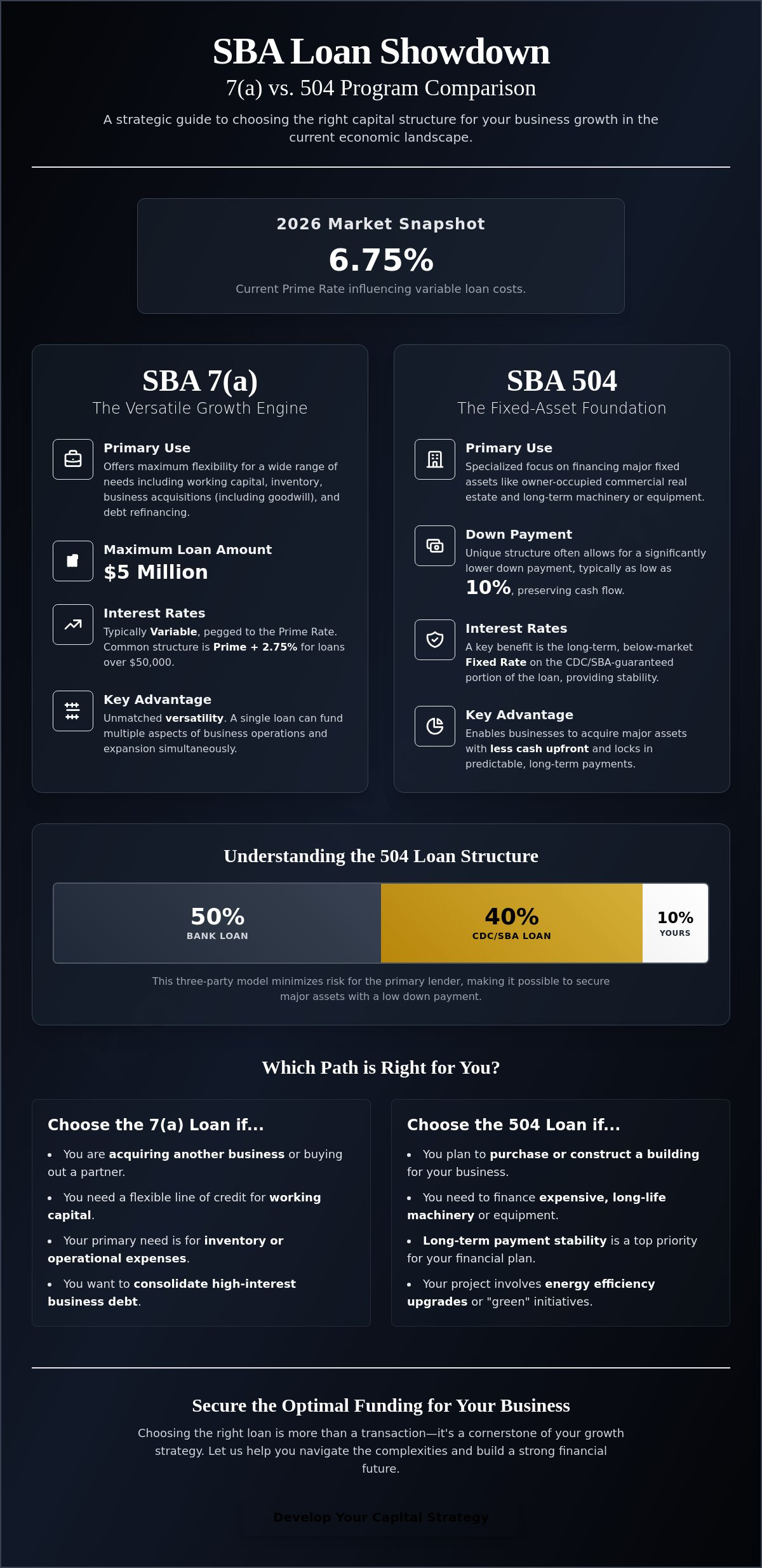

SBA 7(a) vs. 504 Loan: Choosing the Right Capital Strategy for 2026

Choosing the wrong capital structure today can cost your business more than a high interest rate ever will. With the Prime Rate holding at 6.75% as of June 2026, many entrepreneurs feel trapped between the urgent need to scale and the burden of variable debt. Deciding between an SBA 7(a) vs 504 loan isn't just a matter of checking boxes; it's a strategic maneuver that determines your operational agility for years to come.

You've likely felt the pressure of complex application requirements and the uncertainty of which assets qualify for specific programs. It's frustrating to see potential growth stall while you're navigating high interest rates on conventional loans. We understand that your goal isn't just to get funded, but to do so in a way that protects your cash flow and provides a stable foundation for expansion.

This guide will help you master the critical differences between the two most popular SBA programs to secure the optimal funding for your business growth. We'll break down the 2026 fee structures, compare the benefits of long term fixed rates versus working capital flexibility, and provide a clear roadmap to achieving lower monthly payments for your specific industry.

Key Takeaways

- Differentiate between the 7(a) flagship program's versatility and the 504's specialized focus on owner-occupied real estate and major equipment.

- Analyze the strategic trade-offs of the SBA 7(a) vs 504 loan, focusing on how variable rates and fixed-rate options impact your long-term debt service.

- Understand how the 504 program's three-party funding structure allows you to secure major assets with a significantly lower down payment.

- Learn how to leverage professional business valuations to strengthen your application and provide the necessary justification for higher loan amounts.

- Determine which capital strategy provides the necessary working capital to scale operations without compromising your business's financial stability.

Understanding the SBA Loan Landscape in 2026

The Small Business Administration (SBA) doesn't actually cut checks to business owners. Instead, it acts as a strategic guarantor. By promising to repay a portion of a loan if a borrower defaults, the SBA reduces the risk profile for traditional lenders. This government backing allows banks to offer terms that are often unavailable through conventional commercial channels. Understanding the nuances of an SBA 7(a) vs 504 loan is the first step toward building a capital strategy that scales with your ambitions rather than restricting them.

The 7(a) program serves as the agency's flagship offering. It's designed for maximum versatility, covering everything from working capital to business acquisitions. In contrast, the 504 loan is a specialized tool for economic development. It focuses specifically on fixed assets like owner occupied real estate and long term machinery. Choosing the wrong program creates more than just a paperwork headache; it can lead to capital bottlenecks that drain your liquidity or missed ROI because your debt structure doesn't align with your asset's lifespan.

The Core Purpose of SBA Financing

SBA lending exists to fill the gap where conventional financing falls short. Most traditional bank loans require high down payments and shorter repayment windows that can stifle a growing company's cash flow. By utilizing SBA loan programs, you can often secure funding with as little as 10% down. This empowerment of small businesses drives national economic growth and allows entrepreneurs to retain more cash for daily operations. It's a collaborative approach that turns a lender's "no" into a "yes" through structured risk mitigation.

Why 2026 is a Critical Year for SBA Borrowing

Market conditions in June 2026 have shifted the math for many borrowers. With the Prime Rate sitting at 6.75%, the variable nature of most 7(a) loans requires careful calculation. Borrowers are seeing rates for loans over $50,000 typically land at Prime plus 2.75%. This environment makes the fixed rate portion of a 504 loan particularly attractive for those looking to lock in stability.

There's also a clear regulatory push toward sustainability and domestic production. The SBA recently introduced significant fee waivers for manufacturers and expanded incentives for "green" 504 projects that focus on energy efficient upgrades. In FY 2025 alone, the SBA guaranteed 85,000 loans totaling $45 billion. Staying informed about these evolving 2026 regulations ensures you don't leave money on the table or find yourself overleveraged in a fluctuating interest rate environment.

The SBA 7(a) Program: Maximum Versatility for Operational Growth

The 7(a) loan is the Swiss Army knife of small business finance. It offers a maximum loan amount of $5 million, which provides a substantial runway for most growing enterprises. Unlike the more rigid SBA 504 loans, the 7(a) program allows you to use proceeds for almost any legitimate business purpose. This flexibility is what makes it the most popular choice for entrepreneurs who need to address multiple needs with a single funding source. Whether you're purchasing inventory, hiring key staff, or consolidating high interest debt, the 7(a) adapts to your specific operational requirements.

One of the most significant advantages of this program is its utility in business acquisitions. If you're looking to buy out a partner or acquire a competitor, the 7(a) is usually your most effective path. It allows for the financing of "goodwill," which is often a major component of a company's value but difficult to secure through traditional lending. When comparing the SBA 7(a) vs 504 loan, the ability to fund intangible assets often makes the 7(a) the clear winner for mergers and acquisitions.

You should be aware that 7(a) loans typically carry variable interest rates. These are usually pegged to the Prime Rate, which stands at 6.75% as of June 2026. For loans exceeding $50,000, you'll often see a spread of Prime plus 2.75%. While this variability introduces some risk if rates rise, the flexibility of the capital often outweighs the cost for rapidly scaling firms. If you're unsure how to structure your request for maximum approval, our team can help you refine your strategic planning to ensure every dollar works toward your long term goals.

When to Choose 7(a) Over Other Options

- Acquiring a competitor: Use the 7(a) to purchase a new business entity, including the intangible value that fixed asset loans won't cover.

- Unsecured working capital: Secure the liquidity needed for daily operations without always needing to tie the loan to a specific piece of real estate.

- Refinancing debt: Replace predatory or high interest business debt with a structured, government backed solution that improves your monthly cash flow.

The Role of Working Capital in 7(a) Strategy

Working capital is the lifeblood of expansion. In a 7(a) framework, non real estate loans generally come with a 10 year maturity. This provides a much longer repayment window than standard commercial lines of credit, which often require annual renewals or balloon payments. Integrating using working capital for business acquisition ensures you have the liquidity to handle the transition costs of a merger. It bridges the gap between closing the deal and reaching operational synergy, allowing you to focus on growth rather than immediate debt pressure.

The SBA 504 Loan: Building Foundations with Fixed-Asset Financing

While the 7(a) program provides operational agility, the 504 loan offers foundational stability. This program is specifically designed to help small businesses acquire major fixed assets that promote long term growth and community development. The 504 structure is unique because it involves a collaborative three party partnership. A conventional bank typically provides 50% of the project cost, a Certified Development Company (CDC) covers 40%, and you contribute a 10% down payment. This arrangement allows you to preserve capital while securing the infrastructure your business needs to scale.

The CDC is a non profit corporation certified by the SBA to support local economic development. Unlike a standard bank, the CDC's mission is to create jobs and revitalize communities. Because of this, the 40% portion of the loan comes with a below market, fixed interest rate that is fully amortized. When evaluating an SBA 7(a) vs 504 loan, the 504 is often the superior choice for high value investments like land, owner occupied buildings, or heavy machinery with a lifespan of ten years or more. As of June 2026, with the 10-year Treasury yield at approximately 4.48%, the CDC portion of these loans has recently remained in the 6.5% to 7.5% range, providing a predictable debt service that variable rate products cannot match.

The 504 Loan Structure Advantage

The primary benefit of the 504 program is cash preservation. Conventional commercial loans often require a 20% to 30% down payment, which can drain your liquidity. The 504's 10% requirement keeps more working capital in your accounts for day to day operations. Additionally, the repayment terms are highly favorable. Real estate projects can be financed over 20 or 25 years, ensuring your monthly payments remain manageable. If you're considering a major acquisition, our specialists can help you determine if SBA Loans are the right vehicle for your specific asset class.

Navigating the CDC Partnership

Working with a CDC requires a different mindset than traditional borrowing. Their underwriting process focuses heavily on the public policy goals of the project. To qualify for SBA loan programs like the 504, your project generally needs to meet job creation or retention requirements. For most borrowers, this means creating or retaining one job for every $95,000 of the CDC loan portion. Manufacturers have even more favorable terms, with fee waivers recently reinstated for FY 2026 to encourage domestic production.

Budgeting for a 504 loan also requires an understanding of the associated costs. You'll need to account for debenture fees and closing costs, which are typically rolled into the loan amount to minimize out of pocket expenses. While the closing process involves more parties than a 7(a) loan, proactive documentation and a clear alignment of your business goals can significantly streamline the timeline. By choosing the 504, you aren't just getting a loan; you're entering a strategic partnership designed to anchor your business in its community for decades.

Direct Comparison: SBA 7(a) vs. 504 Loan Framework

Comparing these two programs side by side reveals distinct financial trade-offs that impact your long term balance sheet. The 7(a) program caps total funding at $5 million, which is often sufficient for mid-sized acquisitions or major operational shifts. The 504 program offers higher limits because the CDC portion alone can reach $5.5 million. For manufacturers or energy efficient projects, this limit can even be exceeded, making the 504 the preferred choice for high value capital expenditures that anchor a business's physical footprint.

Collateral requirements represent another significant fork in the road. A 7(a) lender generally seeks a blanket lien on all business assets. If those assets don't fully secure the loan, the lender may require a lien on your personal residence. In contrast, the 504 program is typically project based. The collateral is limited to the specific assets being financed, such as the real estate or equipment. This provides a cleaner structure for investors who want to keep their personal and business portfolios separate. You should also consider the timeline; a 7(a) loan can often fund within 30 to 60 days, while the multi party nature of a 504 loan usually extends the process to 60 to 90 days or more.

Interest Rate Comparison in a 2026 Economy

In the current economic climate, interest rate structure is a primary concern for debt service management. Most 7(a) loans utilize a variable rate based on the Prime Rate plus a negotiated margin. With the Prime Rate at 6.75% in June 2026, many 7(a) borrowers are currently managing rates near 9.5%. The 504 program offers long term stability through its fixed rate debenture, which is especially valuable during periods of market volatility. The 10-year Treasury yield of approximately 4.48% serves as the benchmark for the CDC's debenture pricing, ensuring that 504 rates remain insulated from the fluctuations of the Prime Rate.

Down Payment and Collateral Nuances

Financing the required equity is often the final hurdle for SBA approval. While both programs offer lower down payments than conventional 25% requirements, the 504 program's 10% equity requirement is exceptionally rigid. If you're looking to preserve your cash reserves for scaling, you can source this 10% equity through our 0% interest funding solution. This strategy allows you to meet SBA requirements without depleting your liquid capital, ensuring you have the runway needed to support your new assets. Choosing the right SBA 7(a) vs 504 loan framework requires balancing this need for immediate liquidity against the benefits of long term, fixed rate debt.

Optimizing Your Profile for SBA Approval and Success

Securing a competitive loan in 2026 requires more than just a solid business idea. As the SBA reinstates stricter underwriting standards to ensure fiscal discipline, your financial profile must be impeccable before you ever sit down with a lender. Credit health has emerged as the primary hurdle for applicants this year. Even a minor discrepancy on a credit report can trigger a denial or lead to significantly higher interest rates that erode your profit margins. Preparing your profile is a collaborative effort that transforms your business from a risky prospect into a preferred borrower.

One of the most frequent reasons for funding delays is the lack of objective data to justify the loan amount. This is where professional business valuation services become indispensable. Whether you are pursuing an SBA 7(a) vs 504 loan, a certified valuation provides the third party validation lenders need to approve large capital requests. It prevents the common pitfalls of over-borrowing, which can lead to debt service ratios that stifle growth, or under-funding, which leaves you without enough working capital to execute your plan.

Credit Restoration as a Funding Catalyst

Optimizing your credit score before applying is a non-negotiable step in a high-interest environment. Our success-based philosophy focuses on identifying and correcting common errors, such as misreported balances or outdated late payments, which frequently trigger SBA denials. Improving your score by even fifty points can save you thousands of dollars in interest over the life of the loan. While your SBA application is pending, you can also explore a 0% interest funding solution to bridge any immediate liquidity gaps, ensuring your operations don't stall during the 60 to 90 day underwriting window.

The Strategic Advantage of Professional Consulting

Lenders don't just fund businesses; they fund plans. Integrating strategic business planning services into your application package shows the bank that you have a clear roadmap for repayment and job creation. This is particularly vital for the 504 program, which requires specific community impact goals. A well-structured five-year plan aligns your loan request with tangible growth milestones, making it easier for underwriters to say yes. Partnering with an advisor who understands the "insider" requirements of the SBA 7(a) vs 504 loan programs increases your approval odds and ensures your capital strategy is built for long-term stability rather than just a quick fix.

Securing Your Strategic Advantage in 2026

Determining the right capital path requires a balance between immediate operational needs and long term foundational goals. Whether you prioritize the versatility of a 7(a) for acquisition or the fixed rate stability of a 504 for real estate, your choice will define your company's financial trajectory. Success in the 2026 lending environment depends on more than just selecting a program. It requires a meticulously prepared application backed by accurate valuations and an optimized credit profile.

At Koval Investments, we bring over eight years of strategic capital procurement expertise to your corner. We provide national advisory for complex mergers and acquisitions and offer success-based credit restoration with no upfront financial risk. This collaborative approach ensures that your decision regarding an SBA 7(a) vs 504 loan is supported by deep industry insight and a commitment to your results. We believe in building partnerships that prioritize your progress over simple transactions.

Secure your business future with expert SBA loan assistance and credit optimization. Your vision for expansion deserves a steady, experienced partner to navigate the complexities of institutional finance. We look forward to helping you scale with confidence.

Frequently Asked Questions

Can I use an SBA 7(a) loan to buy out a business partner?

Yes, you can use an SBA 7(a) loan to buy out a business partner's interest in a company. This is a standard use for the program because it allows for the purchase of intangible assets like stock or partnership equity. The 504 program is restricted to fixed assets, so the 7(a) is the correct choice for restructuring ownership. You'll need to provide a professional business valuation to justify the buyout price and ensure the remaining owner has sufficient experience to lead.

Is it possible to have both an SBA 7(a) and an SBA 504 loan simultaneously?

You can absolutely have both an SBA 7(a) and an SBA 504 loan at the same time. Many entrepreneurs use a 504 loan to purchase their facility while securing a 7(a) loan for the working capital or equipment needed to operate within it. This dual strategy allows you to maximize the benefits of both programs. It's an effective way to lock in long term real estate rates while maintaining operational liquidity.

What is the minimum credit score required for an SBA 7(a) vs. 504 loan in 2026?

Most lenders look for a minimum credit score of 680 for both programs in 2026. While the SBA doesn't set a hard floor, individual banks use this benchmark to assess risk and determine your interest rate margin. If your score is lower, focusing on credit repair before applying is a strategic move that can prevent denial. A higher score often results in more favorable terms when comparing an SBA 7(a) vs 504 loan in a competitive market.

Do SBA 504 loans have a prepayment penalty compared to 7(a) loans?

SBA 504 loans carry a declining 10-year prepayment penalty on the CDC portion of the debt. This is significantly different from the 7(a) program, which typically only penalizes prepayments on loans with terms of 15 years or more during the first three years. If you plan to refinance or sell the asset quickly, the 7(a) might offer more flexibility. The 504 is designed for business owners committed to their location for the long haul.

How much are the typical closing costs for an SBA 504 loan?

Closing costs for an SBA 504 loan generally range between 3% and 5% of the total project cost. These costs include various fees such as the CDC processing fee, legal fees, and the SBA guarantee fee. A major advantage of the 504 program is that most of these costs can be financed directly into the loan. This minimizes the out of pocket cash required at closing, preserving your reserves for business growth.

Can I use an SBA 7(a) loan for 100% of a business acquisition?

It's unlikely you'll secure 100% financing for a business acquisition through the 7(a) program. The SBA generally requires a minimum equity injection of 10% from the borrower to ensure you have skin in the game. This down payment can sometimes be a combination of cash and seller financing, provided the seller's note is on full standby. We help clients navigate these equity requirements to ensure their application meets lender standards.

What happens if I don’t meet the job creation requirements for a 504 loan?

If your business doesn't meet the job creation requirements, you can still qualify for a 504 loan by meeting a community development or public policy goal. These goals include expanding exports, aiding rural development, or implementing energy efficient upgrades. The SBA recently emphasized these alternatives to support manufacturers and green energy projects. This flexibility ensures that capital remains accessible to businesses that drive economic value in ways other than direct hiring.

How does the SBA definition of a "small business" change for the 504 program?

The 504 program often uses an alternate size standard to define a small business, which is broader than the 7(a) standard. To qualify, your business must have a tangible net worth of less than $15 million and an average net income of less than $5 million after taxes for the previous two years. This allows larger companies that might exceed 7(a) industry caps to still access government backed financing. It's a vital distinction when comparing an SBA 7(a) vs 504 loan for mid-sized enterprises.