SBA Loan Assistance: A Strategic Guide to Navigating Small Business Funding in 2026

Securing government-backed capital in 2026 isn't a matter of luck or simply filling out forms; it's an exercise in strategic financial positioning. You've likely felt the weight of the endless documentation required for a 7(a) or 504 loan, or perhaps you've hesitated to apply because your credit profile doesn't feel strong enough. It's frustrating to know your business is ready for growth while the path to funding remains obscured by red tape. Professional SBA loan assistance can transform this overwhelming process into a clear, manageable strategy that aligns with your long-term goals.

We understand that the stakes are high, especially with new regulations like the citizenship and residency requirements that took effect on April 1, 2026. This guide will show you how to optimize your application and meet the strict eligibility standards required for approval. We'll explore the nuances of specialized programs like the MARC initiative for manufacturers, clarify credit expectations, and provide a roadmap to help you secure the capital your business deserves without the typical stress of procurement. By the end of this article, you'll have the clarity needed to move from uncertainty to a successful funding outcome.

Key Takeaways

- Professional SBA loan assistance bridges the gap between your growth goals and federal lender requirements, transforming a complex process into a streamlined capital strategy.

- Distinguish between the 7(a) program for flexible working capital and the 504 program for fixed-asset investments to ensure your funding choice aligns with your specific growth stage.

- Learn why a current low credit score isn't a permanent barrier and how optimizing your financial profile directly impacts the interest rates you're offered.

- Build a lender-ready application package by focusing on critical financial statements and a business plan that proves your long-term repayment ability.

- Leverage a success-based partnership that combines capital procurement with strategic financial optimization to minimize risk and accelerate your results.

Navigating the SBA Landscape: Why Expert Assistance is a Strategic Advantage

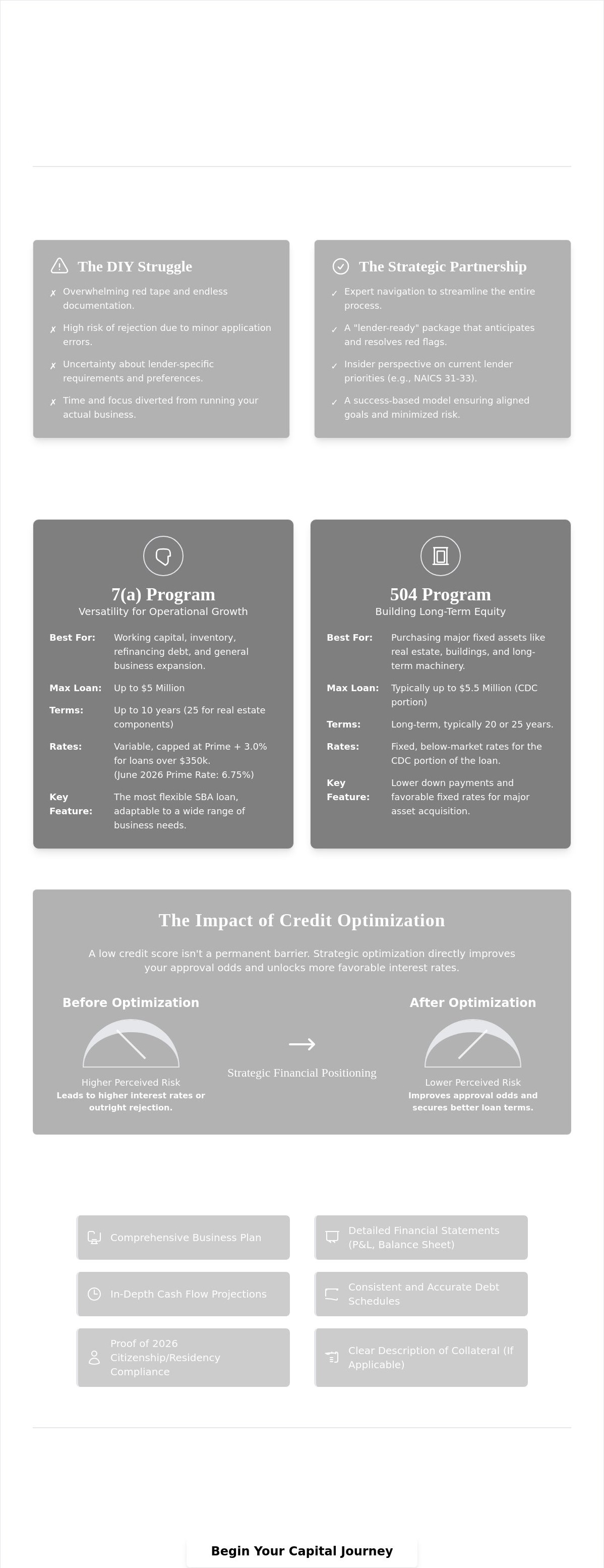

Securing capital through federal programs often feels like a full-time job. Professional SBA loan assistance isn't just a service; it's a strategic advisory that bridges the gap between your growth ambitions and the rigid requirements of federal lenders. Many business owners attempt the "DIY" route, only to find themselves buried under layers of technical documentation and conflicting advice. By choosing a mentored approach to capital procurement, you're not just saving time. You're ensuring that your financial narrative is presented in a language that lenders understand and respect.

It's vital to remember that the Small Business Administration (SBA) doesn't typically lend money directly to you. Instead, it acts as a guarantor, promising the bank that a portion of the loan will be repaid if the business defaults. Because the agency only sets the guidelines, the individual bank still holds the power of approval. In the current June 2026 lending environment, where the Prime Rate sits at 6.75%, banks have become increasingly selective. They're looking for "lender-ready" packages that go beyond basic tax returns to show a deep understanding of cash flow and market positioning.

The Reality of SBA Approval Rates

Applications are frequently rejected for reasons that have nothing to do with the viability of the business. Common "red flags" include inconsistent debt-schedule reporting, insufficient collateral descriptions, or a failure to address the new 2026 citizenship and residency requirements. Expert SBA loan assistance identifies these hurdles before your file ever hits a loan officer's desk. We maintain an insider perspective on what specific institutions are prioritizing right now. For instance, many lenders are currently favoring manufacturing projects due to the significant fee waivers available in the 7(a) and 504 programs for NAICS sectors 31-33.

Moving Beyond Simple Funding to Strategic Partnership

Working with a trusted advisor changes the dynamic of capital procurement from a high-pressure transaction to a collaborative financial plan. Our success-based philosophy ensures that our goals are perfectly aligned with yours. We handle the heavy operational burden of document gathering and lender communication, allowing you to stay focused on running your company. This partnership approach provides a steady hand in a complex landscape, ensuring that the capital you secure actually supports your long-term operational efficiency rather than just providing a short-term fix.

Decoding SBA Loan Programs: Finding the Right Fit for Your Business Goals

Identifying the right vehicle for capital is the first step in any successful procurement strategy. While many entrepreneurs gravitate toward the most popular options, the nuances of different SBA loan programs can significantly impact your long-term operational flexibility. Selecting a program isn't just about the dollar amount; it's about aligning the capital's structure with your specific business valuation and future exit strategy.

The 7(a) Program: Versatility for Operational Growth

The 7(a) program remains the most versatile instrument for small business owners. It's the primary tool for securing working capital, purchasing inventory, or refinancing high-interest debt that's currently stifling your cash flow. In 2026, the maximum loan amount is $5 million, with variable rates capped at Prime plus 3.0% for loans over $350,000. For general operational growth, these loans typically offer maturity terms of up to 10 years, though real estate components can extend this to 25 years. While personal guarantees are standard for anyone owning 20% or more of the business, professional SBA loan assistance helps you navigate the collateral requirements that banks often use to mitigate their risk.

The 504 Program: Building Long-Term Equity

If your goals involve building tangible equity, the 504 program is often the superior choice. This program utilizes a unique partnership between a private lender and a Certified Development Company (CDC). It's designed specifically for major fixed-asset investments, such as purchasing commercial real estate or heavy machinery. The primary advantage here is the fixed-rate financing, which provides stability against market fluctuations. For instance, as of May 2026, a 25-year 504 term carries a fixed rate of 5.952%. Keep in mind that 504 funding often requires a commitment to job creation or the fulfillment of specific public policy goals, making it a highly intentional choice for established firms.

For startups or businesses with smaller capital needs, the Microloan program provides up to $50,000 through community-based intermediaries. This is an excellent entry point for newer ventures that haven't yet built the extensive credit history required for larger 7(a) loans. Regardless of the path you choose, the key is to ensure the debt structure supports your growth trajectory. If you're planning a future merger or acquisition, the way you leverage these funds now will dictate your strategic planning options and overall enterprise value. Professional SBA loan assistance ensures that your capital structure remains an asset rather than a liability as you scale.

The Hidden Barrier: How Credit Optimization Impacts Your Approval Odds

Many entrepreneurs believe a less-than-perfect credit score is an automatic "no" from a lender. This isn't true. While the SBA loan programs have strict standards, your current score is a snapshot, not a life sentence. A lower score doesn't just risk rejection; it directly inflates your borrowing costs. Lenders use your credit profile to determine where you fall within the allowed rate caps. For example, with the Prime Rate at 6.75% in mid-2026, a stronger score could be the difference between paying Prime plus 3% or being pushed into a much higher bracket. Even a small increase in your score can move you into a lower interest rate tier, saving your business thousands over the life of the loan.

Identifying and Disputing Credit Report Inaccuracies

Errors are surprisingly common in the financial world. Inaccurate payment histories, outdated debt balances, or even simple clerical mistakes like wrong addresses can drag down your profile. Part of comprehensive SBA loan assistance involves a methodical audit of both personal and business credit reports. We look for these red flags and use proven Credit Repair Services to clear the path. A clean profile is essential before you enter the lender match process. It demonstrates financial responsibility and reduces the lender's perceived risk. This isn't about "gaming" the system; it's about ensuring your business is represented accurately to the institutions holding the capital.

Leveraging 0% Interest Solutions During Optimization

Waiting for credit scores to climb shouldn't stop your operations. A strategic 0% interest business funding approach provides a powerful bridge during this transition. This interest-free capital allows you to meet immediate needs, such as inventory purchases or equipment repairs, while we work on the long-term goal of an SBA approval. It's a win-win scenario. You get the liquidity required for growth today, and the improved credit profile ensures you'll qualify for the best possible SBA terms tomorrow. This synergy between short-term flexibility and long-term stability is a hallmark of a mature capital strategy. By utilizing professional SBA loan assistance to optimize your credit now, you aren't just looking for an approval; you're looking for the most efficient capital procurement possible.

The SBA Application Blueprint: Preparing a Lender-Ready Package

Having a solid credit score and selecting the right program are critical steps, but they only get you to the starting line. To cross the finish line with an approval, you must present a document package that leaves no room for doubt. Professional SBA loan assistance ensures your application isn't just a collection of forms, but a persuasive argument for your business's stability. Lenders in 2026 prioritize "lender-ready" files that demonstrate a clear, low-risk path to repayment through meticulous financial reporting.

Your Profit and Loss (P&L) statements, balance sheets, and cash flow projections serve as the bedrock of this package. Banks aren't only interested in your historical performance; they're looking at your future sustainability. A three-year projection that accounts for the current 6.75% Prime Rate is essential to show that your margins can handle the debt service. Furthermore, every owner with a 20% stake or more must provide detailed personal financial statements. This transparency confirms that the leadership team is personally invested and meets the necessary residency and citizenship requirements that were updated in early 2026.

One of the most scrutinized components is the "Use of Proceeds" statement. Vague requests for "general working capital" often lead to delays or outright rejections. You must be specific. Whether you're purchasing a specialized piece of equipment for a manufacturing plant or hiring a new management tier to oversee an expansion, every dollar must be accounted for. This level of detail proves to the lender that the capital will be used to generate tangible growth rather than just covering operational inefficiencies.

Crafting the Business Narrative

A compelling business plan is more than a formality; it's a management narrative. Lenders look for deep industry experience and a clear understanding of your competitive landscape. You should present market research that proves your niche is defensible and your revenue streams are diversified. This is where strategic planning becomes a tangible asset. It justifies the loan amount by showing a logical progression from capital injection to increased enterprise value, making the bank's decision much easier.

The Role of Professional Business Valuations

If your goal involves a merger or an acquisition, a formal Business Valuation is a non-negotiable requirement. It provides an objective baseline for the assets being financed, which prevents the dangerous cycle of under-funding or over-leveraging. Accurate valuations ensure that the loan amount matches the collateral's true worth, protecting your equity and the lender's interest. By integrating professional SBA loan assistance into this phase, you ensure that every asset, from real estate to intellectual property, is valued correctly to support your long-term capital strategy.

Partnering for Growth: How Koval Investments Streamlines Your Capital Journey

Choosing a financial partner is a decision that dictates the future ceiling of your business. While many firms treat capital as a one-off transaction, we view it as the foundation of a long-term strategic alignment. Our approach integrates capital procurement with deep financial optimization, ensuring that the debt you take on is structured to fuel your specific growth objectives. Professional SBA loan assistance should provide more than just a list of lenders; it should provide a steady hand to guide you through the complexities of federal regulations and bank expectations.

Our success-based philosophy ensures that our goals are perfectly mirrored by your results. We don't operate on high-pressure sales tactics or upfront risks to your capital. Instead, we focus on a collaborative venture where our compensation is tied to the tangible value we deliver. This mindset creates a low-pressure environment where the focus remains entirely on the practicalities of your business's advancement and the precision of your application package.

From Credit Repair to Capital Access

The journey to an approved loan often begins long before the first application form is signed. We provide a seamless transition from credit restoration to final funding, addressing the "hidden barriers" that often lead to rejection. Managing multiple vendors for credit and capital can lead to fragmented strategies and missed opportunities. By having a single partner oversee both your credit profile and your funding strategy, you ensure that every dispute and optimization is done with the final lender's requirements in mind.

We pride ourselves on a "straight-talk" mentality. During our initial assessment of your business's health, we provide a pragmatic view of your current eligibility and a clear roadmap for improvement. This honesty saves you time and prevents the frustration of pursuing programs that don't fit your growth stage. We act as an insider on your team, sharing the knowledge you need to navigate challenges alongside us rather than from a distance.

Securing Your Business Legacy

Strategic funding is a powerful tool for those looking at the bigger picture of their industry. Many of our clients utilize SBA programs for business acquisition, allowing them to expand their market share or acquire competitors with favorable government-backed terms. Whether you are scaling operations or preparing for an eventual exit, the way you manage your capital today defines your enterprise value tomorrow.

While an initial loan solves an immediate need, a strengthened credit profile and a refined financial narrative provide value that lasts for the life of your company. It's about more than just one approval; it's about building a legacy of financial stability and operational efficiency. If you are ready to move past the paperwork and secure a roadmap to approval, we are ready to help. Partner with Koval Investments for your SBA journey and let's assess your funding eligibility through a professional consultation focused on your long-term success.

Mastering Your Capital Strategy for 2026

Navigating federal funding requires more than just persistence; it demands a precise alignment of your credit profile, financial documentation, and growth objectives. By selecting the right program, whether it's the versatile 7(a) or the asset-focused 504, you position your business to leverage capital as a catalyst rather than a burden. Professional SBA loan assistance ensures every detail of your application reflects a lender-ready narrative, minimizing the risk of rejection and maximizing your long-term operational efficiency.

Since 2018, Koval Investments has acted as a steady hand for entrepreneurs seeking to scale. Our success-based philosophy means we're fully invested in your results, providing a seamless integration of credit restoration and capital procurement. We focus on creating win-win partnerships that allow you to secure your business legacy without unnecessary financial risk. If you're ready to stop guessing and start growing, it's time to take the next step toward a stable financial future.

Secure your business funding with Koval Investments expert SBA assistance. Your vision for growth is achievable with the right partner by your side.

Frequently Asked Questions

What is the minimum credit score required for SBA loan assistance?

Lenders generally look for a FICO Small Business Scoring Service (SBSS) score of 155 or higher for 7(a) loans. On the personal side, a score of 680 or above is typically the benchmark for traditional SBA lenders. If your score is currently lower, professional SBA loan assistance can help you identify and dispute inaccuracies to improve your profile before you apply.

How long does the SBA loan application process typically take with professional help?

The timeline from initial submission to funding usually ranges between 30 and 90 days. Professional guidance accelerates this by ensuring your "lender-ready" package is complete on the first attempt, which prevents the common delays caused by missing or inconsistent documentation. The specific program and the lender's current volume also influence the final speed of your capital procurement.

Can I use SBA loan proceeds to buy out a business partner?

Yes, you can use an SBA 7(a) loan to finance a partner buyout if the transaction results in a 100% change of ownership or a significant shift in control. The business must demonstrate that its cash flow can comfortably support the new debt service. We help you structure these acquisitions to meet the specific equity and valuation requirements set by federal guidelines.

What is the difference between an SBA 7(a) and a 504 loan?

The 7(a) program is a versatile tool used for working capital, inventory, and debt refinancing with terms up to 10 years. In contrast, the 504 loan is designed for fixed assets like real estate or heavy equipment and offers long-term, fixed-rate financing. Choosing between them depends on whether your priority is operational flexibility or building long-term equity in tangible assets.

Does SBA loan assistance include help with credit repair?

Our comprehensive service integrates credit restoration with the funding process to ensure your profile is optimized for approval. We don't just point out credit issues; we actively work to resolve inaccuracies that could lead to higher interest rates or rejection. This dual approach ensures your business is positioned to secure the most efficient capital available in the 2026 market.

Are there SBA loans available with 0% interest?

The SBA does not offer 0% interest loans; however, we provide a separate 0% Interest Funding Solution that acts as a strategic bridge. This interest-free capital allows you to manage immediate operational needs while we work on your long-term SBA loan assistance strategy. It's an effective way to maintain momentum without the immediate burden of interest expenses during the optimization phase.

What documents are most critical for a successful SBA loan application?

The most vital documents include three years of business and personal tax returns, a current debt schedule, and detailed P&L statements. Lenders also require a specific "Use of Proceeds" statement and personal financial statements for any owner with at least a 20% stake. Accuracy across these documents is non-negotiable for proving your business's ability to repay the debt.

How much does it cost to get professional SBA loan assistance?

Costs for professional advisory services depend on the complexity of your financial restructuring and the specific capital needs of your business. We operate under a success-based philosophy, ensuring that our incentives are perfectly aligned with your funding results. A professional consultation is the best way to get a pragmatic assessment of the value and support required for your journey.