in a collaborative partnership designed to maximize your long-term success through a success-based philosophy.

The Personal-Business Credit Nexus: Solving the Founder’s Funding Dilemma

Banks don't just lend to companies; they lend to the people who lead them. This reality creates what we call the "Personal-Business Credit Nexus." For most entrepreneurs, the business and the individual are financially inseparable in the eyes of a lender. While you might focus on your company's revenue, a bank uses your personal credit history as a proxy for your business's reliability. This is why credit repair for business owners is a vital step even for established firms. Personal FICO scores track your consumer behavior, while business indexes like Dun & Bradstreet (D-U-N-S) monitor your reliability with trade partners. If your personal debt-to-income (DTI) ratio is too high, it acts as a bottleneck, capping your business funding limits regardless of your company's cash flow. Even as your business grows, the "personal guarantee" remains a standard requirement, making the founder’s profile the permanent anchor of the company's financial reach.

Understanding the Hybrid Credit Model

Lenders often use the FICO Small Business Scoring Service (SBSS) to evaluate applications. The SBA requires a minimum FICO SBSS score of 155 for 7(a) loans under $350,000, though many preferred lenders look for scores closer to 170. This score is a hybrid. It's composed of your personal credit history (40%), business credit history (25%), time in business (15%), and your revenue or assets (20%). High personal credit utilization can drag down this score, signaling to banks that you're over-leveraged. The FICO SBSS score acts as the bridge between personal and business financial health. If you're struggling to secure the capital you need, our Credit Repair Services can help align your personal profile with your corporate goals.

Strategies for Decoupling and Protection

Building a business credit profile that stands on its own requires a methodical approach. You should start by securing an EIN and a D-U-N-S number, then following the SBA guidelines on business credit to establish trade lines with vendors who report to business bureaus. It's essential to separate personal and business expenses strictly. Co-mingling funds is a major red flag for lenders and can lead to lower funding approvals. Professional credit repair for business owners protects your personal assets by ensuring that inaccuracies or old consumer debts don't bleed into your business evaluations. This separation creates a layer of protection, allowing your business to eventually access capital based on its own merit rather than just your personal signature. This transition is a key part of our collaborative approach to your long-term growth.

From Disputes to Dollars: How Credit Optimization Unlocks 0% Interest and SBA Loans

Credit repair for business owners is often misunderstood as a defensive reaction to past errors. In reality, it's the offensive pre-qualification phase of capital procurement. If you treat this process as a strategic prerequisite, you transform your financial profile into a tool that qualifies you for elite funding vehicles. At Koval Investments, we focus on moving you from a "denied" status to an "approved" status by aligning your profile with the specific risk benchmarks used by institutional lenders. This isn't just about removing late payments; it's about optimizing every data point to ensure your application meets the highest standards of scrutiny. When your profile is clean, you aren't just asking for money; you're presenting a low-risk opportunity to the bank.

Qualifying for 0% Interest Funding

Our 0% Interest Funding Solution is a prime example of why score optimization matters. To access unsecured, interest-free capital, lenders typically look for a personal FICO score of 700 or higher. High-impact negative items, such as public records or recent collections, can result in an immediate hard decline. By removing these obstacles, you open the door to business lines of credit that offer zero interest for introductory periods, often lasting 12 to 22 months. This period of "credit seasoning" allows your business to leverage funds for growth without the immediate burden of interest payments. It's a powerful way to manage cash flow while your revenue scales to meet new demands.

Navigating SBA Loan Requirements

SBA loans require an even higher level of transparency than standard commercial products. While traditional banks might overlook a minor dispute, the SBA is highly sensitive to "character" issues and old discrepancies. An unresolved error or a poorly documented dispute can trigger an automatic rejection during the underwriting process. Professional consulting helps you identify these red flags before you submit your package. You can find more details in this comprehensive guide to repairing company credit, which outlines the technical steps of report cleanup. When your credit health is synchronized with an accurate business valuation, your SBA 7(a) application becomes significantly more compelling. This synergy ensures you're positioned to secure the 5.50% to 6.50% fixed rates currently available for the CDC portion of 504 loans, rather than settling for high-interest alternatives.

Professional Credit Restoration vs. DIY: A Cost-Benefit Analysis for Entrepreneurs

You've likely seen advertisements for apps that promise to fix your credit with a few clicks. For a busy entrepreneur, the DIY route seems tempting, but credit repair for business owners involves complexities that standard consumer software isn't designed to handle. While consumer bureaus are regulated by strict frameworks, business credit bureaus like Experian Business and Equifax Commercial operate under different standards. Automated templates often trigger "frivolous" dispute tags. These tags can lead to a credit bureau ignoring your request entirely, potentially setting your funding timeline back by months. An expert partner provides more than just administrative help; they offer a perspective aligned with what lenders actually want to see in a funding application.

The Complexity of the Dispute Process

Business credit bureaus are notoriously harder to correct than consumer ones. They don't always follow the same dispute resolution paths, and the data they collect is often more fragmented. The legal nuances of the Fair Credit Reporting Act (FCRA) as it applies to business owners have become even more rigorous in 2026. New standards require higher levels of verification for disputed information, meaning a simple "this isn't mine" letter is no longer sufficient. Professional firms have established relationships and protocols that DIY software lacks. We understand the specific language and documentation required to meet these higher verification standards without triggering automated rejections from AI-powered reporting systems.

Time as a Non-Renewable Business Asset

Your time is a non-renewable asset. If you calculate your "Founder Hourly Rate," the cost of managing your own credit restoration often far exceeds the price of a professional service. Spending dozens of hours researching bureau protocols and tracking correspondence is a distraction from your core mission: growing your company. A hands-off approach allows you to remain focused on operations and strategic planning while experts handle the technical heavy lifting. At Koval Investments, our success-based philosophy removes the financial risk of outsourcing. We act as a strategic partner, meaning we're equally invested in your success. If you're ready to stop managing paperwork and start securing capital, explore our Credit Repair Services today. This collaborative model ensures that your financial profile is optimized for the 0% interest funding and SBA loans discussed in previous sections.

Partnering for Growth: The Koval Investments Approach to Success-Based Credit Repair

At Koval Investments, we don't view ourselves as a distant service provider or a high-volume processing center. We operate as a seasoned strategic partner and a trusted advisor to entrepreneurs who are serious about scaling. Our firm understands that your time is better spent on operational efficiency than on tracking bureau correspondence. This is why our philosophy centers on a collaborative venture where our goals are perfectly aligned with yours. We aren't just here to fix numbers on a screen; we're here to ensure your financial profile is a precision-engineered tool ready for the capital markets. Credit repair for business owners is the foundational step in this journey, but it's only the beginning of our engagement.

The defining characteristic of our work is the success-based model. We believe in a "win-win" philosophy that removes the traditional financial risk from our clients. By aligning our incentives with your results, we reinforce our confidence in our ability to deliver tangible value. This approach creates a low-pressure, supportive environment where the focus remains entirely on the outcome. Our clients appreciate this "straight-talk" mentality because it builds trust through transparency and accountability. We don't use aggressive sales tactics. Instead, we offer a steady hand to help you navigate the complex financial landscapes of 2026, ensuring you're positioned to leverage every available opportunity.

A Holistic Financial Suite

Our expertise extends far beyond simple restoration. We offer a holistic suite of services that includes Business Valuations, Strategic Planning, and Mergers and Acquisitions Consulting. When we optimize your credit, we're often doing so with an eye toward a larger transaction. For example, a clean credit profile can significantly impact a business valuation during an acquisition or merger, as it demonstrates a history of fiscal responsibility and lowers the risk for the incoming party. This "insider" advantage allows us to bridge the gap between high-level strategy and day-to-day operational constraints. We ensure that your credit health supports your broader objectives, whether that's securing Working Capital or pursuing Real Estate Investment Funding.

Your Path to Funding Starts Here

The roadmap from your initial analysis to final funding is methodical and logical. During your initial consultation, we conduct a deep dive into your specific goals. We don't just look at your score; we look at the capital you need to reach your next milestone. This thorough comprehension allows us to build a tailored strategy that leads directly to our 0% Interest Funding Solution or SBA Loans. You can expect a process defined by integrity and forward-thinking expertise. We value the quality of our relationships over the volume of our transactions, ensuring that every client receives the personalized attention they deserve. Schedule your strategic credit analysis with Koval Investments today.

Turning Your Financial Profile into a Growth Engine

Your financial profile is more than a collection of scores; it's the engine that powers your company's expansion. By treating credit repair for business owners as a proactive growth strategy, you move beyond mere cleanup and into the realm of capital optimization. We've discussed how a clean record facilitates access to SBA loans and 0% interest funding, providing the liquidity needed for inventory, acquisitions, or real estate. It's about ensuring your business doesn't pay a "credit tax" through high interest rates that eat into your margins.

At Koval Investments, we bring a steady hand to this process. Our success-based philosophy ensures that our interests are perfectly aligned with your results. We combine deep expertise in funding solutions with a strategic partner approach that covers everything from business valuations to M&A consulting. This isn't just about fixing the past; it's about engineering a future where capital is never a constraint. If you're ready to transform your profile from a liability into a high-leverage asset, we're here to navigate the complexities alongside you.

Secure Your Strategic Funding Analysis

Your next phase of growth is within reach once you have the right financial foundation in place.

Frequently Asked Questions

How long does credit repair for business owners typically take?

The timeline for results varies based on the complexity of your file, but most entrepreneurs see significant movement within 90 to 180 days. While the 2026 FCRA updates mandate a 10-day preliminary investigation for high-risk errors, the full process of verification and updating bureau records requires a methodical approach. We focus on a steady progression to ensure that changes are permanent and recognized by lenders during your funding application.

Will fixing my personal credit really help my business get an SBA loan?

Yes, your personal credit is a critical factor because it accounts for 40% of the FICO SBSS score used for SBA 7(a) loans under $350,000. Most preferred lenders require a score between 160 and 170 to move forward. By addressing personal derogatories, you strengthen the "character" portion of the SBA's evaluation, which is often the deciding factor in a loan approval or denial.

What is the difference between business credit repair and personal credit repair?

Personal credit repair focuses on consumer bureaus like Equifax and TransUnion under the protections of the FCRA. Business credit repair targets commercial entities like Dun & Bradstreet and Experian Business, which use different scoring models like the PAYDEX score. The dispute protocols for business bureaus are often more complex and don't always follow the same automated paths as consumer reporting.

Can I still get 0% interest funding if I have a bankruptcy on my record?

Securing 0% interest funding with a bankruptcy is challenging but depends heavily on the age of the discharge and your current score. Most interest-free business lines of credit require a 700+ FICO score and a clean record for at least several years. If your bankruptcy is older, professional credit repair for business owners can help optimize the rest of your profile to offset the impact of that legacy item.

How much does professional credit repair for business owners cost?

Fees for professional restoration are typically structured based on the depth of the analysis required and the number of items being addressed. Every business owner's situation is unique, so costs reflect the specific strategic path needed to reach your funding goals. We operate on a success-based philosophy, which ensures our incentives are aligned with your actual results rather than just the volume of disputes sent.

Does credit repair guarantee that I will get a business loan?

No service can legally guarantee a loan approval because lenders also evaluate your revenue, time in business, and industry risk. Credit repair optimizes your profile to ensure you meet the minimum creditworthiness thresholds required by banks. It removes the "credit roadblocks" that cause automatic denials, allowing the lender to focus on the strength of your actual business operations.

What are common errors found on business credit reports?

Inaccuracies often include debt that belongs to a business with a similar name, outdated tax liens that have already been satisfied, or missing trade lines that should be boosting your score. Because business data is often manually entered by vendors, the error rate can be higher than in consumer reporting. These mistakes can lead to lower credit limits or higher interest rates if they aren't caught and corrected.

Is business credit repair legal under the Fair Credit Reporting Act?

Yes, you have a legal right to dispute any information on your credit report that is inaccurate, unfair, or unsubstantiated. The Credit Repair Organizations Act (CROA) provides the federal framework that governs how these services must operate. This ensures that you're protected from deceptive practices while you work to ensure your financial profile accurately reflects your true creditworthiness.