The Ultimate Guide to 0% Interest Business Funding in 2026

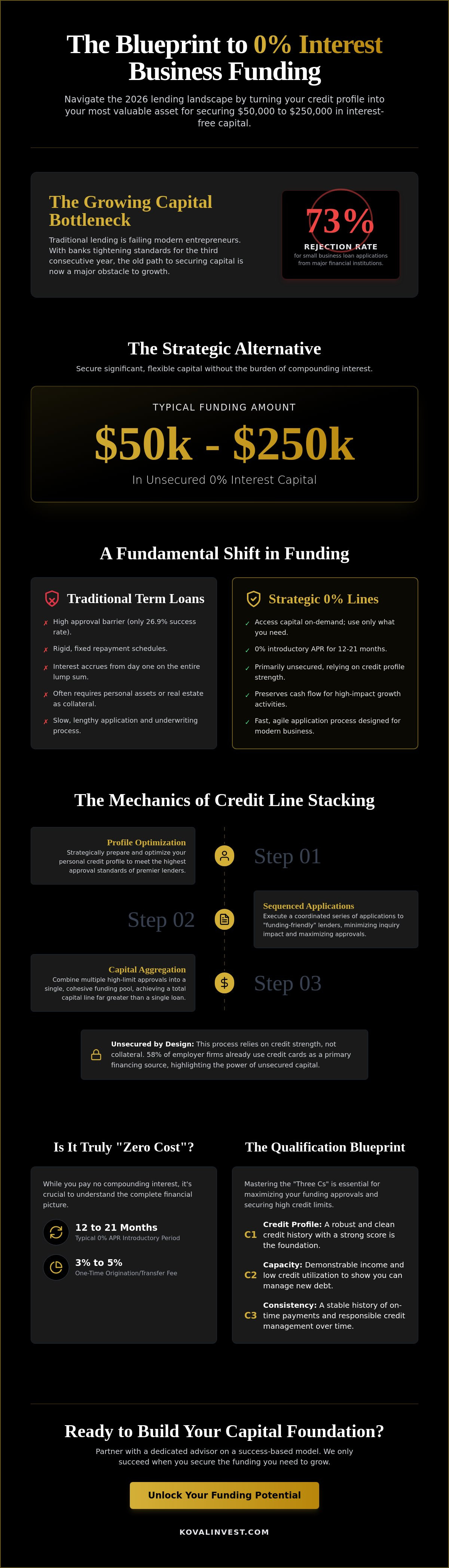

With major financial institutions now rejecting over 73% of small business loan applications, the traditional path to capital has become a bottleneck for growth. It's frustrating to watch high interest rates eat into your hard-earned margins while banks tighten their standards for the third consecutive year. You've likely realized that the old way of securing capital doesn't work for modern entrepreneurs who need agility and cost-efficiency.

We believe that 0% interest business funding isn't a rare stroke of luck; it's the result of a deliberate, professional strategy. You can secure between $50,000 and $250,000 in interest-free capital by optimizing your credit profile and leveraging strategic funding frameworks. This guide provides a clear path to qualify and explains how to navigate the complexities of credit stacking. We'll explore the current 2026 lending environment and show you exactly how to build a capital foundation that supports your long-term success. By the end, you'll understand how to turn your credit profile into your most valuable business asset.

Key Takeaways

- Understand the fundamental shift from traditional term loans to strategic revolving lines as a tool for sustainable business growth.

- Learn the sophisticated mechanics of credit line stacking to maximize your total aggregate 0% interest business funding through precise application sequencing.

- Identify the reality of origination fees versus long-term interest costs to gain complete transparency over your capital structure.

- Master the "Three Cs" of qualification to ensure your personal credit profile is optimized for high-limit approvals.

- Discover how a success-based partnership model aligns your funding objectives with a dedicated advisor focused on tangible results.

The Landscape of 0% Interest Business Funding in 2026

In 2026, the financial environment for entrepreneurs has shifted significantly. As traditional banks continue to tighten their lending standards, 0% interest business funding has evolved from a niche perk into a sophisticated strategic capital tool. Unlike a standard loan where you receive a lump sum and pay it back with fixed interest, this strategy focuses on revolving access. It allows business owners to draw what they need, pay it back, and reuse the capital without the burden of compounding interest. This flexibility is vital in a market where cash flow has surpassed inflation as the top concern for 31% of small business owners.

A key distinction lies in the difference between traditional term loans and a 0% line of credit. Term loans often come with rigid repayment schedules and interest rates that start the moment the funds hit your account. In contrast, 0% revolving lines provide a safety net where you only pay for what you use. With major financial institutions currently approving only about 26.9% of small business loan applications, these interest-free structures have become essential for maintaining operational agility. Primary sources for this capital now include a mix of forward-thinking regional banks, fintech innovators, and private credit optimization firms that specialize in credit stacking.

Why Traditional Banks Rarely Offer 0% APR

The primary reason you won't find a 0% interest rate on a standard bank loan is the profit motive. Banks thrive on the spread between what they pay for money and what they charge you. However, many institutions have shifted toward offering introductory 0% periods as a customer acquisition tool. They're often willing to waive interest for 12 to 21 months to secure a long-term relationship. It's vital to distinguish between 0% interest and 0% APR. While 0% interest means no cost for the money borrowed, 0% APR includes the total cost of credit, including any potential origination or balance transfer fees which typically range from 3% to 5%.

The Strategic Advantage of Interest-Free Capital

Accessing 0% interest business funding provides a profound competitive edge. It allows you to preserve cash flow for high-impact activities like R&D or marketing without the drag of monthly interest payments. We often see clients use these funds as a bridge for real estate earnest money or to secure inventory during peak seasons. There's also a significant psychological benefit; growing your company without accumulating high-interest debt reduces the pressure on your bottom line. It creates a collaborative scenario where you can scale aggressively while keeping your margins intact. This methodical approach to capital ensures that your growth is both sustainable and intentional.

The Mechanics of Business Credit Line Stacking

Credit line stacking is often misunderstood as a simple series of credit applications. In reality, it's a sophisticated financial framework designed to maximize capital access while protecting your credit health. Credit line stacking is a professional procurement method that involves coordinating the timing and sequence of applications to secure high-limit capital before new inquiries or balances impact your overall profile. This strategy allows you to aggregate multiple approvals into a single, cohesive funding pool, often totaling between $50,000 and $250,000.

The true power of this approach lies in its unsecured nature. Unlike traditional bank loans or SBA products that may require equipment, real estate, or personal assets as collateral, 0% interest business funding through stacking relies on the strength of your credit profile. This lack of collateral requirements makes it a preferred choice for 58% of employer firms that already utilize credit cards as their primary financing source. By removing the need for asset-based security, you maintain total control over your business operations while gaining the liquidity needed to scale.

How Stacking Works for Unsecured Funding

The process begins by identifying "funding-friendly" lenders that do not report activity to personal credit bureaus. This is a critical step; if these high-limit lines appeared on your personal report, your debt-to-income ratio would spike, potentially lowering your scores. To execute this correctly, you must first establish business credit that is distinct from your personal identity. We focus on a specific "Inquiry Strategy" where applications are grouped to minimize the visibility of recent credit-seeking behavior. This methodical approach ensures that each lender views your profile in its most favorable light, leading to higher aggregate approvals.

The Role of 0% Introductory APR Periods

Most 0% interest business funding strategies leverage introductory windows that last between 12 and 21 months. These periods offer a unique opportunity to use "free" money for high-ROI activities like inventory purchases or marketing campaigns. However, you must have a clear exit strategy. Once the introductory period ends, variable APRs typically jump to a range of 16.74% to 28.49%. Professional consultants manage this transition by planning for a "rollover" of capital. This might involve strategic refinancing or consolidating balances using transfer offers, which often carry a modest 3% to 5% fee. If the complexity of managing these timelines seems daunting, you might benefit from a strategic funding partner who handles the sequencing and maintenance for you. This ensures you never get trapped by high post-introductory rates, keeping your growth sustainable and interest-free for the long term.

Debunking the Myths: Is Zero-Interest Funding Too Good to be True?

Skepticism is a natural response to the phrase "interest-free money." Most entrepreneurs assume there's a hidden catch designed to trap them in debt. In reality, 0% interest business funding is a calculated customer acquisition strategy used by major lenders. Banks aren't being charitable; they're data mining. They're willing to waive interest for a set period to acquire high-quality business clients who will eventually utilize other profitable services over a multi-year relationship.

It's essential to look at the total cost of capital rather than just the interest rate. A traditional term loan with a 10% interest rate over two years is significantly more expensive than a revolving line with a one-time 3% procurement fee. When you calculate the math, the upfront fee is a fraction of the compounding interest costs of a standard loan. However, you must be vigilant about "deferred interest" traps. Some predatory offers backdate interest to the original purchase date if the balance isn't cleared by the deadline. We help our partners avoid these pitfalls by selecting transparent, business-grade products that don't include these hidden anchors.

The Risks of DIY Funding Without Expert Oversight

Many founders attempt a "DIY" approach by applying for several accounts at once. This "shotgunning" method almost always backfires. Each application triggers a hard inquiry, and without proper sequencing, your score can drop by 100 points in a single afternoon. Lenders also watch for "max-out" signals on personal credit, which can lead to immediate rejections or drastically reduced limits. This is where the value of a partner becomes clear.

Professional oversight changes the equation entirely. By integrating strategic planning and business valuations into the procurement process, we present a profile of stability to the banks. We treat capital acquisition as a surgical operation rather than a game of chance. This methodical approach ensures you don't just get funded, but that you stay fundable as your business scales. Taking the DIY route might seem like a way to save money, but the cost of a damaged credit profile far outweighs the investment in professional guidance.

The Qualification Blueprint: Preparing Your Business for 0% Capital

Securing high-limit capital requires more than just a registered entity. It demands a specific alignment of three core pillars: Credit, Capacity, and Character. While traditional banks often require three years of tax returns and heavy collateral, the criteria for 0% interest business funding are more focused on the individual behind the business. You don't need a decades-old enterprise to qualify, but you do need a profile that signals low risk to institutional lenders. This shift in focus is why many founders find success with us after being rejected by traditional institutions.

Your personal credit report is the ultimate gatekeeper. In the world of unsecured funding, lenders view your personal financial behavior as the best predictor of how you'll manage business lines. This means inaccuracies, late payments, or high personal utilization can act as immediate "funding killers." Disputing errors and cleaning up your report isn't just about the score; it's about presenting a narrative of reliability. Most founders are surprised to learn that they don't need complex financial documentation like profit and loss statements for many of these products, provided their credit profile is pristine.

The Critical Intersection of Personal and Business Credit

Leveraging a FICO score of 700 or higher is the most effective way to secure $100,000 or more in interest-free business lines. If your score is currently below this threshold, the first step is optimization. This involves Mastering Business Credit Repair to remove obstacles that prevent high-limit approvals. By addressing these issues early, you position yourself to access capital that doesn't report to your personal credit, keeping your individual scores high even as you scale your business operations. This separation is vital for protecting your long-term borrowing power.

Essential Documentation and Financial Benchmarks

Beyond the score, your business must be structured for maximum "lendability." This starts with a clean legal setup. Lenders look for a formal LLC or Corporation with a professional business address and a dedicated phone line. Using a home address or a personal mobile number can trigger fraud alerts or signal a lack of stability to automated underwriting systems. We also find that incorporating strategic planning and business valuations into your application package significantly increases lender trust. It shows that you have a clear roadmap for the capital, which encourages banks to offer higher limits. If you're ready to see where your business stands, you can start your qualification assessment today to identify any gaps in your profile before you apply.

Securing Your Capital with Koval Investments’ Success-Based Model

Automated fintech platforms like Stripe or Square often provide capital based strictly on sales volume. While convenient, these systems are inherently inflexible. If your business doesn't fit their narrow algorithmic boxes, you're left without options. Koval Investments offers a more personalized, boutique experience that prioritizes your specific objectives over automated data points. We provide a comprehensive suite of services that spans from initial credit restoration to final capital procurement, ensuring every obstacle to your funding is removed.

Our firm operates on a fundamentally different principle than traditional lenders. We believe in a success-based model where our interests are directly tied to your results. This "win-win" philosophy means we only succeed when you get funded. It's a supportive, low-pressure approach that transforms the traditional client-provider dynamic into a true partnership. We don't just provide a service; we act as a steady hand to help you manage complex financial landscapes with confidence and clarity.

Our Strategic Approach to Procurement

We don't believe in one-size-fits-all solutions. A real estate investor looking for earnest money requires a different strategy than a SaaS founder scaling their engineering team. We develop customized funding roadmaps that reflect these industry realities. Our "insider" advantage comes from a deep network of funding-friendly lenders who specialize in high-limit, unsecured lines. Koval manages the entire application lifecycle, handling the administrative complexity so you can focus on running your business. This ensures that your 0% interest business funding is secured through a methodical, professional process rather than a game of chance.

Beyond Funding: Long-Term Growth and Advisory

Our partnership doesn't end once the capital hits your account. We view 0% interest funding as the first step in a broader strategic journey. For businesses looking for permanent, long-term financing, we provide expert assistance with SBA loans. If you're ready to scale aggressively, our M&A consulting and strategic planning services help you use your interest-free capital to acquire competitors or expand into new markets. We bridge the gap between high-level strategy and daily operations, ensuring your capital is always working toward your ultimate goals. Apply for your 0% funding strategy session today to start building your customized capital roadmap.

Empowering Your Next Phase of Strategic Growth

Securing capital shouldn't be a source of stress or a gamble with your company's future. You've seen that 0% interest business funding is a sophisticated financial framework that rewards those with an optimized credit profile and a clear roadmap. By separating your personal and business credit identities and utilizing professional line stacking, you can access the liquidity needed to scale without the anchor of compounding interest rates.

We specialize in navigating these complexities alongside you. From initial credit restoration to final capital procurement, our team manages the entire process to ensure you get the best possible terms. Our success-based model eliminates upfront risk because we believe our relationship should be a collaborative venture where we only succeed when you get funded. Whether you're bridging a gap for real estate or seeking strategic advisory for M&A and long-term growth, we provide the steady guidance your business deserves.

Secure Your 0% Interest Funding Roadmap with Koval Investments

Your vision for expansion is achievable when you have the right capital and a trusted partner by your side. We're ready to help you turn your ambitions into a tangible, debt-free reality.

Frequently Asked Questions

Is 0% interest business funding actually real or just a marketing gimmick?

Yes, it is a legitimate financial tool used by major lenders to acquire high-quality business clients. These offers are primarily introductory APR periods on business credit lines. Banks use these periods as a customer acquisition strategy, betting that the long-term relationship will be profitable through other services or post-introductory interest. It's a calculated move by the bank, not a gimmick.

How much 0% interest capital can my business realistically qualify for?

Most businesses qualify for between $50,000 and $250,000 in aggregate funding through a strategic stacking approach. The final amount depends heavily on the strength of your credit profile and the number of lenders we can sequence in a single funding round. While individual limits vary, our goal is to maximize your total liquidity while maintaining a sustainable debt-to-income ratio.

Do I need a high personal credit score to get 0% business funding?

A personal credit score of 700 or higher is typically required to access the most competitive high-limit offers. Since these are unsecured lines, lenders use your personal FICO score as a benchmark for your financial reliability. If your score is currently lower, we often begin with credit repair services to optimize your profile before initiating the funding applications to ensure the best possible approval odds.

What happens after the 0% introductory interest period expires?

Once the introductory period ends, the remaining balance is subject to variable APRs that typically range from 16.74% to 28.49%. We prepare our clients for this transition by helping them develop an exit strategy or a refinancing plan. This might involve moving the balance to a new 0% vehicle or utilizing permanent financing like an SBA loan to consolidate the debt at a lower fixed rate.

Are there any collateral requirements for 0% interest business lines?

No, the 0% interest business funding we help you secure is entirely unsecured, meaning you don't have to pledge personal or business assets. This protects your real estate, equipment, and inventory from being seized in the event of a business downturn. This lack of collateral is why these lines are so popular among entrepreneurs who want to scale quickly without risking their foundational assets.

How long does the 0% interest funding procurement process take?

The entire 0% interest business funding procurement process generally takes between three to five weeks from the initial consultation to the funds being available. This timeline allows for a thorough review of your credit profile, any necessary optimization, and the strategic sequencing of applications. We handle the administrative heavy lifting during this period to ensure the process moves as efficiently as possible without triggering red flags with lenders.

Can I use 0% interest funding for real estate investment down payments?

Yes, many investors use these interest-free lines as a bridge for earnest money or down payments on investment properties. Because the funds are revolving and unsecured, they provide the liquidity needed to move quickly on deals without waiting for traditional mortgage approvals. It's a common strategy for scaling a portfolio while keeping your cash reserves intact for operational expenses or renovations.

What is the difference between an SBA loan and 0% interest funding?

SBA loans are long-term, government-backed debt instruments with fixed or variable interest, while 0% funding focuses on short-term revolving credit lines. SBA loans often require extensive documentation and collateral, making them better suited for major acquisitions or permanent working capital. Our solutions provide faster access to capital with zero interest for the first 12 to 21 months, offering more flexibility for immediate growth.