How to Access Capital for Business Expansion: A Strategic Guide for 2026

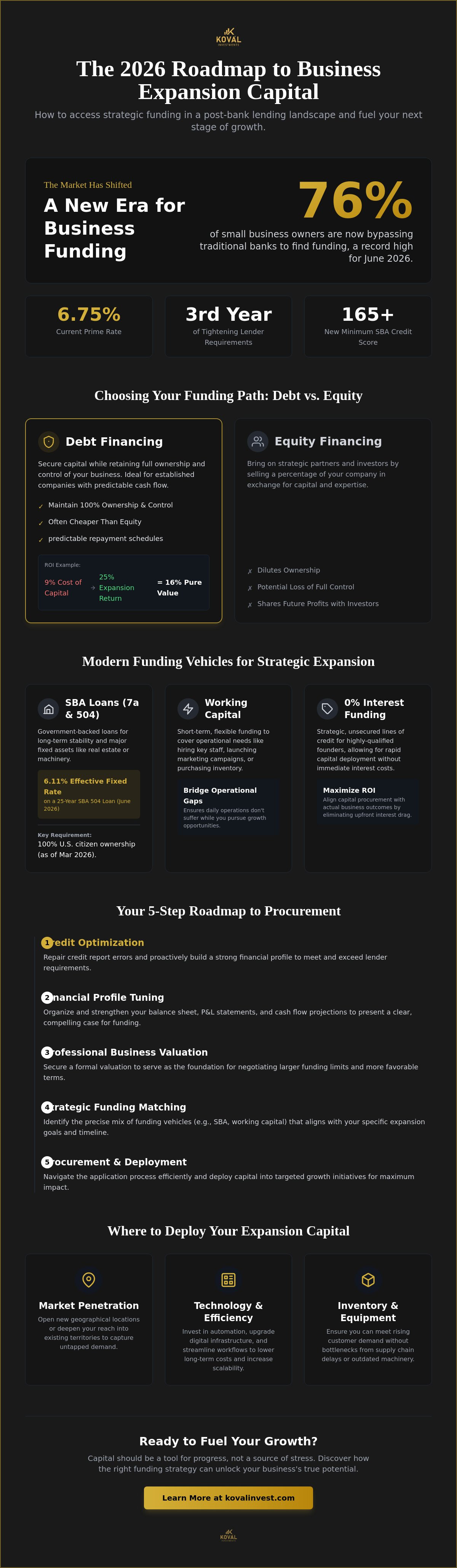

Over 76% of small business owners are now bypassing traditional banks to find the funding they need to grow, marking a survey all-time high for June 2026. It's understandable if you feel hesitant to scale when the Prime Rate sits at 6.75% and traditional lenders continue to tighten their requirements for the third consecutive year. You've likely felt the frustration of high interest rates eating into your projected ROI, or worried that a credit score below the new SBA minimum of 165 might stall your momentum. Many entrepreneurs find themselves stuck in a cycle of confusion, unsure which funding vehicle actually aligns with their long-term goals.

We believe that capital should be a tool for progress, not a source of stress. This guide will show you exactly how to access capital for business expansion by leveraging strategic alternatives that traditional institutions often overlook. You'll discover the most effective ways to secure expansion capital, from 0% interest solutions to optimized SBA loans, while learning how to repair your financial profile for maximum funding. We'll walk through the roadmap from credit optimization to procurement, helping you identify the right mix of working capital to fuel your next stage of growth with confidence.

Key Takeaways

- Learn why traditional bank lending is no longer the primary path for growth and how to navigate the 2026 digital lending landscape.

- Identify whether SBA 7(a) programs or immediate working capital solutions best fit your specific scaling objectives.

- Understand the critical steps to access capital for business expansion by repairing credit report errors and optimizing your financial profile.

- Discover how a professional business valuation serves as the foundation for securing larger funding limits and better terms.

- Explore the benefits of 0% interest funding solutions that align your capital procurement with actual business outcomes.

What is Expansion Capital and Why is it Critical in 2026?

Expansion capital is the fuel used to accelerate a business that has already found its footing. Unlike seed funding, which focuses on the initial launch, or survival capital, which keeps a struggling company afloat, expansion capital is strictly designated for scaling operations, entering new markets, or completing strategic acquisitions. In June 2026, the ability to access capital for business expansion has become a primary differentiator between firms that merely exist and those that dominate their industry. It's about moving from a state of stability to a state of aggressive, calculated growth.

The lending environment has shifted significantly this year. With the Prime Rate holding at 6.75%, traditional bank loans are no longer the default choice for many. Digital lending platforms and non-bank alternatives have matured, offering faster approvals and more tailored structures than the rigid institutional models of the past. Success in this landscape requires a clear distinction between "survival" funding and "strategic" expansion capital. Survival funding is reactive and often carries high costs because it's sought under pressure. Strategic capital is proactive. You'll find that timing your capital injection is just as vital as the amount you secure. Securing funds while your balance sheet is strong gives you the leverage to negotiate terms that protect your ROI.

The Core Drivers of Business Expansion

Growth usually follows three distinct paths in the current market. First, market penetration involves reaching deeper into current territories or opening new geographical locations to capture untapped demand. Second, investing in technology and operational efficiency has become essential. By automating workflows or upgrading digital infrastructure, businesses lower long-term costs and increase their scalability. Finally, many firms utilize expansion capital for inventory and equipment financing. This ensures they can meet rising demand without the bottlenecks of supply chain delays or outdated machinery.

Equity vs. Debt: Choosing the Right Path

Choosing how to fund growth requires a firm grasp of Corporate Finance Fundamentals. While equity involves selling a piece of your vision to investors, debt allows you to maintain 100% ownership and control. For established businesses with predictable cash flow, debt is often significantly cheaper than giving up a percentage of future profits. The key is analyzing the "cost of capital" against the expected ROI of the expansion. If the cost of the funding is 9% but the expansion yields a 25% return, that spread represents pure value for the owner. Leveraging debt as a tool for growth allows you to scale without sacrificing the equity you've worked hard to build.

Types of Capital for Business Expansion

Identifying the right funding vehicle is the first step to successful growth. While traditional banks have tightened their lending standards for the third consecutive year, modern founders have a broader toolkit to access capital for business expansion effectively. The current market offers a spectrum of solutions, ranging from government-backed guarantees to highly specialized unsecured funding. Choosing between them depends entirely on your specific growth stage and the nature of your investment. Whether you're looking for long-term stability or short-term agility, understanding the nuances of each option is essential for maintaining a healthy balance sheet.

SBA loans are a cornerstone of growth for many established firms. The 7(a) program remains the most versatile, while the 504 program is specifically designed for major fixed assets. For instance, the effective fixed rate for a 25-year SBA 504 loan in June 2026 is 6.11%, making it an attractive option for long-term stability. However, applicants must navigate strict new regulations. As of March 1, 2026, businesses must be 100% owned by U.S. citizens to qualify for these programs. Understanding these nuances in SBA financing options can save months of wasted effort during the application process.

Not every growth move requires a ten-year commitment. Working capital provides the short-term liquidity needed to hire key staff or purchase inventory ahead of a major launch. It's the bridge that ensures your daily operations don't suffer while you chase new opportunities. For high-qualified founders with excellent credit profiles, 0% interest solutions represent a strategic advantage. These are often unsecured lines that allow for rapid deployment without the drag of immediate interest costs. Similarly, Real Estate Investment Funding is essential for those looking to expand their physical footprint, whether through purchasing a new facility or renovating an existing one.

SBA Loan Strategies for Commercial Growth

Success starts with professional SBA loan assistance to navigate the complex documentation requirements. The 504 program is particularly powerful for purchasing commercial real estate because it requires a lower down payment than most conventional bank loans. To prepare, ensure your financial statements are current and your debt-to-income ratio is within the 1.25x coverage range typical for 2026 approvals. If you're unsure which vehicle matches your 2026 goals, consulting with a strategic advisor can help align your capital mix with your long-term vision.

Working Capital for Rapid Scaling

Short-term capital is often the most efficient way to maintain momentum during a transition. Many founders are now using working capital for business acquisition to fold competitors into their existing operations without depleting their cash reserves. This approach manages cash flow effectively, ensuring you have the resources to integrate the new entity while your primary business continues to thrive. It's a strategic method to scale quickly while keeping your long-term debt obligations manageable.

The Credit Hurdle: Optimizing Your Profile for Access

Your credit profile is the primary filter through which lenders view your expansion plans. It isn't just a pass or fail metric. It's a valuation of your financial reliability that directly determines your funding ceiling. In 2026, the stakes are higher than ever. The SBA has increased the minimum Small Business Scoring Service (SBSS) score to 165. If your score falls below this threshold, you aren't just looking at higher interest rates; you're looking at a complete block on many traditional Business Expansion Loans. Optimizing this profile before you apply is the most effective way to lower the total cost of capital over the life of your funding.

Identifying errors is your first strategic move. Credit bureaus frequently report outdated information or incorrect debt loads that artificially depress your score. Disputing these inaccuracies isn't just about financial housekeeping. It's a calculated effort to unlock larger funding limits. By building a "lender-ready" profile, you present a low-risk opportunity to institutions. This transparency directly translates to more favorable terms when you access capital for business expansion, ensuring your growth isn't hampered by avoidable financial friction.

Credit Repair as a Growth Strategy

Professional credit restoration should be viewed as a high-ROI investment rather than a simple expense. Improving your score by even a few dozen points can shift your SBA 7(a) interest rate from the 14% range down toward the 9.75% floor. This spread can save your business thousands of dollars in annual interest costs. Additionally, you must proactively manage your debt-to-income (DTI) ratio. Lenders want to see that your current obligations don't choke your ability to reinvest. Strategic restructuring of existing debt can improve this ratio, making your expansion application significantly more attractive to underwriters.

Establishing Business Credit Independently

Separating your personal and business credit profiles is essential for long-term protection and scalability. Many founders rely too heavily on personal guarantees, which eventually limits their total borrowing power. By establishing trade lines with vendors and ensuring they report your payment history, you build a standalone business credit score. A strong, independent business profile opens doors to unsecured funding and higher-limit working capital lines. This separation ensures that your personal financial health remains secure while you make the aggressive moves necessary to scale your company to the next level.

A 5-Step Roadmap to Procurement

Securing the right funding isn't a matter of luck; it's a methodical process of alignment and preparation. Many entrepreneurs fail to access capital for business expansion because they approach lenders before their internal story is fully formed. To maximize your chances of approval and secure the most favorable terms, you must follow a structured path that bridges the gap between your current financials and your future goals. This roadmap ensures that every action you take builds toward a successful capital injection.

- Step 1: Conduct a professional business valuation. You need an objective assessment of your company's worth to justify the funding amount you're requesting.

- Step 2: Optimize credit profiles. As we discussed earlier, repairing errors and optimizing your DTI ratio ensures you qualify for the lowest possible rates, such as the 6.11% fixed rate currently available for SBA 504 loans.

- Step 3: Align goals with the correct vehicle. Determine if your expansion requires the long-term stability of an SBA loan or the rapid agility of a 0% interest line.

- Step 4: Engage professional support. Utilizing specialized capital procurement services allows you to offload the complex application process to experts who understand lender requirements.

- Step 5: Execute and monitor. Once funds are deployed, track your ROI against specific milestones to ensure the capital is driving the intended growth.

Following this sequence reduces the risk of rejection and positions you as a sophisticated borrower. If you're ready to begin this process with a partner who understands the 2026 lending environment, connect with our strategic team today to evaluate your options.

The Role of Business Valuation in Expansion

Lenders require a professional valuation because it provides a baseline for risk assessment. It isn't just about what you think your business is worth; it's about what the market and your cash flow can support. A high-quality valuation serves as a powerful negotiation tool, allowing you to secure higher funding limits or better terms with investors. Additionally, if your expansion involves mergers or acquisitions, having an accurate financial snapshot is the only way to ensure you're paying a fair price and integrating a healthy asset.

Strategic Planning for Capital Deployment

Capital is only as effective as the plan behind it. You must create a detailed roadmap for how every dollar will be spent, whether it's for hiring, technology, or inventory. Setting clear milestones allows you to measure the success of the expansion in real-time. If a specific initiative isn't yielding the expected ROI, a well-defined plan gives you the framework to adjust your strategy based on market feedback and current cash flow. This disciplined approach ensures that your capital deployment leads to sustainable growth rather than just increased overhead.

Leveraging 0% Interest Funding for Maximum ROI

Traditional institutions rarely mention interest-free options because their business model relies on your debt service. For founders with optimized profiles, the ability to access capital for business expansion without immediate interest costs is a significant competitive advantage. This funding typically involves unsecured business credit lines that offer 0% APR for introductory periods, often lasting between 12 and 22 months. It differs fundamentally from the SBA loans or working capital terms we discussed earlier, where interest begins accruing the moment the funds hit your account.

Adopting a "success-based" philosophy means aligning your funding with specific business outcomes. 0% interest capital is the ultimate tool for risk-averse expansion because it removes the immediate pressure of monthly interest payments. Instead of your ROI being eaten by a 14% interest rate, every dollar generated by your new location or product line stays in the business. To qualify for these interest-free lines in 2026, you'll need the lender-ready profile we detailed in section three, specifically a clean credit report and a business that shows clear operational momentum.

The Benefits of Interest-Free Growth

Eliminating interest expenses directly inflates your profit margins during the most volatile phase of growth. Founders use these 0% APR periods to fund aggressive marketing campaigns or bulk inventory purchases for new locations. It's a strategic way to scale without the drag of debt service. By reinvesting that saved interest back into your operations, you accelerate your scaling timeline. By the time the introductory period ends, the expansion should already be generating the cash flow necessary to clear the balance or transition into a long-term fixed-rate structure.

Partnering with Koval Investments for Expansion

We don't just provide a list of lenders; we act as your strategic partner in the procurement process. Our collaborative approach integrates professional credit repair services with deep expertise in both SBA loans and 0% interest solutions. We understand that the right capital mix is unique to your stage of growth. By managing the complexities of documentation and lender requirements, we help you access capital for business expansion while you focus on running your company. Our goal is a win-win scenario where your growth is fueled by the most cost-effective capital available in the 2026 market. Secure your expansion capital with Koval Investments and take the next step in your growth journey with a trusted advisor by your side.

Securing Your Strategic Growth for 2026

The roadmap to scaling your business requires more than just a vision; it demands a precise financial foundation. We've explored how a professional business valuation and targeted credit repair can transform your funding potential. By shifting your focus from traditional bank debt to strategic vehicles like 0% interest lines and SBA programs, you protect your profit margins while accelerating your timeline. The ability to access capital for business expansion in 2026 depends on this alignment between your financial profile and your growth objectives.

Koval Investments stands as your steady partner in this journey. We provide expert SBA loan assistance and comprehensive credit repair to ensure you're always lender-ready. Our success-based funding philosophy means we're as invested in your results as you are, removing the friction from capital procurement. You don't have to navigate these complex financial landscapes alone. Partner with Koval Investments to access 0% interest expansion capital today. Let's work together to turn your expansion goals into a tangible, well-funded reality.

Frequently Asked Questions

What is the fastest way to access capital for business expansion?

Unsecured working capital lines and 0% interest business credit solutions are the fastest routes, often providing funds within 48 hours to two weeks. These options bypass the lengthy appraisal and underwriting processes required by traditional term loans. While SBA loans offer long-term stability, they can take several months to close. For immediate scaling needs like inventory or equipment, these high-speed vehicles are the most practical choice.

Can I get expansion capital if my business credit score is low?

You can still secure funding with a lower score through alternative lenders, though it often comes with higher interest rates and shorter terms. However, the SBA increased the minimum SBSS score to 165 in 2026, making government-backed options harder to reach for those with credit challenges. It's usually more strategic to engage in credit repair first to unlock larger limits and the 0% interest solutions that high-qualified founders enjoy.

Is an SBA loan better than 0% interest funding for expansion?

The choice depends entirely on your specific growth goal and asset type. SBA 504 loans are superior for long-term stability in commercial real estate, offering fixed rates around 6.11% in June 2026. Conversely, 0% interest solutions are the better tool for funding marketing cycles or short-term inventory needs. These interest-free lines allow you to reinvest every dollar of profit back into the business without immediate debt service costs.

What documentation do I need to apply for expansion capital?

Lenders typically require three years of federal tax returns, year-to-date profit and loss statements, and a current balance sheet. You'll also need a professional business valuation to justify the loan amount and a detailed strategic plan showing how the capital will drive growth. Having these documents ready before you apply minimizes delays and signals to the lender that your business is a well-managed, low-risk investment.

How does credit repair help me get a larger business loan?

Credit repair directly increases your borrowing capacity by lowering the lender's risk profile. When you remove inaccuracies and optimize your personal and business scores, you move into higher tier lending categories. This shift allows you to access capital for business expansion at much lower interest rates. Higher scores also lead to larger unsecured limits, giving you the financial flexibility to scale without pledging excessive collateral.

What is the typical interest rate for expansion capital in 2026?

With the Prime Rate at 6.75% as of June 2026, interest rates vary significantly by funding type. SBA 7(a) variable rate loans currently range from 9.75% to 13.25%, while bank term loans can fall anywhere between 8% and 17.25%. For those seeking the lowest cost of capital, SBA 504 loans remain attractive at approximately 6.11% fixed, while 0% interest solutions provide the ultimate savings for qualified borrowers during their introductory periods.

How much capital can I realistically access for my business?

Your funding capacity is primarily determined by your Debt Service Coverage Ratio (DSCR), with most 2026 lenders requiring at least 1.25x coverage. This means your cash flow must comfortably support the new debt along with existing obligations. A professional business valuation also plays a key role, as it sets the ceiling for what lenders are willing to provide. Most established firms can realistically access between 10% and 30% of their annual revenue.

Do I need a business valuation before applying for funding?

Yes, a professional business valuation is a critical component of a successful funding application. It provides an objective baseline that justifies your requested loan amount to underwriters and investors. Beyond just meeting lender requirements, an accurate valuation helps you understand your true market position. This knowledge allows you to negotiate more favorable terms and ensures you aren't over-leveraging the business during your expansion phase.