Using Working Capital for Business Acquisition: A Strategic Guide for 2026

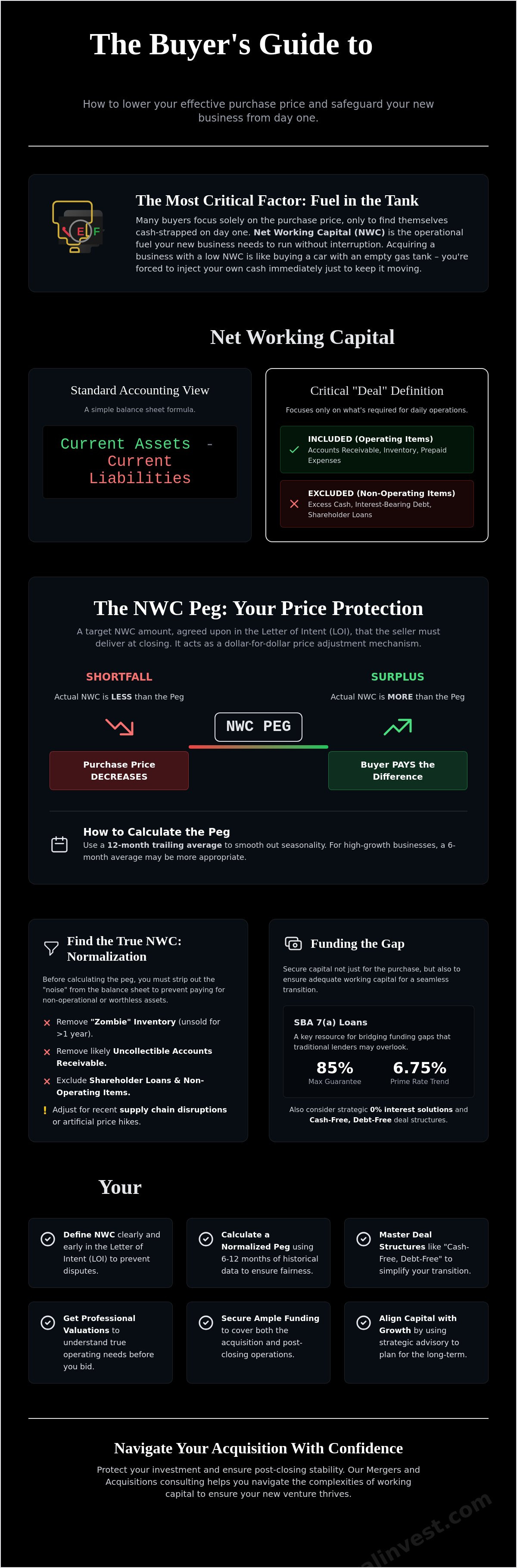

What if the most critical factor in your business acquisition isn't the purchase price, but the liquid fuel left in the tank on closing day? Many buyers spend months obsessing over valuation multiples only to find themselves cash-strapped because they didn't prioritize using working capital for business acquisition as a core strategy. It's a common fear; nobody wants to overpay due to hidden liabilities or lose sleep over post-closing cash flow. We understand that navigating these financial nuances requires a steady hand and a clear strategy.

This guide will show you how to master net working capital (NWC) adjustments to lower your effective purchase price and safeguard your operational stability. You'll learn how to identify reliable funding sources, such as SBA 7(a) loans, which currently offer up to 85% guarantees for smaller transactions in this rebounding 2026 market. We'll walk through the mechanics of the NWC peg, current interest rate trends like the 6.75% prime rate, and strategic ways to utilize 0% interest solutions to ensure your new venture thrives from the very first hour.

Key Takeaways

- Understand why Net Working Capital is the operational fuel that ensures your business remains a going concern from day one.

- Learn how to calculate a normalized NWC Peg to prevent overpaying and use it as a strategic lever during deal negotiations.

- Discover how using working capital for business acquisition through SBA 7(a) loans can bridge the funding gap that traditional lenders often overlook.

- Identify how professional business valuations and strategic planning before signing an Letter of Intent protect your cash flow and long-term investment.

- Master Cash-Free, Debt-Free deal structures to simplify your transition and align your capital procurement with future growth objectives.

The Strategic Role of Working Capital in Business Acquisitions

Net Working Capital (NWC) represents the liquid resources required to keep a business running without interruption. In the context of M&A, think of it as the fuel left in the tank when you take over the keys. If the tank is empty, you'll be forced to inject your own cash immediately just to keep the lights on. This is why using working capital for business acquisition effectively starts with a precise definition during the due diligence phase. It's not merely a balance sheet calculation; it's a fundamental component of the deal's value.

The standard accounting definition is simple: current assets minus current liabilities. However, the "deal" definition used in a transaction is far more nuanced. It focuses strictly on operating items, excluding interest-bearing debt and excess cash that isn't required for daily functions. This distinction is vital because it directly impacts your purchase price. Enterprise value assumes the business includes enough capital to operate normally. If the seller delivers less than that "normalized" amount, the equity value, which is the actual cash you pay the seller, should decrease accordingly to compensate for the shortfall.

Why Working Capital is Not Just "Extra Cash"

It's vital to distinguish between operating cash and excess cash. Operating cash is the minimum amount needed to fund daily transactions; excess cash is anything above that, which the seller usually retains. The core components of NWC in a deal include Accounts Receivable, Inventory, and Prepaid Expenses. Buyers expect a "normalized" level of these assets at closing. This means looking at a 12-month or 6-month average to account for seasonal spikes. Our Business Valuations often highlight these trends to ensure you don't inherit a business that's temporarily inflated or artificially depleted.

The Consequences of Mismanaging NWC Negotiations

Failing to define NWC in the Letter of Intent (LOI) often leads to purchase price erosion during the final hours of a deal. Without a clear "peg" or target, sellers might try to accelerate their collections or delay paying vendors right before the close to extract more cash for themselves. This leaves you with a starved business on Day 1. To ensure post-acquisition stability, you must negotiate clear terms that prevent these maneuvers. Using working capital for business acquisition planning ensures you have the liquidity needed to thrive immediately after the transition. At Koval Investments, we provide Mergers and Acquisitions Consulting to help you navigate these complexities, ensuring the capital structure aligns with your long-term strategic growth goals.

Calculating the Net Working Capital Peg: A Buyer’s Framework

Proactive buyers don't wait for the seller to define what is "normal" for the business. Establishing the Net Working Capital (NWC) peg early in the deal flow is a protective measure that defines the exact amount of liquidity the seller must deliver at closing. If the actual NWC at the time of the sale is higher than this target, the buyer pays more; if it is lower, the purchase price drops dollar-for-dollar. Successfully using working capital for business acquisition requires setting this target based on historical performance rather than a single point in time. This ensures you aren't inheriting a business that has been "hollowed out" of its necessary operating cash.

Most professionals utilize a 12-month trailing average to calculate this peg. This approach effectively smooths out seasonal fluctuations, such as inventory build-ups before a peak sales season or temporary lulls in accounts receivable. In high-growth industries where the business is significantly larger than it was a year ago, a 6-month average might be more appropriate to reflect the current scale. Our team provides specialized Mergers and Acquisitions Consulting to help you define these targets before you sign the LOI, ensuring your offer remains competitive yet grounded in reality.

Normalization: Adjusting for One-Time Events

Normalization is the process of stripping away "noise" from the balance sheet to find the true operating NWC. This involves removing non-operating items like shareholder loans or excess cash. In the current 2026 economic environment, you must also adjust for recent supply chain disruptions or sudden price hikes that might have artificially inflated inventory values. You should also look for "zombie" inventory that hasn't moved in over a year or accounts receivable that are likely uncollectible. These items should be excluded from the peg to prevent you from paying for assets that provide no real value to the going concern.

The Working Capital Adjustment Mechanism

The adjustment mechanism acts as a safety net. You propose the peg in the Letter of Intent (LOI) to set expectations early. Since the exact NWC on the closing date won't be known until weeks later, the deal includes a post-closing "true-up" period, typically lasting 60 to 90 days. During this time, both parties review the final closing balance sheet. If disagreements arise over the valuation of specific assets, the purchase agreement should outline a clear dispute resolution process, often involving an independent accounting firm. This methodical approach ensures a fair, win-win outcome where the final price accurately reflects the business's actual health on Day 1.

Using Working Capital as a Negotiation Lever

Negotiation in the 2026 M&A market often centers on the headline purchase price, yet the most sophisticated buyers recognize that the Net Working Capital (NWC) peg is their most effective tool for protecting value. Instead of viewing the NWC target as a static requirement, you should treat it as a strategic lever. For instance, if a seller is firm on a high valuation multiple, you might agree to that price only if they deliver a higher-than-average NWC peg. This strategy ensures the business remains well-capitalized on Day 1, effectively lowering your net cash outlay. Using working capital for business acquisition in this manner transforms a technical accounting requirement into a powerful mechanism for deal alignment.

Most mid-market transactions are structured on a "Cash-Free, Debt-Free" basis. This simplifies the capital structure by ensuring the seller keeps the cash and pays off all long-term debt before closing. However, the definition of "debt" is often where the best deal terms are won. Savvy buyers work with Mergers and Acquisitions Consulting experts to identify "debt-like" items that a seller might try to hide within working capital. By shifting these items out of NWC and into the debt category, you trigger a dollar-for-dollar reduction in the purchase price. A comprehensive Quality of Earnings (QofE) report is your primary weapon here, allowing you to challenge the seller’s claims with objective, normalized data.

Identifying Hidden Liabilities in Current Assets

Not all current assets are created equal. When using working capital for business acquisition, you must scrutinize the aging of receivables. Invoices older than 90 days are often uncollectible and should be discounted or removed from the peg entirely. Similarly, you should evaluate customer concentration risks. If a single client represents a significant portion of the receivables, any friction in that relationship threatens your post-close liquidity. Finally, perform a physical or digital audit to verify that inventory is truly marketable and usable. Obsolete stock should never be included in the NWC calculation at full value.

Strategic Exclusions: What to Leave Out of the Deal

To ensure a clean transition, certain items must be excluded from the working capital definition. Related-party notes and shareholder loans are internal matters that should be settled by the seller prior to close. You must also pay close attention to deferred revenue. While it appears as a liability, it represents work you must perform after closing for which the seller has already collected the cash. Treating deferred revenue as a debt-like item protects your future cash flow. Additionally, employee benefit accruals, such as unpaid PTO or earned bonuses, should be treated as debt to ensure you aren't paying for the seller's past labor costs.

Funding the Gap: Securing Capital for a Seamless Transition

Traditional lenders often hesitate to provide Working Capital as part of an acquisition loan because they view it as an intangible asset. While they're comfortable financing heavy machinery or real estate, funding the "gas in the tank" feels riskier to them. This creates a significant hurdle for buyers who need to maintain liquidity on Day 1. Successfully using working capital for business acquisition requires looking beyond standard commercial banking and tapping into specialized programs that recognize the strategic value of NWC.

Our firm operates on a success-based philosophy, meaning our objectives are perfectly aligned with your results. We focus on creating a capital structure that protects your cash flow rather than just filling a temporary need. By positioning your financial profile correctly, you can secure the necessary funds without the aggressive pressure typical of institutional finance. This collaborative approach ensures you have a steady hand guiding you through the complexities of acquisition funding.

SBA Loan Assistance for Acquisition Financing

The SBA 7(a) program remains the gold standard for mid-market acquisitions because it allows you to bundle working capital directly into the primary loan. As of March 2026, the SBA provides a 75% guarantee for loans greater than $150,000, which gives lenders the confidence to fund the operational side of your deal. You'll typically need a 10% equity injection, but professional SBA Loans consulting can help you structure this to ensure your application meets the strict requirements of preferred lenders. This approach ensures you aren't draining your personal reserves to cover the NWC peg.

The Impact of Credit Scores on Acquisition Funding

Your personal credit profile is often the first thing a lender scrutinizes before approving an acquisition package. High scores open doors to lower interest rates, such as the current SBA maximum spreads of Prime plus 3.0% for loans over $350,001. If your profile has inaccuracies, utilizing Credit Repair Services is a necessary step to qualify for maximum funding limits. The "Credit-to-Capital" pipeline functions as the essential link between a buyer’s personal financial standing and their ability to secure high-leverage funding for strategic acquisitions.

Preserving Cash with 0% Interest Funding Solutions

Strategic buyers often use a 0% Interest Funding Solution to handle immediate post-closing expenses. These unsecured business credit lines provide a flexible bridge between the closing date and the final NWC true-up, which often takes 60 to 90 days to finalize. By using these lines for initial payroll or inventory restocks, you keep your primary acquisition capital intact. This creates a win-win scenario where you can retire short-term bridge debt using the business's improved cash flow, all while benefiting from the permanent 100% bonus depreciation rules established by the OBBBA of 2025.

Strategic Advisory: Positioning Your Financial Profile for Success

Success in the 2026 M&A market requires more than just a signed contract; it requires a shift from a "transaction" mindset to a "transformation" mindset. While the closing date is a major milestone, it's actually the starting line for your new venture's growth. Positioning your financial profile correctly ensures that you aren't just buying a company, but building a sustainable future. Using working capital for business acquisition effectively means aligning your current capital procurement with your long-term strategic growth goals from the very beginning.

Professional Business Valuations are essential before you ever sign a Letter of Intent (LOI). These valuations provide the objective data needed to set a fair NWC peg, protecting you from overpaying for uncollectible receivables or obsolete inventory. When your funding strategy is integrated with Strategic Planning, you create a foundation of calm reliability. This methodical approach allows you to focus on operational improvements on Day 1 rather than scrambling to cover unexpected liquidity gaps.

M&A Consulting for Small and Mid-Sized Businesses

Entrepreneurs often find that large institutional finance firms offer a cold detachment that doesn't suit the nuances of mid-market deals. A boutique approach to Mergers and Acquisitions Consulting provides a more personalized, empathetic connection. At Koval Investments, we act as a seasoned strategic partner, sharing insider knowledge to help you navigate challenges. We specialize in identifying and disputing credit barriers that could otherwise limit your borrowing power. This collaborative, low-pressure environment ensures that every deal is a win-win for both the buyer and the firm.

Next Steps: Preparing Your Acquisition Strategy

Your journey toward a successful acquisition begins with a thorough audit of your own borrowing capacity. Understanding your credit profile and liquid reserves allows you to approach sellers with confidence. Once you've identified a target company, the next step is to have a strategic advisor perform a deep-dive review of their NWC history. This ensures that the "gas in the tank" is sufficient for your specific growth plans. If you're ready to move forward with a steady hand guiding your financial strategy, it's time to take the next step. Schedule a consultation with Koval Investments to secure your acquisition funding and ensure your transition is both stable and successful.

Building a Foundation for Post-Acquisition Growth

Mastering the intricacies of net working capital ensures you don't just close a deal, but inherit a business positioned for immediate momentum. By establishing a clear NWC peg and identifying debt-like items early, you protect your equity and lower your effective purchase price. Using working capital for business acquisition as a strategic tool rather than a closing-day hurdle allows you to focus on what matters most: scaling your new enterprise in the favorable 2026 economic environment.

We believe in a partnership where your success is our primary objective. Our success-based funding philosophy means we're as invested in the outcome as you are. Whether you need expert SBA loan assistance to maximize your leverage or comprehensive credit restoration to unlock higher limits, we provide the steady hand needed in today's complex financial landscape. You don't have to navigate these hurdles alone.

Secure your 0% interest funding for your next acquisition today and move forward with the confidence of a well-capitalized buyer. Your next chapter starts with the right financial foundation.

Frequently Asked Questions

What is the "NWC Peg" in a business acquisition?

The NWC peg is the target amount of net working capital a seller is required to deliver at the time of closing. It acts as a benchmark to ensure the business has enough "fuel" to operate without the buyer needing to inject immediate cash. Professionals typically calculate this peg by averaging the trailing 12 months of operating assets and liabilities to smooth out seasonal fluctuations.

Does working capital include cash in an M&A transaction?

In most mid-market deals structured as "cash-free, debt-free," working capital specifically excludes cash. The seller generally retains the cash on hand and settles all long-term debt before the transfer. The focus remains on operating items like accounts receivable, inventory, and prepaid expenses, which are essential for the daily functioning of the going concern.

How does a working capital adjustment affect the final purchase price?

The adjustment mechanism triggers a dollar-for-dollar change in the final equity value paid to the seller. If the actual working capital at closing exceeds the agreed-upon peg, the purchase price increases; if it falls short, the price decreases. This ensures you only pay for the actual value delivered on the closing date, protecting your initial investment.

Can I use an SBA loan to fund the working capital of a business I am buying?

Yes, the SBA 7(a) program is a highly effective tool for bundling working capital into your total financing package. It's a strategic way of using working capital for business acquisition because it allows you to secure operational funds at the same interest rate as the purchase price. This preserves your personal liquidity for future growth initiatives.

What happens if the seller delivers less working capital than agreed upon?

A shortfall in working capital results in a downward adjustment to the purchase price during the post-closing true-up. The seller essentially "reimburses" you for the missing liquidity, which gives you the necessary funds to restock inventory or cover payables. This process prevents you from inheriting a business that is financially "starved" on Day 1.

How do 0% interest funding solutions work for business acquisitions?

These solutions provide unsecured business credit lines with an introductory 0% APR period, often lasting 12 to 18 months. They serve as a flexible bridge to cover immediate operational costs or unexpected expenses while you finalize the post-closing true-up. It's a low-pressure method to maintain stability without incurring high-interest debt during the transition phase.

Why do I need a professional valuation to determine working capital needs?

A professional valuation identifies the "normalized" level of capital required to sustain the business based on industry standards and historical data. Without this precision, you might agree to a peg that is artificially high due to a recent seasonal spike or one-time event. This expert analysis is vital for using working capital for business acquisition as a successful negotiation lever.

How long does the post-closing working capital true-up typically take?

The true-up process generally takes between 60 and 90 days to complete. This window allows both the buyer and seller to review the final closing balance sheet and verify the accuracy of all accounts. Once both parties agree on the final numbers, the adjustment is settled, ensuring the transaction concludes with total transparency and alignment.