How to Fix Credit for SBA Loan Approval: A Strategic 2026 Guide for Business Owners

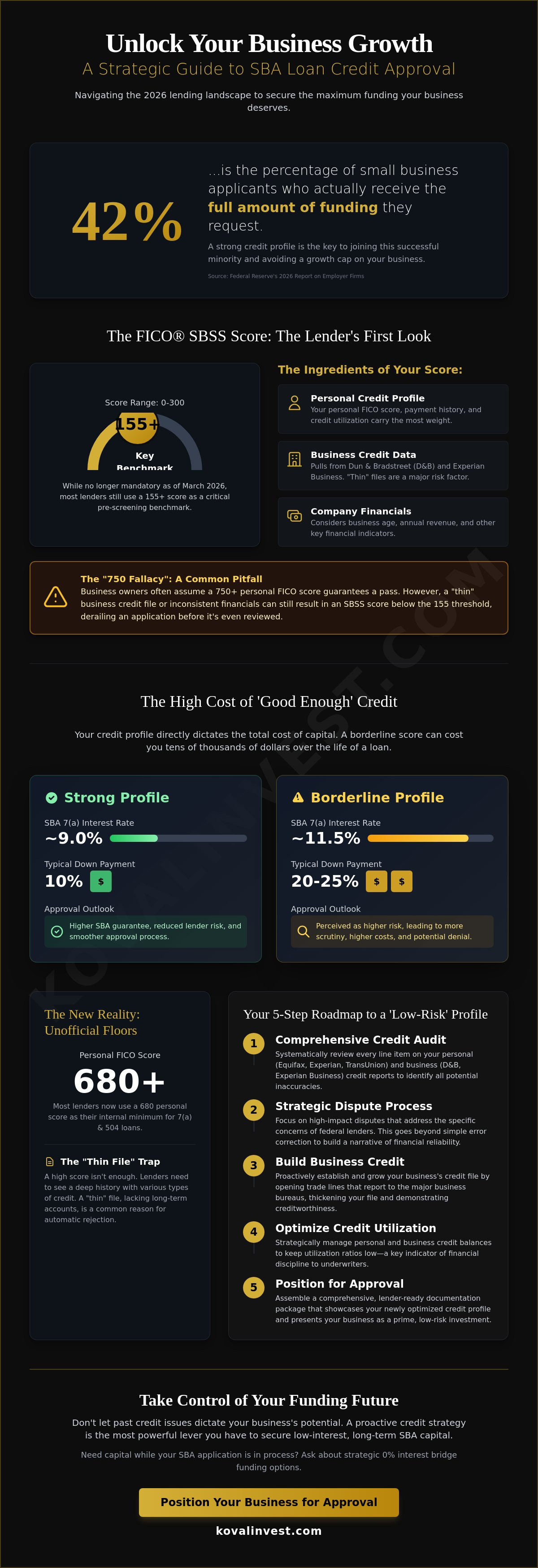

According to the Federal Reserve's 2026 Report on Employer Firms, only 42% of small business applicants actually receive the full amount of funding they request. It's a sobering reality for many owners who feel their growth is capped by a personal credit score that doesn't reflect their current success. If you're wondering how to fix credit for SBA loan approval, you're likely already feeling the pressure of complex documentation and the fear that a past mistake will lock you out of low-interest capital.

We understand that the path to securing an SBA 7(a) or 504 loan feels like a moving target, especially with recent shifts in how lenders evaluate your profile. This guide provides a clear roadmap to optimize your credit profile by focusing on the specific metrics that matter most in 2026. You'll learn how to navigate the March 2026 sunset of mandatory FICO SBSS requirements, satisfy individual lender standards, and position your business for the highest possible funding limits. We'll also cover strategic 0% interest alternatives if you need capital while your SBA application is in process.

Key Takeaways

- Identify why the 155-point FICO SBSS threshold remains the benchmark many lenders use to pre-screen applications, even with recent regulatory shifts.

- Learn exactly how to fix credit for SBA loan eligibility by focusing on high-impact disputes that address the specific concerns of federal lenders.

- Evaluate the high opportunity cost of passive waiting and why a proactive credit audit is essential for meeting rigorous SBA documentation standards.

- Explore strategic 0% interest bridge funding options that provide working capital without delaying your long-term SBA financing goals.

- Position your business as a low-risk borrower to secure the most competitive interest rates and maximize your total cost of capital savings.

Why Credit is the Primary Gatekeeper for SBA Loan Approval in 2026

The Small Business Administration (SBA) doesn't just look at your current bank balance; they look at your historical financial integrity. In the eyes of federal lenders, your credit profile serves as a proxy for your professional character and reliability. It's the most efficient way for a bank to determine if you'll treat their capital with the same respect you've shown past creditors. While insufficient cash flow remains the top reason for denial, a personal credit score below the lender's threshold is the second most common hurdle. If you're researching how to fix credit for SBA loan approval, you've already recognized that a high score is the key to unlocking the government's most attractive programs.

Your credit health directly dictates the total cost of capital. With the Prime Rate sitting at 6.75% as of June 2026, a lower credit score can push your variable interest rate for an SBA 7(a) loan as high as 11.5%. Conversely, borrowers with strong profiles can secure rates closer to 9%. Over a ten year term, that spread represents tens of thousands of dollars in interest. While the SBA 7(a) program is flexible for working capital and equipment, the 504 loan program often demands even more stability since it involves long term fixed assets and real estate. In either case, the lender's confidence is built on the foundation of your credit history.

The Minimum Credit Score Myth vs. Reality

Many entrepreneurs believe there's a hard "pass or fail" number for federal funding. While the SBA officially sunset the mandatory FICO SBSS score requirement on March 1, 2026, most lenders still maintain an unofficial floor of 680 for 7(a) and 504 loans. Lenders use these scores to justify lower down payment requirements. If your score is high, the bank feels comfortable with you putting 10% down. If it's borderline, they might demand 20% or 25% to offset the perceived risk, which can drain your company's liquidity at a critical time.

How Credit History Affects Your Loan Terms

The depth of your credit history is just as vital as the three digit number. "Thin" credit files, which lack a variety of accounts or long term history, often lead to automatic rejections regardless of the score. Lenders want to see how you handle different types of debt over several years. High credit scores also influence the SBA guarantee percentage. A stronger profile makes it easier for the lender to secure the maximum guarantee from the government, which reduces the bank's risk and improves your approval odds. Credit restoration is a strategic investment that yields dividends in the form of lower interest rates and reduced borrowing costs over the life of the loan. Understanding how to fix credit for SBA loan applications is the first step toward transforming your business from a risky prospect into a preferred borrower.

Understanding the FICO SBSS Score: The Hidden SBA Hurdle

The FICO LiquidCredit Small Business Scoring Service (SBSS) score is perhaps the most misunderstood metric in commercial lending. It's a sophisticated algorithm that aggregates data from your personal credit reports, business credit bureaus, and the financial health of your company to create a single number ranging from 0 to 300. This hybrid model is a core component of SBA 7(a) loan requirements, acting as a gatekeeper before a human underwriter ever sees your file. While the SBA officially sunset the mandatory use of this score for pre-screening on March 1, 2026, most lenders continue to use the 155-point threshold as a validated benchmark for risk assessment.

A common frustration for business owners is the "750 fallacy." You might maintain a 750 personal FICO score and still fail the SBSS check. This happens because the algorithm doesn't just care about your personal habits; it weights your business's credit footprint and operational data heavily. If your business is young or lacks established trade lines, the SBSS algorithm may produce a score below the 155-point floor. Understanding how to fix credit for SBA loan approval requires looking past your personal score and addressing the "thin" file of your business entity.

The Ingredients of Your SBSS Score

The SBSS calculation is a "black box," but we know the primary inputs. Personal FICO data typically carries the most weight, but the algorithm also pulls from Dun & Bradstreet (D&B) and Experian Business reports. Beyond credit, the model considers your business's age and annual revenue. A company with five years of steady growth will naturally outscore a startup with the same credit profile. If your business data is missing or inaccurate at the major bureaus, your SBSS score will suffer regardless of your personal financial discipline.

Optimizing the Hybrid Score

Fixing personal credit errors is the fastest way to see an immediate lift in your SBSS score. However, long term success depends on your business credit profile. You must ensure that your business has active "trade lines" with suppliers who report to D&B or Experian. If you're struggling to meet these benchmarks, seeking professional credit repair services can help you identify and correct the specific data points that are dragging your hybrid score down. Strategic optimization ensures your business data is accurately reported, making you a much more attractive candidate for federal funding. Mastering how to fix credit for SBA loan applications means treating your business credit with the same level of scrutiny as your personal finances.

Strategic Credit Restoration vs. Passive Waiting

Waiting for credit to heal on its own is a luxury most entrepreneurs can't afford. While traditional advice often suggests letting negative items age out over seven years, this passive approach carries a massive opportunity cost. In a market where the Prime Rate is 6.75%, delaying your expansion by even twelve months could mean missing out on a specific real estate opportunity or losing market share to a competitor who secured funding faster. When you're evaluating how to fix credit for SBA loan approval, you must treat your credit profile as a strategic business asset that requires active management rather than a static record that fixes itself over time.

SBA lenders are notoriously thorough during the underwriting process. They don't just look at your current three-digit score; they perform a deep "look-back" into the history of your accounts. A passive approach often leaves unresolved "dispute" flags or incorrectly reported balances that can trigger an automatic rejection during the pre-screening phase. Aligning your credit restoration with your SBA loan application timeline ensures that your profile is optimized exactly when the lender pulls your report. This proactive timing is especially critical for maintaining a competitive FICO SBSS score, which requires both personal and business data to be in peak condition simultaneously.

The Limitations of DIY Credit Repair

Self-filing disputes can often do more harm than good for a business owner. A common mistake is using generic "not mine" templates, which credit bureaus easily identify and flag as frivolous. For an SBA lender, seeing a history of unresolved disputes suggests financial instability. Furthermore, simply "deleting" an item is often less effective than "correcting" the history to show a positive resolution. Correcting data ensures the fix is permanent and won't reappear just as your loan moves to the final approval stage. Managing responses from three different bureaus while running a company is a complex task that frequently leads to missed deadlines and incomplete files.

The Value of Professional Financial Restructuring

Professional restoration goes beyond simple disputes; it involves a comprehensive audit to identify inaccuracies that the average owner misses, such as misreported credit limits or outdated public records. Our approach to Professional Credit Repair for Business Owners focuses on securing capital by aligning your profile with specific lender overlays. Experts understand the nuances of how different banks interpret credit events, allowing you to position your business as a "low-risk" borrower. By leveraging this insider knowledge, you can move through the how to fix credit for SBA loan process with much greater speed and certainty, turning a potential rejection into a successful funding event.

A 5-Step Roadmap to Fix Your Credit for SBA Eligibility

Achieving SBA eligibility requires a methodical approach that addresses both your personal and business credit identities. This roadmap outlines the technical process of how to fix credit for SBA loan approval by focusing on the specific variables that underwriters prioritize. By following these steps, you transform your profile from a liability into a strategic asset that supports your funding goals.

- Step 1: Perform a Comprehensive Credit Audit across all three bureaus to identify every reporting error.

- Step 2: Identify and Dispute Inaccuracies using high-impact evidence to ensure permanent removal or correction.

- Step 3: Strategically Reduce Credit Utilization to under 30% to demonstrate responsible debt management.

- Step 4: Establish and Season New Business Trade Lines to build a robust business credit footprint.

- Step 5: Monitor and Maintain the SBSS Score throughout the entire SBA application and closing process.

Auditing and Disputing Inaccuracies

The first stage of credit restoration involves a granular review of your Experian, Equifax, and TransUnion reports. You're looking for incorrect balances, outdated late payments, and duplicate accounts that can artificially inflate your debt load. When you identify an error, you must provide specific documentation, such as cancelled checks or bank statements, to the bureaus. They typically have a 30-day response window to verify or remove the item. For past credit blips that are accurate, prepare a detailed narrative explaining any extenuating circumstances. This context helps a human underwriter understand that a previous mistake doesn't reflect your current financial reliability.

Optimizing Your Debt-to-Credit Ratio

Lenders view high credit utilization as a sign of financial strain. If you need a quick point gain before submitting an application, the "Rapid Rescore" technique can update your credit report in just a few days rather than waiting for the standard monthly cycle. It's vital that you don't close old accounts during this time. Even if you don't use them, the age of those accounts is a major factor in your score. Prioritize paying down revolving debt on accounts that are closest to their limits to maximize the positive impact on your score. This tactical approach is a core part of how to fix credit for SBA loan requirements efficiently.

Building the Business Side of the File

Your business entity needs its own established history to satisfy the FICO SBSS algorithm. Start by registering for a D-U-N-S number and verifying that your business data is accurate with Dun & Bradstreet. You should ask your current vendors to report your on-time payments, as many don't do this automatically. Be mindful of UCC-1 filings, which indicate that other lenders have a claim on your assets. These filings are common in business, but they must be managed correctly to avoid appearing over-leveraged. If you need a professional partner to navigate these complexities, our team provides specialized credit repair services tailored for business owners seeking federal capital.

Leveraging Professional Capital Procurement for SBA Success

Fixing your credit is the essential foundation, but the ultimate objective is securing the capital necessary for your company's expansion. Once you've addressed technical errors and improved your utilization, you must pivot toward positioning your business as a low-risk borrower. SBA lenders prioritize stability, and a clean credit profile is the most compelling evidence of that trait. Moving from the initial research on how to fix credit for SBA loan approval to actually submitting a formal application requires a strategic bridge between your current financial state and your future funding goals.

The transition from credit restoration to capital access is rarely a straight line. It involves a methodical alignment of your personal financial history, your business's operational data, and the specific requirements of your chosen lender. By treating credit optimization as one component of a broader capital procurement strategy, you ensure that your business is not just "eligible" on paper, but truly ready for the rigors of federal underwriting. This holistic approach minimizes the risk of a late-stage denial and maximizes the funding limits you can realistically achieve.

The 0% Interest Funding Alternative

For many owners, the standard SBA timeline is too slow to meet immediate market demands. This is where 0% interest business funding serves as a strategic tool. Unlike federal loans that can take months to process, these unsecured solutions provide rapid access to capital. You can use this interest-free liquidity to pay down high-interest balances on other accounts, which instantly improves your debt-to-credit ratio and boosts your score. It's a proactive way to manage your profile while simultaneously funding operations. This dual-purpose strategy accelerates the process of how to fix credit for SBA loan eligibility by providing the cash needed to settle old obligations without the SBA's stringent collateral requirements.

Your Strategic Partner in Growth

Koval Investments acts as a seasoned advisor in this complex financial landscape. We move beyond simple credit repair to offer a comprehensive capital readiness assessment. Our "straight-talk" mentality ensures you understand your business valuation and funding potential before you ever step into a bank. We operate on a success-based philosophy, which means our objectives are perfectly aligned with your results. This partnership reduces the friction of the application process and ensures you don't miss out on low-interest capital due to easily correctable documentation errors. Transitioning from credit restoration to a fully funded expansion is a logical progression when you have a steady hand guiding the strategy.

Apply for a strategic credit and funding consultation with Koval Investments to begin your journey toward optimized eligibility and higher funding limits.

Transforming Your Financial Profile into a Strategic Growth Asset

Achieving SBA eligibility in 2026 requires more than just checking a box. It's about building a narrative of reliability through both personal and business credit channels. We've explored the necessity of meeting the 155-point SBSS threshold and the tactical steps required to audit and optimize your reports. Understanding how to fix credit for SBA loan approval is simply the first step in a larger journey toward sustainable expansion and lower costs of capital.

Since 2018, Koval Investments has functioned as a boutique partner for business owners who value precision and integrity. Our expertise in 0% interest funding and SBA assistance allows us to bridge the gap between your current credit status and your ultimate funding goals. We operate on a success-based philosophy because we believe a true partnership only exists when our wins are directly tied to yours. Our collaborative approach ensures you have a steady hand navigating the complexities of modern commercial finance.

Secure the funding your business deserves with our success-based credit optimization. Your business has the potential to scale; don't let a repairable credit profile stand in the way of that progress.

Frequently Asked Questions

What is the absolute minimum credit score for an SBA loan in 2026?

Most lenders require a minimum personal FICO score of 680 for SBA 7(a) and 504 loans. While the SBA allows for flexibility, scores below 650 typically require significant compensating factors like high collateral or exceptional cash flow. For smaller amounts, SBA Express loans may accept scores as low as 650. Microloans remain the most accessible option, with some lenders accepting scores between 575 and 640 depending on their specific risk model.

How long does it take to fix credit enough to qualify for an SBA loan?

The timeline to see results when learning how to fix credit for SBA loan eligibility typically ranges from three to six months. This duration accounts for the 30 day investigation window credit bureaus require for disputes and the subsequent time for lenders to update their records. If you utilize a rapid rescore through a lender, you might see specific point gains in just a few days. However, a full profile optimization usually takes several months to finalize.

Does the SBA look at my personal credit or just my business credit?

Lenders evaluate both profiles because your personal financial history serves as a primary indicator of how you will manage business debt. Even though the SBA sunset the mandatory FICO SBSS requirement on March 1, 2026, most banks still use a hybrid model that blends your personal score with business data. A strong personal score cannot always compensate for a thin business credit file. This makes it necessary to address both identities simultaneously during the restoration process.

Can I get an SBA loan with a recent bankruptcy if I fix my credit?

Securing an SBA loan with a recent bankruptcy is difficult but possible if the discharge occurred several years ago and you have since rebuilt a positive credit history. Most lenders require a minimum of three years since discharge for a Chapter 7 filing. You must provide a detailed written explanation of the circumstances. You must also demonstrate that the business currently maintains a Debt Service Coverage Ratio of at least 1.15x to prove repayment ability.

What is the FICO SBSS score and why is it so important?

The FICO LiquidCredit Small Business Scoring Service (SBSS) is a hybrid score ranging from 0 to 300 that pre-screens 7(a) loan applications. It aggregates personal credit reports, business bureau data, and company financial records into a single risk metric. Although the mandatory requirement ended in early 2026, many lenders still use the 155 point threshold as their internal benchmark. This score determines if an application should move to human underwriting or receive an automatic denial.

How much does professional credit repair for business owners cost?

The investment for credit restoration varies based on the complexity of your file and the specific inaccuracies that require resolution. Rather than focusing on a fixed price, business owners should evaluate the service based on the potential interest savings a higher score provides. Since SBA loan rates are tied to the Prime Rate, which is 6.75% as of June 2026, moving into a lower risk tier can save your company thousands of dollars over the life of the loan.

Will disputing items on my credit report hurt my SBA application?

Active disputes can stall your application because underwriters cannot accurately assess your risk while account data is in flux. It is essential to resolve all disputes and have the dispute notation removed from your credit reports before the lender pulls your final file. A strategic approach to how to fix credit for SBA loan approval ensures that all corrections are finalized and verified well before you submit your formal documentation to the bank.

What happens if my SBA loan is denied due to credit?

If your application is denied, you have the right to receive a specific explanation of the credit factors that led to the decision. You can use this information to create a targeted restoration plan or explore alternative funding options. Many owners pivot to 0% interest business funding or working capital solutions to maintain operations. This provides the necessary time to optimize their profile for a future SBA re-application without halting their business growth.