SBA Loan Consultant: Your Strategic Partner for Capital Procurement in 2026

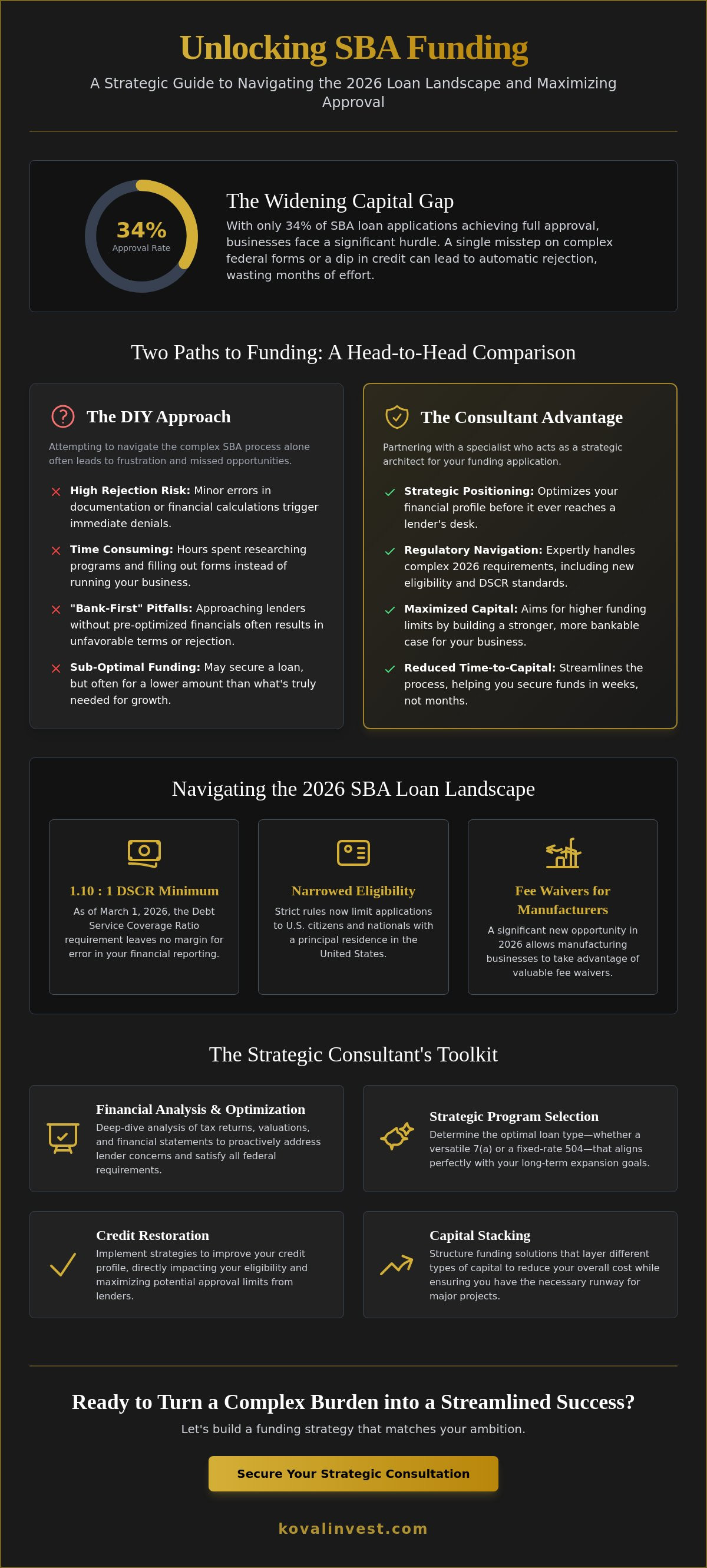

With only 34% of SBA loan applications reaching full approval in recent years, the gap between needing capital and actually receiving it has never been wider. It's frustrating to face a mountain of federal forms while worrying that a single credit score dip might trigger an automatic rejection. You've likely spent hours wondering which specific program fits your growth stage, only to find more questions than answers. Partnering with a dedicated SBA loan consultant changes this dynamic by shifting the focus from mere document preparation to strategic financial positioning.

I'll show you how a professional consultant navigates the complex 2026 federal requirements to secure the high-limit capital your business needs for expansion. You'll learn how to bypass common application hurdles, take advantage of new 2026 fee waivers for manufacturers, and ensure your funding aligns with your long-term goals. We'll explore the methodical process of turning a confusing administrative burden into a streamlined, success-based path toward sustainable growth.

Key Takeaways

- Learn why an SBA loan consultant serves as a strategic architect for your funding, ensuring your financial profile is optimized before it reaches a lender's desk.

- Navigate the specific 2026 regulatory environment, including updated eligibility standards and significant fee waivers available for manufacturing businesses.

- Discover how credit restoration and capital stacking can maximize your approval limits while reducing your overall cost of capital.

- Understand the critical pitfalls of a "bank-first" DIY approach and how to replace it with a methodical, results-oriented preparation phase.

- Master the documentation process by aligning your tax returns, valuations, and financial statements with the specific requirements of federal programs.

What is an SBA Loan Consultant and Why Does Your Business Need One?

An SBA loan consultant is a specialized financial advisor who focuses exclusively on helping businesses secure funding through the programs of the Small Business Administration (SBA). While many business owners view them as administrative help, they're actually strategic architects. They don't just fill out forms; they engineer a business's financial profile to meet the specific, often rigid, standards of federal lenders. This role is essential because the path to capital is rarely a straight line. It requires a deep understanding of how government backing interacts with private banking interests.

It's vital to distinguish between a general business coach and a results-oriented loan strategist. A coach might offer valuable advice on operational efficiency or marketing, but an SBA loan consultant specializes in the mechanics of capital procurement. They understand that a high-growth business might look "risky" on a standard bank balance sheet. The consultant's job is to bridge the gap between your operational reality and the lender's strict underwriting requirements, ensuring your story is told through the lens of bankable data.

Attempting a DIY application in 2026 carries significant risks. With the SBA now requiring a Debt Service Coverage Ratio (DSCR) of at least 1.10:1 for small loans as of March 1, 2026, the margin for error has disappeared. Regulations regarding residency and citizenship have also narrowed recently, making the eligibility landscape more difficult to navigate alone. Without an expert's eye, a single miscalculated figure or an overlooked policy change can lead to an immediate rejection, wasting months of effort.

The Core Responsibilities of a Professional Consultant

- Financial Analysis: A consultant's primary duty involves a deep dive into your financial statements to ensure they satisfy the current DSCR requirements. They don't just report numbers; they identify trends that might concern a lender and address them proactively.

- Program Selection: They determine whether the flexibility of a 7(a) loan or the long-term fixed rates of a 504 loan best serves your specific expansion plans.

The consultant acts as the primary advocate and translator between the borrower and the lender throughout the entire funding lifecycle.

The ROI of Strategic Funding Assistance

The value of professional guidance is measured in both speed and scale. By eliminating common errors and omissions, consultants significantly reduce the "time-to-capital," often helping clients secure funds in weeks rather than months. Better financial positioning frequently leads to higher funding limits, providing the necessary runway for major projects. Understanding the nuances of SBA loan assistance is essential for any business owner who views capital not just as a survival tool, but as a catalyst for long-term strategic growth. This methodical approach ensures that the funding you receive today doesn't create operational constraints tomorrow.

Navigating the 2026 SBA Loan Landscape: Programs and Requirements

The current lending environment in 2026 marks a decisive shift toward strategic expansion rather than the emergency relief focus of previous years. To secure funding, you must navigate a refined suite of SBA loan programs that prioritize for-profit entities with strong operational health. As of March 1, 2026, the SBA narrowed eligibility to U.S. citizens and nationals with a principal residence in the U.S. This change, paired with a Prime Rate of 6.75% as of June 14, 2026, creates a landscape where precision isn't just a goal; it's the only path to approval.

Lenders now place a heavy emphasis on the "certification of need." You must demonstrate that the capital is essential for growth and isn't available through other reasonable channels. A clean financial trail is mandatory. An SBA loan consultant helps you prepare for this scrutiny by ensuring your financial history is transparent and your business valuations are professionally documented to support your funding request. This preparation is the difference between a rejected application and a successful capital injection.

SBA 7(a) Loans: The Versatile Growth Engine

The 7(a) program remains the primary vehicle for working capital, equipment purchases, and debt refinancing. In 2026, the maximum loan amount is $5 million, with maturity terms extending up to 10 years for working capital and 25 years for real estate. Interest rates vary by loan size, with loans over $350,000 typically capped at Prime plus 3.00%. An SBA loan consultant is instrumental here, as they negotiate these spreads with lenders to ensure your debt service remains manageable over the long term.

SBA 504 Loans: Fixed Assets and Real Estate

For businesses looking to acquire major fixed assets or real estate, the 504 program offers long-term, fixed-rate financing. These deals are structured as a partnership between a private lender, a Certified Development Company (CDC), and the borrower. The SBA-backed portion can reach up to $5.5 million. Consultants specialize in aligning these three parties, ensuring the project meets the specific job creation or public policy goals required for 504 eligibility. This structured approach is particularly beneficial in 2026, as the SBA has waived certain fees for manufacturers to support domestic production goals.

Professional Consultant vs. DIY SBA Applications

Most business owners begin their search for capital at their local bank branch. This "bank-first" approach is a common mistake because it subjects your business to a single institution's specific internal rules, or "overlays," before your application is truly ready. If that one bank says no, you're often left with a mark on your record and no clear path forward. A "consultant-first" strategy flips this dynamic. By partnering with an SBA loan consultant, you focus on optimizing your financial profile before a single lender ever sees your file. This proactive preparation ensures that when you do apply, you're matched with a lender whose current appetite for risk aligns perfectly with your business model.

Understanding the various SBA loan programs is only half the battle; the other half is knowing how to present your business to a specific lender's internal committee. A consultant manages the entire lender-matching process, acting as a strategic matchmaker who identifies the institutions most likely to offer high-limit approvals. This creates a "win-win" alignment where the lender gets a high-quality borrower and you secure the capital needed for expansion without the stress of multiple rejections.

Common DIY Pitfalls That Lead to Rejection

- Inaccurate DSCR Calculations: Since the SBA requires a minimum Debt Service Coverage Ratio of 1.10:1 for many loans as of March 2026, even a minor math error can trigger an automatic red flag. DIY applicants often fail to account for how new debt will impact this ratio.

- Unexplained Credit Fluctuations: Simply having a "good" score isn't always enough. If there are recent dips or inaccuracies, failing to provide a clear, professional explanation can lead to a quick disqualification.

- Static Business Plans: Many owners use generic templates that don't meet 2026 underwriting standards. A plan must show specific, data-driven projections that justify the "certification of need" required by federal guidelines.

The Advantage of a Success-Based Philosophy

One of the primary objections to hiring professional help is the perceived cost. However, it's essential to view this as a partnership rather than a traditional expense. A collaborative partner is far more motivated than a distant banking institution because their success is directly tied to yours. This creates a "straight-talk" environment where we're honest about financial flaws that need fixing before the application goes live. Because the focus is on outcome-based results, there's a significant reduction in financial risk. You aren't just paying for a service; you're investing in a methodical path toward a guaranteed funding goal, ensuring that every move you make is calculated for maximum impact.

The Koval Advantage: Credit Optimization and Capital Stacking

Securing a federal loan involves more than just demonstrating cash flow; it requires a pristine financial reputation. While most advisors treat your current credit score as a fixed constraint, a strategic SBA loan consultant views it as a variable that can be engineered for better results. We recognize that your credit profile is the primary lever for determining not just your eligibility, but the interest rate spread you'll pay over the Prime Rate of 6.75%. By positioning Koval Investments as the partner that handles both the credit "fix" and the eventual funding, we eliminate the friction between preparation and approval.

Credit restoration is the "secret weapon" that many successful applicants use to move from a tentative "maybe" to a high-limit approval. We don't just look at the three-digit number; we analyze the underlying data that lenders scrutinize during the underwriting process. This methodical approach allows us to fix foundational flaws before they become reasons for rejection. When your credit is optimized, you gain access to the most favorable terms available under the current 2026 guidelines, ensuring your debt remains a tool for growth rather than a burden on your cash flow.

Repairing Credit for SBA Eligibility

Our process begins with identifying and disputing inaccuracies on both business and personal credit reports. These errors are more common than many entrepreneurs realize and can unfairly suppress your borrowing power. You should follow strategic steps to improve your business credit profile well before your lender review begins. A 50-point score increase can save thousands in interest over the life of an SBA loan. This focus on precision ensures that your application reflects your true creditworthiness, allowing you to bypass the stricter overlays often imposed by traditional banks.

Integrating 0% Interest Funding

The concept of "Capital Stacking" is where our strategic approach truly shines. Many businesses struggle with the down payment requirements or the initial closing costs associated with federal programs. We solve this by showing you how to use 0% interest business funding to bridge the gap. This unsecured capital provides the liquidity needed to satisfy SBA requirements without diluting your equity or taking on high-interest short-term debt. By integrating these solutions, we optimize your total cost of capital and maximize your operational efficiency from day one.

If you're ready to move beyond basic applications and build a comprehensive capital strategy, we invite you to connect with a strategic partner for capital who understands the full scope of your business ambitions.

How to Get Started with an SBA Loan Consultant

The transition from planning to procurement begins with a rigorous financial health check. Engaging an SBA loan consultant allows you to move through this phase with a clear understanding of your fundability before any formal application is submitted. This initial audit focuses on more than just your credit score; it examines the structural integrity of your business, your debt-service capabilities, and your readiness for 2026's stricter underwriting standards. By identifying potential hurdles early, we ensure that the path to capital is a methodical progression rather than a series of trial-and-error attempts.

Our collaborative process is designed to be low-pressure and outcome-focused. We act as a steady hand, guiding you through the practicalities of engagement while maintaining a sharp focus on your long-term expansion goals. This "straight-talk" approach ensures you're never left wondering where your application stands or what the next logical step should be. We value the quality of our relationships and align our success-based philosophy with your tangible business growth.

Preparing Your Documentation for 2026 Standards

Success in the current lending environment requires a comprehensive and professionally organized document package. You'll need to gather the last three years of federal tax returns for both your business and any individual owners with a stake of 20% or more. Current year-to-date profit and loss statements, along with a balance sheet, are essential for demonstrating your business's ongoing health. If your growth strategy involves using working capital for business acquisition, your documentation must also include the financial records and a professional valuation of the target competitor to justify the investment.

The Path to Funding: A Strategic Timeline

The timeline for securing capital is structured in clear, manageable phases. During weeks 1-4, we conduct a deep-dive audit of your financials and optimize your credit profile to reach a "Ready-to-Fund" status. Once your package is optimized, we move into the lender-matching and submission phase. While standard processing can take 6-12 weeks, working with Preferred Lenders can often reduce this window to 2-4 weeks. Throughout the underwriting process, your SBA loan consultant remains your primary advocate, answering lender inquiries and ensuring the deal stays on track through closing. This methodical approach allows you to focus on implementing your growth strategy while we handle the complexities of the capital stack.

Ready to secure the capital your business needs to scale in 2026? Let's begin with a strategic consultation to align your financial profile with your expansion ambitions.

Accelerate Your Business Growth with Strategic Capital

Navigating the complexity of federal funding doesn't have to be a solitary or risky endeavor. By shifting from a bank-first approach to a consultant-first strategy, you ensure your business is positioned for the best possible terms before your application ever reaches a lender. Working with an SBA loan consultant transforms a cumbersome administrative process into a methodical, success-based path toward expansion. You've seen how professional credit optimization and the strategic integration of 0% interest funding can significantly reduce your borrowing costs while maximizing your available liquidity.

At Koval Investments, we operate on a success-based philosophy that removes the financial risk from your shoulders. Our deep expertise in both credit restoration and capital procurement allows us to handle the preparation and the funding simultaneously. We provide a comprehensive approach that includes 0% interest funding integration to cover initial costs and down payments. Secure your success-based SBA consultation with Koval Investments today to discover how our strategic solutions can provide the fuel your business needs to scale. We're ready to partner with you to turn your strategic ambitions into tangible results.

Frequently Asked Questions

How much does an SBA loan consultant cost?

Fees for professional consulting are typically negotiated between the business owner and the advisor, often structured as a percentage of the total loan amount. This creates a success-based environment where your partner is motivated to secure the highest possible funding limit. Because the engagement is collaborative, the value provided through interest rate negotiations and fee waivers often offsets the cost of the service.

Can an SBA loan consultant help if I have bad credit?

Yes, a consultant assists by integrating credit repair services into the preparation phase to optimize your score before the lender review. Since 2026 guidelines allow lenders to take a more holistic view of business health, fixing inaccuracies and explaining past fluctuations can prevent automatic disqualification. This proactive approach ensures your financial profile meets the necessary standards for approval despite past credit challenges.

What is the difference between an SBA consultant and a bank loan officer?

A bank loan officer is an employee of the financial institution whose primary responsibility is to protect the bank's interests and follow its specific internal "overlays." An SBA loan consultant acts as your personal advocate and strategic architect. They work for you, not the bank, and use their industry knowledge to match your business with the specific lender most likely to approve your high-limit request.

How long does the SBA loan process take with professional help?

Professional guidance can significantly accelerate the timeline, often reaching a "Ready-to-Fund" status within four weeks. When working with Preferred Lenders, the processing time can be as short as 2 to 4 weeks. Without professional help, the process frequently stretches to 12 weeks or longer due to documentation errors, incomplete business plans, or back-and-forth inquiries from the lender's underwriting committee.

What is the most common reason SBA loans are denied in 2026?

The most frequent cause for denial is failing to meet the mandatory Debt Service Coverage Ratio (DSCR) of 1.10:1, which became a strict requirement on March 1, 2026. Many businesses also face rejection because their "certification of need" isn't properly documented or their business plans lack the data-driven projections required by modern underwriting standards. A consultant identifies these mathematical and narrative flaws before the application is submitted.

Can a consultant help me get a 0% interest business loan alongside an SBA loan?

Yes, this is a core part of a capital stacking strategy. We integrate 0% interest funding solutions to provide the liquidity needed for down payments or initial operational costs. This synergy allows you to satisfy SBA requirements without depleting your cash reserves, ultimately lowering your total cost of capital and improving your business's overall debt-to-income profile during the application process.

Do I need a business valuation before talking to a consultant?

You don't need a valuation completed before your initial consultation. Part of our strategic planning involves determining if a professional valuation is necessary for your specific loan program, such as an SBA 504 real estate deal or a 7(a) loan for a business acquisition. If one is required, we help coordinate the process to ensure the valuation meets the strict standards of federal lenders.

Is an SBA loan consultant worth it for a small microloan?

While SBA microloans are capped at $50,000, professional guidance ensures you don't make errors that could disqualify you from larger funding in the future. However, the return on investment is most significant for 7(a) and 504 programs where the capital needs are higher and the regulations are more complex. For businesses targeting millions in growth capital, the expertise of a consultant is essential for navigating the intricate 2026 requirements.