Small Business Financing Without Collateral: The 2026 Guide to Unsecured Capital

What if the strongest security you could offer a lender wasn't a physical asset like your home, but a strategically optimized financial profile? Many entrepreneurs mistakenly believe that securing significant capital requires putting their personal livelihood on the line. This fear often leads to stagnation, especially when traditional banks demand a level of collateral that feels more like a ransom than a partnership. Finding reliable small business financing without collateral is no longer a matter of luck; it's a result of understanding the specific levers that modern lenders value most in 2026.

We understand the pressure of needing growth capital while facing the reality of higher interest rates and stricter credit thresholds, like the current SBSS minimum of 165. You deserve a path to funding that doesn't involve risking your family's future. This guide will show you exactly how to navigate the current lending environment to secure affordable working capital and maintain total personal asset protection. We'll explore the latest SBA updates, the power of credit repair as a funding catalyst, and how to structure your business to qualify for 0% interest funding solutions that keep your overhead low and your momentum high.

Key Takeaways

- Learn why 2026 lenders are shifting away from traditional asset-backed requirements toward profile-based evaluations that prioritize your business's operational health.

- Discover how to leverage 0% interest funding structures and unsecured lines of credit to maintain cash flow without the burden of high APRs.

- Understand the critical role of credit repair as a strategic tool for securing small business financing without collateral and increasing your total capital limits.

- Master the two-step qualification process involving comprehensive credit audits and revenue projections to position your firm as a low-risk borrower.

- Explore how a success-based partnership with a strategic advisor can align your growth goals with the most competitive unsecured capital structures available.

What is Small Business Financing Without Collateral?

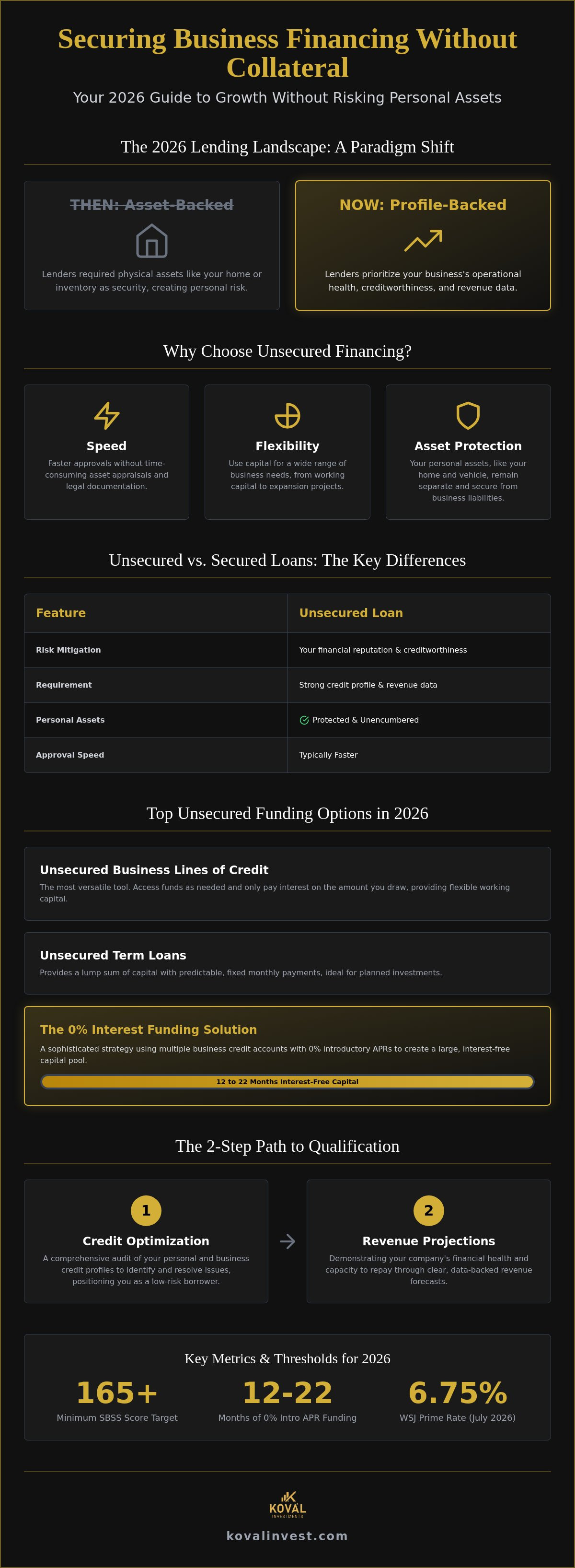

Small business financing without collateral is a funding structure where capital is provided based on a borrower's creditworthiness and business performance rather than physical assets. Unlike traditional mortgages or equipment loans, these arrangements don't require you to pledge your home, vehicle, or inventory as security. In the financial sector, this is commonly known as an unsecured loan. By 2026, the lending environment has moved away from "asset-backed" requirements toward a "profile-backed" model. Lenders now use sophisticated data to evaluate the health of your business rather than just the value of your property.

Entrepreneurs lean toward these options for three primary reasons: speed, flexibility, and protection. Secured loans often require time-consuming appraisals and legal documentation that can stall your operations. Unsecured capital moves faster. It also ensures that your personal assets remain separate from your business liabilities. While some analysts suggest that secured debt is cheaper, they often overlook the "risk cost" involved. If a business faces a temporary downturn, a secured loan puts your personal property on the line. Small business financing without collateral eliminates that specific fear, allowing you to focus on growth without risking your family's security.

Unsecured vs. Secured Business Loans

The main difference lies in how a lender mitigates risk. In a secured loan, the asset is the safety net. In collateral-free funding, the safety net is your financial reputation. Most unsecured agreements involve a personal guarantee. This is a commitment to repay the debt based on your credit profile rather than a specific piece of machinery. This structure is often better for your balance sheet. It keeps your assets unencumbered, which preserves your ability to borrow for other needs later. Lenders in 2026 look for a synergy between your personal credit score and your company's revenue to determine your capacity.

Common Misconceptions About No-Collateral Funding

Many owners wrongly believe that unsecured capital is a last resort for failing businesses. In reality, it's a strategic tool used by high-revenue firms to maintain agility. Another myth is that "no collateral" automatically means "high interest." While some lenders charge a premium for the lack of security, optimized businesses can access 0% interest funding solutions. These introductory periods allow you to use capital for 12 to 22 months without accruing interest charges. It's not about being in a desperate situation; it's about having a profile strong enough that your word and your data are worth more than a physical asset.

Top Unsecured Funding Options for Small Businesses in 2026

Many online lenders push high-interest Merchant Cash Advances as the primary solution for small business financing without collateral. While these products provide speed, they often carry effective APRs that can drain your monthly cash flow. A more sustainable approach to small business financing without collateral involves leveraging credit-based structures and government-backed guarantees. In July 2026, with the Wall Street Journal Prime Rate sitting at 6.75%, choosing the right vehicle for capital is critical for maintaining healthy profit margins.

Unsecured business lines of credit remain the most versatile tool for flexible working capital. These allow you to access funds as needed and only pay interest on the amount you actually draw. For those seeking fixed structures, unsecured term loans provide predictable monthly payments without the need to pledge real estate or equipment. However, the most competitive options in the current market often involve strategic credit stacking or specialized SBA products that prioritize your financial profile over physical security.

The 0% Interest Funding Solution

Credit stacking is a sophisticated method where multiple business credit accounts with 0% introductory APRs are utilized to create a large pool of capital. This strategy provides interest-free funding for 12 to 22 months. It's particularly effective for inventory purchases or marketing campaigns where the return on investment is realized within a year. You can learn more about this in The Ultimate Guide to 0% Interest Business Funding in 2026. This approach allows you to scale your operations without the immediate burden of heavy debt service.

SBA Assistance for No-Collateral Loans

The Small Business Administration has implemented significant updates for fiscal year 2026. While the SBA generally seeks collateral for larger loans, they typically don't require it for loans under $50,000. For larger amounts, the SBA's guarantee acts as a substitute for physical assets, which encourages traditional banks to lend to qualified owners. According to the SBA's own resources on unsecured business funding, the evaluation focuses on the borrower's ability to repay rather than what they can pledge.

With the SBA 7(a) cumulative loan limit now at $10 million as of July 4, 2026, the opportunities for significant capital are vast. For manufacturers, the SBA has even waived most upfront fees on 7(a) loans up to $950,000 this year. Navigating these thresholds requires a clean financial profile and a methodical approach to the application. If you're looking for a partner to help you navigate these options, SBA Loan Assistance: A Strategic Guide offers a deeper look into the process. We focus on helping you find the working capital that aligns with your specific growth objectives.

Why Credit Optimization is the Real Key to Unsecured Capital

Your credit report is the only collateral that truly matters when pursuing small business financing without collateral. While traditional loans rely on the liquidation value of a building or a piece of equipment, unsecured lenders rely on the integrity of your financial track record. They view your credit profile as a predictive map of future behavior. A single reporting error or an optimized utilization ratio can be the difference between a rejection and a $100,000 line of credit. This is why we treat credit not as a static score, but as a variable asset that must be engineered for maximum leverage.

There's a direct, measurable relationship between the precision of your credit profile and your total funding limits. Lenders use your personal credit as a litmus test for business reliability, especially in the early stages of growth. By optimizing your personal report while simultaneously building a robust business profile with agencies like Dun & Bradstreet and Experian Business, you create a "double-blind" layer of security for the lender. This dual-profile strength allows you to access significantly higher capital amounts than a business owner relying on revenue alone. Proactive optimization prevents the need for high-interest emergency borrowing, which often occurs when a business with a "thin" credit file is forced into predatory lending cycles during a cash crunch.

Professional Credit Repair vs. DIY

Many entrepreneurs attempt a DIY approach to credit, but business-level funding requires a more surgical touch. Professional Mastering Business Credit Repair Services focuses on more than just removing late payments. It involves identifying deep-seated inaccuracies that suppress your score and strategically managing debt-to-income ratios to satisfy 2026's stricter underwriting standards. For instance, with the SBSS score threshold now at 165 for many SBA-related products, every point on your report carries a tangible dollar value in terms of potential capital access.

The ROI of a Higher Credit Score

The return on investment for a higher credit score is most visible in your interest savings. When you compare the top unsecured funding options, a score of 720 or higher often unlocks 0% interest introductory offers that can save a business tens of thousands of dollars in debt service over a 12 to 22-month period. Credit optimization is the strategic engineering of financial profiles to maximize borrowing capacity while minimizing interest costs. Even a 1% reduction in the interest rate on a five-year term loan can drastically improve your bottom line, providing more liquidity to reinvest in marketing, inventory, or strategic acquisitions.

How to Qualify for Financing Without Pledging Assets

Qualifying for small business financing without collateral is a methodical process that prioritizes your financial narrative over your physical inventory. Lenders in 2026 are highly selective, focusing on your ability to manage debt rather than your ability to liquidate a property. To position your business for success, follow these five essential steps:

- Audit Credit Health: Review both personal and business credit reports for suppression factors. As mentioned in previous sections, even minor inaccuracies can drastically lower your SBSS score, which many lenders now require to be at least 165.

- Forecast Revenue: Develop detailed cash flow statements and revenue projections. Lenders want to see that your business generates enough surplus to cover monthly payments comfortably.

- Define Purpose: Clarify if you need working capital for daily operations or funds for long-term expansion. Specificity here builds lender confidence and helps them match you with the right product.

- Optimize Profile: Engage in professional consulting to resolve inaccuracies or high utilization. This is where strategic planning and credit repair intersect to maximize your eligibility.

- Select Specialists: Approach lenders whose underwriting models are built for profile-based capital rather than asset-backed debt.

Financial Documentation Required

Lenders often prioritize recent bank statements over tax returns for unsecured lines of credit. Bank statements provide a real-time view of your liquidity and cash velocity. In contrast, tax returns represent lagging data that may not reflect your current growth trajectory. Maintaining a clean Debt-to-Income (DTI) ratio is also vital. A high DTI suggests that your revenue is already over-leveraged, which can trigger higher interest rates or lower funding caps. When presenting your case to an SBA loan consultant, focus on your "debt service coverage ratio" to prove you can handle the new obligation without operational strain.

Bridging the Gap for Newer Businesses

Many entrepreneurs believe that having less than two years of business history is an automatic disqualifier for small business financing without collateral. While traditional institutions often have rigid history requirements, you can bridge this gap by leveraging founder credit. Your personal credit score acts as a temporary surrogate for the business's track record, allowing you to access unsecured business lines while your company matures. This approach is particularly effective when you have a 720+ score and a clear path to revenue. For those who don't fit the standard bank mold, exploring alternative business funding solutions provides a path to capital that rewards strategic planning over tenure. If you're ready to optimize your profile for maximum funding, contact us today for a strategic evaluation of your capital options.

Secure Your Future with Koval Investments' Strategic Funding

Accessing small business financing without collateral shouldn't be a transaction that leaves you feeling exposed or over-leveraged. At Koval Investments, we operate on a success-based philosophy. This means our objectives are directly aligned with your ability to scale. We don't act as a distant institution; we act as a seasoned strategic partner and mentor. By integrating our credit repair services with capital procurement, we ensure that you don't just get a loan, but the most efficient capital structure possible for your specific situation. It's a collaborative venture where we only win when you do.

High-volume, automated lenders often treat business owners like data points on a spreadsheet. They prioritize speed over strategy, which frequently leads to high-interest debt that stalls long-term progress. Our boutique approach is different. We take the time to understand your operational constraints and ambitions. This personalized connection allows us to bridge the gap between high-level financial strategy and your day-to-day reality. Beyond the initial funding, we offer specialized business valuations and mergers and acquisitions consulting to help you prepare for long-term exits or strategic growth phases.

The Koval 0% Interest Advantage

Our 0% Interest Funding Solution is designed to provide zero-cost debt for businesses that qualify through our optimization process. By strategically stacking introductory offers, we've helped clients scale operations and increase inventory without the immediate pressure of interest payments. This method allows you to secure significant small business financing without collateral while keeping your personal assets entirely protected. Every engagement includes customized strategic planning to ensure that the capital you secure is deployed for maximum return. We focus on creating a win-win environment where your business can thrive without the typical high-interest burdens of unsecured debt.

Take the Next Step Toward Collateral-Free Growth

The lending landscape in 2026 is moving fast. With SBA cumulative limits reaching $10 million and new credit thresholds in place, now is the time to optimize your financial profile. We offer a low-pressure, collaborative environment where we share our "insider" knowledge to help you navigate these complexities. We pride ourselves on a "straight-talk" mentality, providing the pragmatism and integrity you need from a trusted advisor. Whether you're seeking working capital for immediate needs or preparing for a future expansion, we are here to guide you through every step of the process.

Schedule your strategic funding consultation with Koval Investments today and discover how a success-based partnership can transform your access to capital.

Mastering Your Capital Strategy for 2026

Securing small business financing without collateral is no longer a matter of chance; it's a result of deliberate financial engineering. By shifting your focus from physical assets to your credit profile, you unlock access to more flexible and affordable capital. We've explored how credit optimization acts as your modern collateral and why 0% interest stacking remains the most competitive way to scale without high-interest burdens. These strategies allow you to maintain momentum while keeping your personal assets entirely protected from business liabilities.

Since 2018, Koval Investments has functioned as a boutique strategic partner for entrepreneurs who value precision over volume. Our team specializes in 0% interest funding and SBA assistance, offering a comprehensive suite that includes credit repair and business valuations. We operate on a success-based philosophy because we believe our growth should be a direct reflection of yours. You don't have to navigate the complexities of 2026 lending alone when you have a partner invested in your long-term viability.

The path to interest-free capital and personal asset protection is within your reach. Secure your 0% interest funding strategy with Koval Investments and take the first step toward a more resilient financial future. Your business deserves a foundation built on strategy, not risk. We look forward to helping you scale with confidence.

Frequently Asked Questions

Can I get a small business loan with no collateral and bad credit?

Yes, but obtaining small business financing without collateral with a low credit score requires a methodical repair process first. Lenders in 2026 typically look for an SBSS score of at least 165 to qualify for the most competitive terms. If your score is below this threshold, focusing on professional credit repair is the most effective way to unlock capital. Without optimization, you may be limited to high-interest short-term options that can strain your company's cash flow.

What is the maximum amount I can borrow without collateral in 2026?

The maximum amount depends on your revenue and credit profile rather than a fixed universal cap. While the SBA 7(a) cumulative limit has increased to $10 million as of July 4, 2026, unsecured portions are often capped at lower levels, such as $50,000 for specific SBA products. Private lenders may offer higher amounts if your debt-service coverage ratio is strong. Strategic credit stacking can also generate several hundred thousand dollars in interest-free capital for qualified owners.

Does an unsecured business loan require a personal guarantee?

Most unsecured business loans require a personal guarantee from the business owners. Since there is no physical property to seize in the event of a default, the lender relies on your personal commitment to repay the debt. This guarantee essentially links your personal creditworthiness to the business obligation. It serves as the primary security for the lender, effectively replacing the need for equipment or real estate liens while keeping your assets unencumbered.

How do 0% interest business funding solutions work?

These solutions work by identifying and applying for business credit accounts that offer 0% introductory APR periods. By stacking multiple accounts, you can access a significant pool of working capital for 12 to 22 months without accruing interest. This approach requires a high personal credit score, typically 720 or above, to qualify for the most competitive offers. It's a strategic way to fund growth or inventory without the burden of immediate debt service costs.

Will an unsecured loan affect my personal credit score?

An unsecured loan may affect your personal credit score depending on the lender's reporting practices and the presence of a personal guarantee. Most lenders perform a hard inquiry during the application process, which can cause a minor, temporary dip in your score. If the loan is reported to personal credit bureaus, your utilization ratio might be impacted. However, many business-specific lines of credit only report to business bureaus unless a payment is missed or a default occurs.

How long does it take to get approved for no-collateral financing?

Approval for no-collateral financing is significantly faster than for secured loans, often ranging from 24 hours to two weeks. Because there are no physical appraisals or title searches required, the underwriting process focuses entirely on digital data and credit profiles. Online lenders provide the quickest turnaround for small business financing without collateral, while traditional banks and SBA-backed options take longer due to more rigorous documentation and manual review requirements.

Are SBA loans always secured by collateral?

SBA loans are not always secured by collateral, particularly for smaller loan amounts. For SBA 7(a) loans under $50,000, lenders are generally not required to take collateral. For loans exceeding this amount, the SBA requires lenders to follow their established collateral policies, but they won't decline a loan solely because a business lacks sufficient assets to pledge. This makes the SBA a viable path for service-based companies with strong cash flow but few physical assets.

Can I use unsecured funding for business acquisitions?

You can use unsecured funding for business acquisitions, provided the capital structure supports the purchase price and operational needs. Using a 0% interest funding solution or an unsecured line of credit can provide the necessary liquidity for a down payment or to cover closing costs. This is often a strategic component of M&A consulting, allowing buyers to preserve their own cash while leveraging their credit profile to expand their business portfolio through acquisition.