Commercial Real Estate Financing Options: A Strategic Comparison for 2026

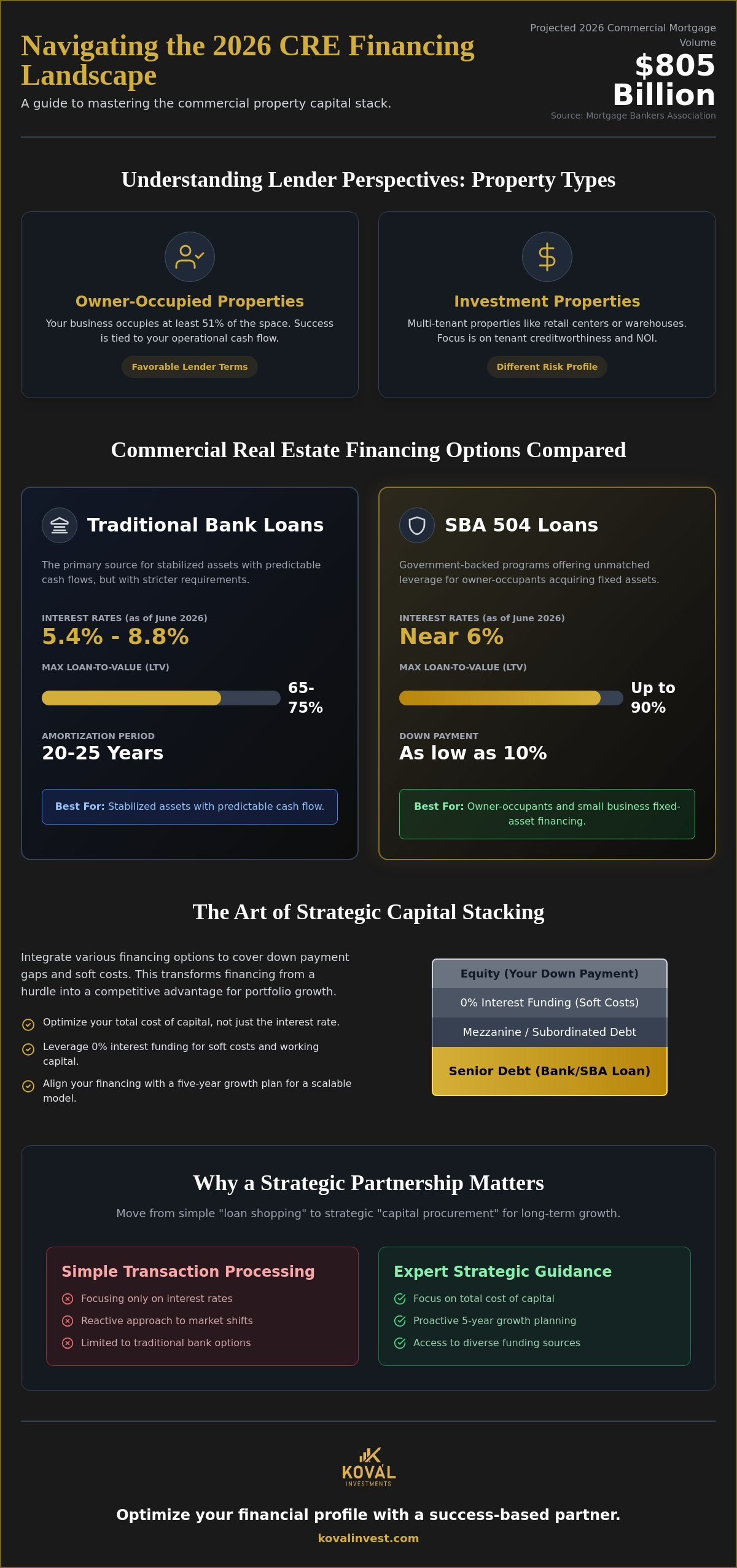

What if the most expensive part of your next acquisition isn't the interest rate, but the way you've structured your capital stack? With the Mortgage Bankers Association forecasting commercial mortgage volumes to hit $805 billion this year, the competition for the best commercial real estate financing options is fiercer than ever. You likely feel the pressure of interest rates for conventional loans hovering between 5.4% and 8.8% while traditional lenders tighten their credit requirements. It's frustrating when high debt service coverage ratios eat into your cash flow and slow your growth.

We understand that securing capital shouldn't feel like a gamble against the market. This guide will help you master the complex landscape of commercial property capital by comparing traditional, federal, and alternative financing strategies. You'll learn how to qualify for SBA 504 loans with rates currently near 6%, identify low-cost capital sources, and find a strategic partner to optimize your financial profile. We'll break down the nuances between conventional and government-backed lending to ensure your next move is both profitable and sustainable.

Key Takeaways

- Identify why 2026 is a pivotal year for strategic refinancing as many existing commercial loans approach their maturity deadlines.

- Compare the structural differences between traditional bank mortgages and specialized SBA programs to determine the most cost-effective path for your acquisition.

- Learn how to optimize critical lender metrics like Debt Service Coverage Ratio (DSCR) to improve your qualification odds and interest rates.

- Master the art of capital stacking by integrating various commercial real estate financing options with 0% interest funding to cover soft costs and down payment gaps.

- Discover the value of a success-based partnership that aligns your financial growth with expert strategic guidance rather than simple transaction processing.

Understanding the 2026 Commercial Real Estate Financing Landscape

Commercial real estate (CRE) financing is the strategic acquisition of capital used to purchase, develop, or refinance income-producing properties and owner-occupied business locations. While many view it as a simple transaction, 2026 has introduced a significant shift in how these deals are structured. A massive wave of debt originated during previous low-rate cycles is hitting a maturity wall, forcing owners to seek innovative commercial real estate financing options to protect their equity. Strategy beats luck in this environment.

This reality requires a move away from "loan shopping" toward "capital procurement." Instead of merely comparing interest rates from a few local banks, successful operators now focus on the total cost of capital and the flexibility of the terms. The primary objectives remain consistent: building equity, capturing tax advantages like depreciation, and ensuring operational stability. However, the path to achieving these goals now demands a more sophisticated approach to how you source and stack your funding. To understand the foundational mechanics, reviewing Commercial mortgage basics helps clarify how lenders evaluate collateral and risk.

Owner-Occupied vs. Investment Properties

Lenders view risk through two distinct lenses based on who uses the building. For owner-occupied properties, where your business occupies at least 51% of the space, lenders often offer more favorable terms because the property's success is tied to your operational cash flow. Building equity in your own location stabilizes your long-term occupancy costs and creates a tangible asset for your balance sheet. It's a foundational step for business longevity.

Investment properties, such as multi-tenant retail centers or industrial warehouses, carry a different risk profile. Here, the lender prioritizes the creditworthiness of your tenants and the property’s ability to generate net operating income. Understanding these differences is essential for determining which commercial real estate financing options fit your specific asset class and risk tolerance.

The Role of Capital Procurement in Portfolio Growth

Capital procurement is a holistic method of securing funds that looks beyond the balance sheet of a single institution. When you adopt this mindset, you aren't just looking for a mortgage; you're building a foundation for long-term expansion. Professional consulting plays a vital role here by identifying funding sources that traditional banks might miss, such as specialized bridge loans or federal programs.

Strategic planning ensures that your current debt doesn't prevent you from taking advantage of future opportunities. By aligning your financing with a five-year growth plan, you create a scalable model for portfolio development. This proactive approach transforms financing from a hurdle into a competitive advantage for your business.

Comparing Traditional Bank Loans vs. Specialized Investment Funding

Selecting between traditional and specialized commercial real estate financing options depends entirely on your speed requirements and long-term equity goals. Conventional bank loans remain the primary source for stabilized assets with predictable cash flows. As of June 2026, conventional mortgage rates range from 5.45% to 8.75%, depending on the borrower’s strength and the property type. These loans typically feature 20 to 25-year amortization periods. Interestingly, many borrowers now favor five- and seven-year loan structures because they expect long-term rates to decline further by the end of the decade. Lenders are maintaining strict underwriting standards, often requiring a Loan-to-Value (LTV) ratio between 65% and 75%. While some exceptional properties might reach 80% LTV, most institutions are cautious, particularly with office assets where delinquency rates hit 12.34% in early 2026. For large-scale investments, CMBS (Conduit) loans provide non-recourse debt with rates in the mid-6% to low-7% range, though they come with rigid prepayment penalties.

SBA Loans: The Gold Standard for Small Business Owners

For owner-occupants, government-backed programs offer unmatched leverage. The SBA 504 loans are ideal for fixed-asset financing. They allow for down payments as low as 10%, with rates for the CDC portion currently around 5.9% to 6.1%. This structure preserves your working capital for operational needs rather than tying it up in real estate equity. The SBA 7(a) program serves as a versatile tool for both real estate and general business use, though rates are slightly higher, typically between 7.75% and 9.75%. Navigating these programs requires precision, making professional SBA loan assistance a critical resource for first-time applicants who want to avoid common processing delays.

Alternative Real Estate Investment Funding

When speed is more important than the interest rate, Hard Money or Bridge loans fill the gap. These are often used for "fix-and-flip" projects or when a property isn't yet stabilized enough for a bank. Private money and debt funds offer flexibility for investors who don't fit into the rigid boxes of traditional institutions. You trade higher interest rates for the ability to close a deal in days rather than months. Choosing among these alternative commercial real estate financing options allows you to stay competitive in a fast-moving market where traditional banks may be too slow to respond. Finding the right balance between these paths is where strategic planning adds the most value to your portfolio.

Critical Qualification Metrics: LTV, DSCR, and the Credit Score Factor

Lenders prioritize risk mitigation above all else. While the physical asset serves as collateral, the strength of your financial metrics determines the cost and availability of your capital. When evaluating commercial real estate financing options, institutions rely on three primary pillars: the Loan-to-Value (LTV) ratio, the Debt Service Coverage Ratio (DSCR), and your credit profile. Understanding these numbers before you walk into a meeting allows you to negotiate from a position of strength rather than desperation.

The "Credit Score Gap" is a silent profit killer in commercial lending. A 50-point difference in your score doesn't just change your approval odds; it fundamentally alters your interest rate. Over a 20-year term, even a 1% increase in your rate can cost hundreds of thousands of dollars in cumulative interest. Financial optimization is not a one-time event but a strategic prerequisite for securing the best possible terms in a selective 2026 market.

Calculating Your DSCR and LTV

The Debt Service Coverage Ratio (DSCR) is the primary metric lenders use to gauge property cash flow health. You calculate it by dividing your Net Operating Income (NOI) by your total annual debt service. Most lenders currently require a minimum DSCR of 1.25x, meaning the property must generate 25% more income than the cost of the mortgage. For riskier assets like under-performing office buildings, lenders may push this requirement to 1.35x or higher to provide a larger safety margin.

LTV limits vary significantly by asset class. While industrial and multifamily properties often qualify for 75% LTV, office properties are currently capped between 60% and 65% by most traditional lenders. If you're looking at specialized assets like medical office buildings, you might see LTVs between 65% and 75%. Life insurance company loans, known for their conservative nature, often max out at 55% to 60% LTV.

Credit Optimization as a Financial Strategy

Many entrepreneurs overlook the power of credit repair as a tool for capital procurement. Disputing inaccuracies on your business and personal reports can yield rapid score improvements that directly lower your borrowing costs. Improving your score expands your commercial real estate financing options by making you eligible for lower-cost conventional and SBA programs that would otherwise be out of reach.

Preparing your financial profile for a 2026 loan application should include a thorough audit of your current liabilities and tax returns. Ensure your records clearly demonstrate consistent cash flow and a healthy balance sheet. By aligning your financial profile with lender expectations before you apply, you reduce the friction of the underwriting process and position your business for a successful closing.

Strategic Capital Stacking: Leveraging 0% Interest and Working Capital

A capital stack is the layering of different types of debt and equity used to fund a property acquisition. While the senior mortgage covers the majority of the purchase price, the "gap" often creates a hurdle for investors, especially as lenders cap LTV ratios in a selective 2026 market. This is where strategic commercial real estate financing options like unsecured working capital and 0% interest lines become essential tools. By combining these sources, you can fulfill down payment requirements or cover closing costs without diluting your ownership or exhausting your personal cash reserves. Using non-dilutive capital ensures you retain full control over the asset’s appreciation while maintaining a healthy liquidity position for your business operations.

The 0% Interest Funding Solution

Accessing 0% interest business funding allows you to manage initial investment stages with maximum efficiency. You can use these funds for soft costs such as appraisals, legal fees, and environmental reports that often aggregate into significant out-of-pocket expenses before a loan even closes. Timing is everything. By strategically sequencing your credit applications, you can secure higher funding limits without triggering the red flags that simultaneous inquiries might cause. This approach contrasts sharply with high-interest bridge loans. While a bridge loan might carry double-digit rates, 0% APR lines provide a cost-free window to stabilize the property or finalize long-term financing, saving you thousands in early-stage debt service.

Working Capital for Property Optimization

Liquidity is the engine of property optimization. Using working capital for business acquisition or property upgrades can significantly boost an asset’s valuation and your resulting DSCR. Consider a "value-add" scenario where you use low-cost working capital to fund tenant improvements for a new lease. The resulting increase in Net Operating Income doesn't just pay back the capital; it increases the overall appraisal value of the building, making a future refinance much more lucrative. This hybrid funding approach transforms a standard acquisition into a high-performance investment by leveraging the right type of capital for the right task. If you're looking to optimize your next project, our 0% Interest Funding Solution can provide the flexible capital needed to bridge your next down payment gap.

Securing Your Capital: Why a Strategic Partnership Matters

A loan officer is an employee of a financial institution whose primary loyalty remains with the bank's specific underwriting criteria. In contrast, a strategic financial partner acts as your advocate, analyzing your entire business ecosystem to identify the most advantageous commercial real estate financing options. This distinction is vital in 2026, a year where credit remains selective and loan terms are increasingly nuanced. At Koval Investments, we operate on a success-based philosophy. This approach ensures our objectives are perfectly aligned with yours. We don't view ourselves as a distant service provider, but as a steady hand helping you navigate a complex financial landscape.

Strategic planning and professional business valuations are the cornerstones of a successful acquisition. Before you sign any loan documents, you must understand the true market value of your target asset and how that debt will interact with your long-term cash flow. Over-leveraging based on faulty data is a common mistake that can stifle a portfolio for years. By integrating valuations into the procurement process, you ensure that every dollar borrowed is a deliberate step toward expansion rather than a burden on your balance sheet. View capital procurement as an ongoing relationship for portfolio growth rather than a one-time transaction.

Consulting Beyond the Transaction

For investors looking at property-heavy business acquisitions, M&A consulting provides a layer of protection that a standard bank cannot offer. These deals are complex because they require valuing both the operational entity and the underlying real estate. A boutique advisory firm provides a "straight-talk" mentality, offering unvarnished feedback on deal viability. This ensures you aren't over-leveraging based on optimistic projections that don't account for the 2026 market's reality. Our collaborative approach focuses on the long-term health of your business, ensuring that the capital you secure today supports the growth you envision for tomorrow.

Next Steps for Your 2026 Investment Strategy

Your journey toward mastering commercial real estate financing options began with credit optimization and moved through the technicalities of LTV and DSCR. The final step is execution through a partner who understands the nuances of capital stacking. Our success-based engagement model means there is no financial risk to you during the consulting phase. We're equally invested in your success, projecting a sense of quiet confidence and forward-thinking expertise throughout the process. If you're ready to optimize your financial profile and secure the low-cost capital your business deserves, now is the time to move from planning to action. Contact us today for a professional consultation and let's build a capital strategy that scales with your ambitions.

Strategic Capital Procurement: Your Path to 2026 Expansion

The 2026 market doesn't reward passive loan shopping; it rewards those who treat capital as a strategic asset. You've learned that mastering metrics like DSCR and LTV, while integrating innovative capital stacking techniques, is the most effective way to navigate high interest rates. By carefully comparing all commercial real estate financing options, you're able to bridge down payment gaps and protect your equity for future acquisitions.

Success in this landscape depends on having an insider who understands the day-to-day realities of business ownership. Koval Investments provides a success-based philosophy with no upfront risk, ensuring our interests are always aligned with your growth. We offer specialized expertise in 0% interest funding solutions and combine national reach with boutique-level personal service. It's about finding a win-win scenario that scales with your ambitions.

Secure your strategic capital consultation with Koval Investments today. We're ready to help you optimize your financial profile and build a legacy that lasts.

Frequently Asked Questions

What are the main commercial real estate financing options for investors in 2026?

The primary commercial real estate financing options in 2026 include conventional bank mortgages, SBA 504 and 7(a) programs, and CMBS loans. Specialized investors also leverage alternative bridge loans and 0% interest funding to remain competitive in a selective market. Each path carries distinct requirements for leverage and interest rates. It's essential to align the funding type with your specific property goals, occupancy status, and long-term exit strategy to maximize your return.

How does a business credit score affect commercial real estate loan rates?

Your credit score serves as a primary risk indicator that determines the interest rate spread a lender applies to your loan. A score improvement of just 50 points can move you from a high-interest alternative tier into a low-cost conventional program. This shift can fundamentally change your property's cash flow by reducing monthly debt service obligations. It also increases your long-term equity growth potential by lowering the total cost of capital over the life of the loan.

Can I use 0% interest funding for a commercial real estate down payment?

You can strategically use 0% interest business funding to cover down payment gaps or soft costs during the acquisition phase. This approach allows you to preserve your liquid cash for operational needs while meeting the lender’s equity requirements. It's a non-dilutive way to stack capital. By using these funds, you maintain full ownership and control over the asset’s appreciation without paying immediate interest on that portion of the debt, significantly improving your day-one ROI.

What is the minimum DSCR required for a commercial mortgage?

Most lenders require a minimum Debt Service Coverage Ratio (DSCR) of 1.25x to ensure the property generates sufficient income to cover its debt. In the current selective market, preferred pricing is often reserved for properties with a DSCR between 1.25x and 1.35x. For office assets, which are under persistent stress in 2026, some conduit lenders may require even higher ratios. This ensures a larger safety margin to protect the lender against potential tenant vacancies or market shifts.

How long does it take to secure real estate investment funding?

Securing traditional real estate investment funding usually takes between 45 and 90 days from the initial application to the final closing. The timeline depends heavily on the complexity of the property appraisal and the speed of the environmental reports. If you require capital more quickly for a time-sensitive acquisition, alternative bridge or hard money loans can often close within 10 to 14 business days. However, you must weigh that speed against the higher interest rates these options carry.

Is an SBA loan better than a conventional bank loan for real estate?

SBA loans are often superior for owner-occupants because they allow for lower down payments of 10% and offer long-term fixed rates. Conventional bank loans are generally better for investors who don't occupy the building or for those seeking non-recourse debt on larger assets. Choosing the right path requires evaluating your specific business needs against the LTV and DSCR constraints. A strategic partner can help you determine which program offers the best balance of leverage and cost.

What is the typical LTV for a commercial property loan?

Typical Loan-to-Value (LTV) ratios for commercial properties currently range from 65% to 75% for stabilized assets. Multifamily and industrial properties often qualify for the higher end of that range due to their perceived stability in the 2026 economy. Conversely, life insurance company loans and CMBS office loans are more conservative. They often cap leverage at 55% to 60% to protect against market fluctuations, requiring borrowers to bring more equity to the closing table for those specific deals.

How can credit repair services help me get a better commercial loan?

Credit repair services help you qualify for better commercial real estate financing options by removing inaccuracies that unfairly suppress your score. A higher score reduces the lender's perceived risk, which directly translates to lower interest rates and more flexible terms. By optimizing your credit profile before applying, you position yourself as a top-tier borrower. This proactive step ensures you gain access to the most competitive capital in the market while avoiding the high costs associated with subprime lending.