How to Secure Commercial Real Estate Financing Options: A Strategic 2026 Guide

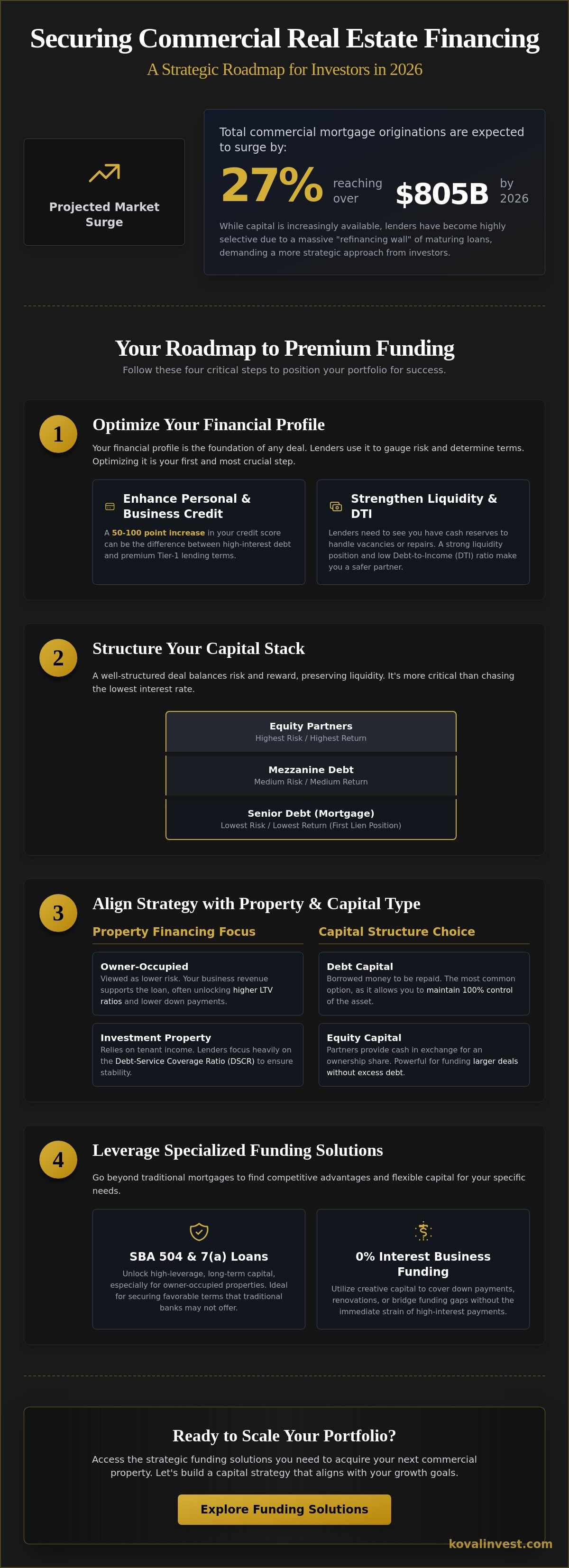

Did you know that total commercial mortgage originations are expected to surge by 27% to over $805 billion in 2026? While capital is increasingly available, the massive "refinancing wall" of maturing loans means lenders have become highly selective about their partners. Securing the best commercial real estate financing options requires more than just a solid property; it demands a tactical understanding of how to position your business for success.

You likely recognize that the barrier to entry for traditional bank loans remains high, and the complexity of modern capital stacks can feel like a moving target. It's frustrating to feel that your credit history or a lack of insider knowledge is holding you back from prime opportunities. This guide delivers a comprehensive roadmap to identifying, qualifying for, and securing the most competitive funding available in today's market. We'll explore how to leverage business credit, navigate SBA programs, and utilize creative capital solutions to ensure your next acquisition is a win-win for your portfolio.

Key Takeaways

- Understand how to structure your capital stack to balance risk and maximize the potential of every property acquisition.

- Identify the most competitive commercial real estate financing options by aligning your specific business goals with today's market realities.

- Learn why optimizing both personal and business credit is the critical first step to unlocking premium funding rates.

- Discover the strategic advantages of SBA 504 and 7(a) loans for securing high-leverage, long-term capital.

- Find out how to utilize 0% interest funding solutions to handle down payments or renovations without traditional financial strain.

Navigating the 2026 Commercial Real Estate Financing Landscape

Commercial real estate financing is the fundamental mechanism used to acquire, develop, or refinance income-producing property. It's the engine that drives portfolio growth. In 2026, the market is undergoing a notable transition. While the Mortgage Bankers Association forecasts that total mortgage originations will increase by 27% to over $805 billion, traditional banks have maintained strict lending standards. This environment has pushed many investors toward non-bank lenders and private capital sources. You now have a wider array of commercial real estate financing options, but accessing them requires a clear understanding of your position in the market. Identifying the right path is a strategic sequence that begins with your specific business goals.

Success starts with understanding the capital stack. This is the financial hierarchy that outlines where debt and equity sit in relation to the property's value. At the foundation is the senior debt, often a Commercial mortgage, which holds the first lien position. Above this, you might find mezzanine debt or equity partners. Choosing the right structure is often more critical than simply chasing the lowest interest rate. A well-structured deal preserves your liquidity and provides the flexibility needed to manage the "refinancing wall" of maturing loans currently hitting the market.

The Difference Between Owner-Occupied and Investment Property

Lenders evaluate risk differently based on who occupies the building. If your business is the primary tenant, you're seeking owner-occupied financing. Lenders often view these deals as lower risk because your business revenue supports the loan. This can unlock higher Loan-to-Value (LTV) ratios, often allowing you to put less money down. Conversely, investment properties rely on third-party tenants. Lenders will focus intensely on the Debt-Service Coverage Ratio (DSCR). They want to see that the property's net operating income can comfortably cover the debt, even if vacancies occur.

Debt vs. Equity Capital: Which Fits Your Growth?

Debt capital is borrowed money that must be paid back with interest over a set period. It's the most common way to fund real estate because it allows you to maintain total control of the asset. Equity capital is different; it involves bringing on partners who provide cash in exchange for a share of the ownership and future profits. This can be a powerful way to fund larger deals without taking on excessive debt. To optimize your strategy, you might consider how 0% interest business funding can bridge the gap. It provides a way to cover down payments or renovation costs without the immediate pressure of high-interest payments, keeping your capital stack lean and efficient.

Optimizing Your Financial Profile to Unlock Premium Funding

Many investors assume they're locked out of the best commercial real estate financing options because their credit score doesn't hit a specific threshold. This common misconception often prevents qualified owners from pursuing lucrative deals. Your financial profile isn't static; it's a variable you can control. Adopting a "funding-ready" mindset means viewing your personal credit as a strategic asset. Even for large commercial transactions, your personal history serves as the primary indicator of how you handle financial obligations. Lenders use it to gauge the level of risk they're assuming by partnering with you.

Lenders also scrutinize your Debt-to-Income (DTI) ratio and liquidity. They want to see that you have enough cash on hand to weather seasonal dips or unexpected repairs. A strong liquidity position suggests stability, making you a safer bet for a high-leverage loan. Optimizing these figures isn't just about getting a "yes" from a bank. It's about building a foundation for long-term operational efficiency. When your financial house is in order, you gain the leverage to negotiate better terms and larger loan amounts.

The Role of Professional Credit Restoration

Professional credit restoration is a powerful lever for lowering your cost of capital. Identifying and disputing inaccuracies on your report can lead to an immediate improvement in your standing. A 50-to-100 point score jump often marks the difference between high-interest debt and tier-1 lending terms. Credit repair is the foundational step for any real estate capital procurement. If you're looking to maximize your borrowing power, starting with a comprehensive credit audit is a prudent move that yields tangible returns.

Establishing a Fundable Business Entity

Structuring your holdings through a dedicated LLC is essential for limiting personal liability. This separation protects your personal assets while allowing the business to build its own credit identity. To ensure your entity is fundable, follow these steps:

- Register your business with a unique tax ID (EIN).

- Maintain a dedicated business bank account with clean, consistent transactions.

- Ensure your business address and phone number are listed in professional directories.

Consistent financial reporting is equally vital. It creates a paper trail that proves your business's health, which is a prerequisite for more complex funding like the SBA 504 loan program. Proper entity structure and clean books also streamline the path to securing SBA loan assistance when you're ready to scale your portfolio. By decoupling your personal and business credit profiles, you create a more resilient financial structure that appeals to both traditional and private lenders.

Comparing SBA Loans, Traditional Mortgages, and Specialized Capital

Identifying the right vehicle from the available commercial real estate financing options is a matter of strategic alignment. For many small to mid-sized firms, the SBA 7(a) and 504 programs represent the gold standard. They offer long-term stability that traditional bank loans often can't match. However, if you're dealing with a distressed asset or a tight closing deadline, specialized capital like hard money or bridge loans might be necessary. These options provide the speed required to secure a property before a conventional lender can even finish the appraisal. The key is to match your loan term to your exit strategy. If you plan to renovate and sell within 18 months, a high-interest bridge loan is a tool, not a burden. If you're holding the asset for 20 years, a fixed-rate government-backed loan is the logical choice.

The 2026 market demands a diversified approach to the capital stack. While institutional banks remain cautious, private debt funds have stepped in to fill the gap for unique projects. This shift means that your "win-win" scenario might involve a combination of different funding sources. You might use a bridge loan to acquire and stabilize a property, then transition into long-term permanent financing once the asset's value is proven. This methodical progression protects your equity while ensuring the project remains viable through every phase of its lifecycle.

SBA 504 vs. Conventional Bank Loans

The SBA 504 loan program is uniquely structured to facilitate the purchase of fixed assets. It utilizes a 50/40/10 framework: a private lender provides 50% of the funding, a Certified Development Company (CDC) covers 40% through an SBA-backed debenture, and the borrower contributes just 10%. This is a massive advantage over conventional loans, which typically require 20% to 30% down. Conventional rates are also often variable; whereas, the SBA portion of a 504 loan is fixed for the life of the term. This makes it ideal for industrial warehouses, medical offices, and retail spaces where long-term cost certainty is paramount.

Leveraging Working Capital for Real Estate Operations

Sometimes, the most effective way to move a deal forward is by using working capital for business acquisition or property improvements. Unsecured working capital has a significant speed advantage. It doesn't require a traditional real estate lien, which can take months to clear. This makes it a perfect solution for covering "soft costs" like architectural fees or minor renovations that increase a property's value before a permanent refinance. Unlike construction loans that offer interest-only draw periods but involve heavy oversight, revolving capital lines provide the flexibility to deploy funds exactly when your project demands it. This agile approach ensures your real estate operations never stall due to a lack of immediate liquidity.

How to Secure Commercial Real Estate Capital: A Step-by-Step Roadmap

Securing capital requires a tactical sequence that transforms a property vision into a funded reality. It begins with a comprehensive audit of both your personal and business credit profiles. This isn't a mere glance at a score; it's a deep dive to ensure no inaccuracies or outdated marks hinder your progress. Next, define your real estate strategy by projecting a realistic ROI. Lenders don't just fund buildings. They fund business cases. Once your strategy is clear, prepare a professional executive summary and financial prospectus. This document acts as your "insider" resume, proving to lenders that you've accounted for every variable.

Identifying the "funding gap" is the fourth critical step. This involves calculating the difference between your available cash and the total project cost. At this stage, you'll select a mix of commercial real estate financing options to bridge that gap. You might combine a senior mortgage with a 0% interest line to cover soft costs or renovations. Finally, navigate the underwriting process with total transparency. Engaging a strategic partner for advisory services can help you anticipate lender questions before they become roadblocks. If you're ready to start this sequence, you can request a strategic funding consultation to map out your specific path.

Preparing Your Documentation for Underwriting

Underwriting is where your preparation meets scrutiny. You'll need to provide the "Big Three": three years of federal tax returns, current year-to-date P&L statements, and updated personal financial statements. If you're acquiring a property-heavy entity, a professional business valuation provides the objective data lenders need to justify the loan amount. Maintaining proactive and transparent communication with your loan officer ensures that minor questions don't turn into deal-killing delays.

The Closing Process and Beyond

The final stretch includes the appraisal, title search, and environmental review phases. These steps verify the asset's value and ensure no legal or ecological liabilities exist. When you receive a commitment letter, it will likely contain "conditions" like updated insurance binders or proof of equity. Handle these immediately to keep the momentum. Closing isn't just the end of a deal; it's the start of a relationship. By performing well on your first project, you build the credibility needed to fund your next three properties with the same lender.

Scaling Your Portfolio with Koval Investments’ Strategic Funding

Koval Investments operates as a seasoned strategic partner rather than a distant lender. Our "insider" approach combines credit optimization with expert capital procurement to ensure you access the most competitive commercial real estate financing options. We don't just hand you a list of products; we work alongside you to prepare your financial profile for the highest level of funding. This methodical process minimizes financial risk by addressing credit report inaccuracies and liquidity concerns before you ever step into a bank's boardroom. This strategic alignment is what separates a successful acquisition from a financial burden. By understanding the full range of commercial real estate financing options, you can structure a capital stack that prioritizes growth over interest payments.

Our success-based philosophy means our objectives are directly aligned with yours. We focus on results that provide tangible value, moving beyond simple transactions to build long-term relationships. This is particularly vital in a market where traditional banks remain selective. By leveraging our deep industry expertise, you gain a steady hand to guide you through complex financial landscapes. It's a collaborative effort designed to create a win-win scenario for your growing portfolio.

The 0% Interest Advantage for Real Estate

One of the most powerful tools in our arsenal is the 0% interest funding solution. This capital serves as an efficient bridge, allowing you to cover down payments or renovation costs without the immediate pressure of high-interest debt. By using interest-free capital for these "soft costs," you preserve your equity and keep your primary mortgage focused on the asset's core value. This strategy is something institutional banks simply don't offer. You're invited to explore your funding eligibility through a professional consultation where we can determine how these creative tools fit your specific roadmap.

Strategic Advisory for Long-Term Expansion

Our commitment to your success extends into strategic planning and mergers and acquisitions consulting. For investors targeting property-heavy businesses or corporate acquisitions, our business valuation services provide a precise understanding of an asset's true worth. This data-driven approach ensures your capital structure supports long-term goals rather than just immediate needs. We want to ensure that every deal you close strengthens your position for the next one.

We view our role as that of a mentor and trusted advisor. M&A consulting facilitates successful transitions, helping you navigate the nuances of complex deals with confidence. This pragmatism and "straight-talk" mentality ensure that every move you make is intentional and focused on operational efficiency. Scaling a portfolio is a journey, and having a deliberate partner ensures you're prepared for every opportunity that 2026 presents.

Strategic Capital for Your 2026 Portfolio Growth

Securing the right commercial real estate financing options in 2026 is a matter of precision rather than luck. You've seen that success begins with a rigorous audit of your financial profile and ends with a capital stack that balances risk and reward. Whether you're navigating the complexities of the SBA 504 program or using 0% interest funding to bridge a down payment gap, the goal is always long-term operational efficiency.

Koval Investments acts as your seasoned strategic partner throughout this journey. We've facilitated over $500M in capital for our clients, specializing in success-based solutions that align our goals with yours. Our team of 0% interest funding experts is ready to help you navigate the current market with confidence and clarity. We believe in a collaborative approach where our success is tied directly to your results.

Don't let the barrier of traditional bank requirements stall your progress. It's time to take the next step toward a more resilient and scalable portfolio. Secure your commercial real estate capital with Koval Investments today. We're here to ensure your next acquisition is a win-win for your business.

Frequently Asked Questions

What is the minimum credit score required for commercial real estate financing?

Most lenders look for a score of at least 660 to 680 for SBA-backed loans, while conventional banks often prefer 700 or higher. A higher score directly translates to more favorable commercial real estate financing options and lower interest rates. If your score is currently below these marks, professional credit restoration is a vital first step to unlocking competitive capital.

Can I use an SBA loan to purchase a purely residential investment property?

No, you cannot use an SBA loan for a purely residential investment property like a single-family rental or a standard apartment complex. SBA programs require the borrowing business to occupy at least 51% of the square footage for existing buildings. These loans are designed to support owner-occupied business operations rather than passive real estate investing.

How much of a down payment is typically required for a commercial loan in 2026?

In 2026, the down payment requirement is typically 10% for SBA 504 loans and between 20% to 30% for conventional commercial mortgages. The exact amount depends on the property type, your financial profile, and the lender's current risk appetite. High-leverage options are generally reserved for strong sponsors with "funding-ready" financial profiles.

What is the difference between a bridge loan and a traditional commercial mortgage?

A bridge loan is a short-term solution, usually lasting one to three years, designed for quick acquisitions, renovations, or property stabilization. Traditional mortgages are long-term instruments with lower interest rates meant for permanent financing. Many investors use bridge loans to secure an asset quickly before refinancing into a long-term mortgage once the property's value has increased.

Is it possible to secure real estate funding with 0% interest?

Yes, it's possible to secure 0% interest funding for specific business purposes like renovations, soft costs, or down payment assistance. While traditional institutional banks don't offer these commercial real estate financing options, specialized strategic partners can facilitate these solutions. This allows you to preserve your cash flow and equity during the critical early phases of a project.

How does professional credit repair impact my business loan interest rates?

Professional credit repair can significantly lower your interest rates by moving you into a higher lending tier. For example, jumping from a 640 to a 720 score can be the difference between a high-interest private loan and a prime-rate conventional mortgage. Lowering your cost of capital through credit optimization often yields a much higher return than the cost of the restoration service itself.

What is a Debt-Service Coverage Ratio (DSCR) and why does it matter?

The Debt-Service Coverage Ratio (DSCR) measures a property's ability to cover its debt payments using its net operating income. It's calculated by dividing the annual net operating income by the total annual debt service. Lenders use this ratio to ensure the property generates enough cash flow to remain viable without relying solely on your personal income or business revenue.

How long does the commercial real estate capital procurement process usually take?

The timeline varies by product, with bridge loans closing in as little as two weeks and traditional or SBA loans taking 45 to 90 days. Proper documentation and a proactive approach to the underwriting process are the most effective ways to accelerate this timeline. Having your "Big Three" financial documents ready for review on day one can shave weeks off the closing process.