Strategic Funding for Real Estate Investors: The 2026 Capital Guide

In 2026, the traditional bank mortgage has officially become the slowest and most expensive path to growing a property portfolio. Finding sustainable funding for real estate investors now requires moving beyond the rigid debt-to-income requirements that have tightened significantly this year. You've likely felt the pressure as interest rates for investment properties stay north of 7.12%, while new FinCEN reporting rules for entity-based transfers add layers of complexity to every closing. It's frustrating to watch a profitable deal disappear because a legacy lender is stuck in a month-long approval cycle.

We believe that your success depends on agility and the strategic management of your capital costs. You'll discover how to navigate this new lending environment by building a capital stack that bypasses traditional red tape and secures the capital necessary to scale. We will show you how to access fast, flexible funding and use business credit to lower your overall cost of debt. This approach allows you to scale your acquisitions with the confidence of a partner who values your progress as much as you do. We'll explore how to leverage 0% interest solutions and DSCR loans to keep your momentum steady in any market condition.

Key Takeaways

- Identify the institutional shifts making traditional mortgages less effective for rapid growth in the 2026 lending environment.

- Master the layers of the real estate capital stack to better manage your debt and equity ratios for maximum deal profitability.

- Learn to leverage strategic alternatives such as hard money and private lending to secure reliable funding for real estate investors.

- Uncover the direct impact your personal credit profile has on your ability to secure low-cost capital and maintain investment leverage.

- Discover how integrating credit repair with specialized capital solutions creates a sustainable and predictable path for scaling your portfolio.

Navigating the Real Estate Funding Landscape in 2026

The financial environment for property acquisitions has shifted dramatically this year. With the passing of the "21st Century ROAD to Housing Act" in June 2026, the industry is witnessing a pivot toward stricter oversight of institutional buyers alongside efforts to modernize FHA loans. This legislative shift, combined with the FinCEN reporting rules introduced in March, means that "all-cash" deals via legal entities now face unprecedented transparency requirements. For those seeking funding for real estate investors, the path is no longer a straight line through a local bank branch. It requires a more sophisticated, multi-layered approach to capital.

When examining a broad real estate investing overview, it becomes evident that while the fundamentals of property value remain, the mechanisms of acquisition have changed. The gap between market opportunity and investor liquidity is widening. While inventory is beginning to stabilize, the cost of traditional debt remains high, with 30-year fixed mortgage rates for investment properties hovering between 7.12% and 7.62%. This creates a squeeze on cash flow that traditional lending models aren't designed to solve.

The 2026 Lending Climate for Investors

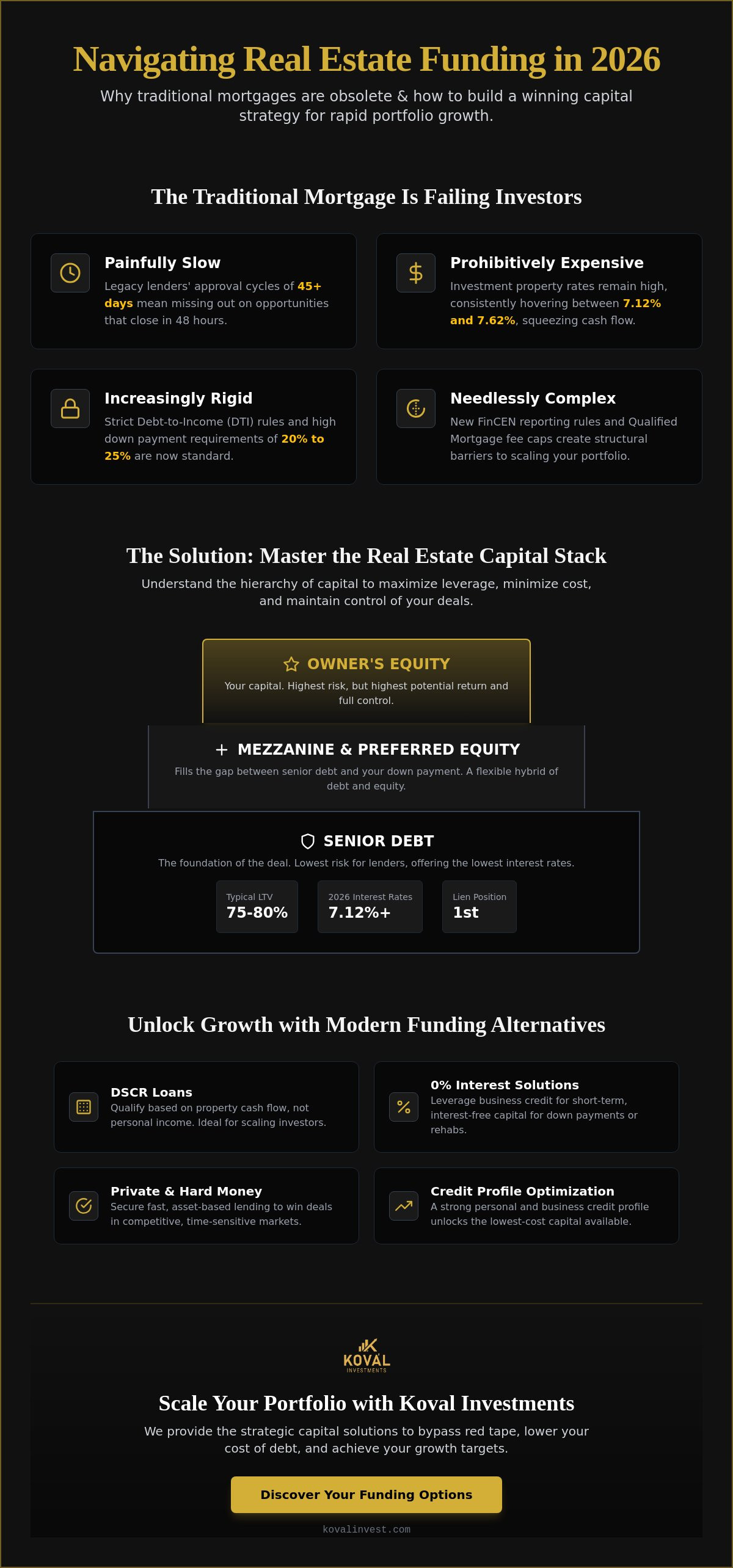

Current debt-to-income (DTI) constraints have become a significant hurdle for even seasoned professionals. Lenders have tightened the screws on how they calculate qualifying income, often ignoring a portion of projected rental yields in favor of historical tax returns. Simultaneously, rising property values have pushed loan-to-value (LTV) requirements into stricter territory. Most traditional institutions now demand 20% to 25% down payments for non-owner-occupied units. Speed is the new currency. In a market where deals are often won or lost in 48 hours, waiting 45 days for a conventional approval is a recipe for stagnation.

Why Traditional Banks Are Not Enough

The "red tape" problem is more than just a nuisance; it's a structural barrier to scaling. Institutional approval processes are bogged down by 2026 Qualified Mortgage points and fees limits, which cap fees at 3% for loans over $137,958. This regulatory environment makes small-dollar or complex deals less attractive to big banks. Most investors also hit a "ceiling" after their tenth conventional loan, regardless of their portfolio's performance. Your personal credit profile continues to dictate your leverage in these scenarios, often linking your business growth to your private financial history. We see this as an unnecessary tether. Relying solely on traditional funding for real estate investors limits your ability to act when a high-value opportunity arises unexpectedly.

Understanding the Real Estate Capital Stack: Debt vs. Equity

The capital stack is the legal and financial hierarchy of every dollar used to purchase and develop a property. It defines who has the first claim on cash flow and who carries the highest risk. For those seeking funding for real estate investors, understanding this structure is the difference between a deal that scales and one that creates a bottleneck. Every transaction is built on layers, starting with the most secure senior debt at the bottom and moving up through mezzanine financing to the equity held by the owner at the top.

Choosing the right mix of these layers allows you to maximize your cash-on-cash return. When you utilize debt effectively, you're able to control a high-value asset with a relatively small amount of your own capital. This creates leverage. If you're exploring various real estate financing options, you'll see that the goal is to find the most cost-effective capital for the lower layers while retaining as much of the top-layer equity as possible. This balance ensures you maintain control while keeping your personal liquidity available for the next opportunity.

The Role of Senior Debt

Senior debt holds the first-position lien on the asset. It's the most secure layer for a lender, which is why it typically offers the lowest interest rates. In 2026, the market for institutional senior debt on investment properties sees interest rates between 7.12% and 7.62% for 30-year fixed mortgages. While this capital is relatively inexpensive, it comes with strict requirements. Traditional banks usually limit their exposure to 75% or 80% of the property's value. This leaves a "gap" that you must fill with your own cash or secondary financing layers.

Mezzanine and Bridge Funding

Bridge and mezzanine funding act as the connective tissue in your capital stack. These options are designed to close the gap between your senior loan and your required down payment. Bridge loans are especially useful for "fix and flip" or value-add projects where traditional banks won't lend due to the property's condition. In the current climate, hard money and bridge rates range from 9.5% to 14%. While these costs are higher, the speed and flexibility they provide are often worth the expense to secure a time-sensitive deal. If you're navigating these complex layers, our team offers specialized real estate investment funding to help you structure a winning deal.

Balancing risk across these layers is essential. High leverage can amplify your returns, but it also increases your sensitivity to market shifts. A healthy capital stack ensures that your debt service remains manageable even if rental income fluctuates. This strategic approach to funding for real estate investors is what separates a hobbyist from a professional looking to build a multi-generational portfolio.

Strategic Alternatives to Traditional Bank Mortgages

When traditional institutions fail to provide the necessary agility, alternative funding for real estate investors becomes the primary engine for growth. You don't have to rely on a single source of capital. Diversifying your approach allows you to secure deals that others miss due to a lack of liquidity. By looking beyond the local bank, you can find flexible terms that align with the specific needs of your project, whether it's a quick renovation or a long-term hold.

Exploring various real estate financing options reveals a landscape where speed and creativity often outweigh the benefits of a slightly lower interest rate. Seller financing, for instance, allows you to negotiate terms directly with the property owner. This can result in lower down payments or interest-only periods that preserve your cash flow during the critical early stages of an acquisition. It's a collaborative way to structure a win-win deal that bypasses the friction of institutional underwriting.

The Power of 0% Interest Funding

One of the most effective ways to scale is by using 0% APR business credit as a gap funding tool. This strategy allows you to cover the 20% to 25% down payment required by senior lenders without depleting your personal cash reserves. By utilizing unsecured capital, you avoid the high-interest bridge loans that often eat into your initial equity. It's a clean, efficient way to maintain momentum. For a deeper look at how this works, read The Ultimate Guide to 0% Interest Business Funding in 2026. This method provides the liquidity you need to act fast while keeping your overall cost of debt manageable.

Private and Hard Money Strategies

Hard money and private lending offer the speed that traditional banks simply cannot match. When comparing commercial real estate financing options, it's clear that hard money is a tool for specific scenarios. With current rates between 9.5% and 14%, it's more expensive than conventional debt, but it allows for closings in as little as 10 to 18 days. The higher cost is often justified by the ability to secure a distressed asset at a significant discount.

Private money lending relies on building strong relationships with individual backers. To succeed here, your pitch must be transparent and results-oriented. You aren't just asking for capital; you're offering an opportunity for a partner to earn a secure return. Successfully managing these high-interest risks requires a clear exit strategy, such as refinancing into a long-term DSCR loan once the property is stabilized. This proactive approach to funding for real estate investors ensures that you're always moving toward more permanent, lower-cost financing as your portfolio grows.

Optimizing Your Financial Profile for Maximum Funding

Your personal financial reputation is the invisible filter through which every lender views your deal. While we've discussed alternative funding for real estate investors like hard money, your personal credit score remains the primary lever for reducing the cost of that debt. A higher score doesn't just mean an approval; it means lower interest rates and higher funding limits. It transforms you from a high-risk borrower into a preferred partner who can command better terms in any negotiation.

Many investors assume their reports are accurate. However, industry data suggests that a significant percentage of credit reports contain errors that can suppress scores by 50 points or more. These inaccuracies often include incorrect account statuses, duplicate reporting of the same debt, or outdated public records that should have been removed years ago. For an investor, these errors aren't just annoying; they're expensive. A lower score can trigger higher points at closing or disqualify you from the 0% interest introductory offers that keep your acquisitions profitable.

Credit Restoration as a Growth Strategy

Proactive credit repair is a strategic investment in your future borrowing power. Reaching a 700+ score opens doors to institutional capital and specialized funding for real estate investors that remains closed to those in the mid-600s. It involves a methodical approach to disputing inaccuracies and optimizing your credit utilization ratios. This preparation is especially critical if you're considering federal options or long-term portfolio loans. You can find more details on these specific requirements in our SBA Loan Assistance: A Strategic Guide.

Establishing Real Estate Entities

Scaling requires moving beyond personal liability. Funding deals through an LLC or Corporation provides a layer of privacy and protects your personal assets from property-specific risks. It also allows you to build a separate business credit profile. When your entity has its own credit history, you can eventually secure working capital and acquisition loans that don't appear on your personal credit report. This separation is vital for maintaining a low debt-to-income ratio and keeping your personal borrowing capacity clear for future needs. Aligning your strategic planning with your entity structure ensures that your business grows as a stand-alone, fundable asset.

If your current credit profile is holding back your acquisitions, our Credit Repair Services can help you rebuild the foundation necessary to access premium capital and accelerate your portfolio growth.

Scaling Your Portfolio with Koval Investments’ Capital Solutions

Scaling a real estate portfolio in 2026 demands a departure from traditional, slow-moving finance. We provide the specialized funding for real estate investors that allows for rapid execution without the friction of institutional red tape. Our approach isn't just about providing a loan; it's about building a sustainable capital structure that supports long-term growth. We integrate our various services to ensure that every layer of your financial profile is optimized for maximum leverage. This methodical preparation ensures you're ready to act when the right deal appears.

The synergy between our Credit Repair Services and capital procurement is a cornerstone of our strategy. By addressing inaccuracies and optimizing your credit score, we lower your cost of debt and increase your eligibility for premium products. This preparation is the foundation for our success-based philosophy. We operate as your strategic partner, aligning our goals with your portfolio's expansion. This means our success is directly tied to the results we deliver for you. We value the quality of our relationships and the alignment of our goals over high-volume, impersonal transactions.

Comprehensive Capital Procurement

Our 0% Interest Funding Solution is designed specifically for the agility required in the 2026 market. It provides the unsecured capital necessary for down payments, allowing you to preserve your personal liquidity for operational needs. When your strategy involves owner-occupied properties, we provide the expertise needed to navigate complex SBA Loans. These federal programs offer excellent terms but require a meticulous application process that we manage alongside you. For investors looking beyond single properties, our Mergers and Acquisitions Consulting ensures that your transition into larger portfolio acquisitions is seamless and strategically sound. We provide the steady hand needed in these complex financial environments.

Partnering for Long-Term Success

A strategic partner is essential when navigating the tighter debt-to-income rules and high interest rates of the current year. We help you move from single-unit deals to multi-family and commercial assets by providing the necessary funding for real estate investors who are ready to scale. This transition requires a shift in mindset and a more robust Strategic Planning framework. Our consultants work with you to develop a plan that accounts for capital availability and market shifts. We don't just provide a service. We offer a collaborative venture that bridges the gap between high-level financial strategy and your daily operations. Contact our consultants today to develop a customized funding roadmap that accelerates your path to significant portfolio growth.

Future-Proofing Your Real Estate Strategy

Success in the 2026 market isn't about finding just any capital; it's about finding the right capital at the right time. You've seen how mastering the capital stack and maintaining a 700+ credit score can transform your acquisition speed. By leveraging strategic alternatives like 0% interest business credit, you can maintain the liquidity necessary to seize undervalued properties while others are sidelined by institutional delays. The landscape has changed, but the opportunities remain abundant for those who move beyond traditional bank red tape.

Since 2018, we've acted as a steady hand for entrepreneurs navigating these complex financial shifts. We specialize in success-based 0% interest funding and comprehensive credit restoration to ensure your entity is fully fundable and ready for growth. This is the most reliable way to secure consistent funding for real estate investors who are serious about scaling their portfolios. Our strategic advisory services are designed to align with your specific objectives, providing the clarity you need to move from single units to commercial assets.

Ready to take the next step in your investment journey? Secure your real estate investment capital with Koval Investments and receive a customized roadmap tailored to your 2026 goals. The market rewards those who are prepared and agile. We look forward to helping you build a more resilient and profitable portfolio.

Frequently Asked Questions

What is the best type of funding for real estate investors in 2026?

The best funding for real estate investors in 2026 is often a combination of DSCR loans for long-term holds and 0% business credit for initial liquidity. DSCR loans qualify you based on the property’s rental income rather than personal tax returns, which is vital given current DTI constraints. Combining this with unsecured business credit allows you to cover down payments while maintaining your personal cash reserves for unexpected repairs or new opportunities.

Can I get real estate funding with a low credit score?

You can secure funding with a lower score through asset-based lenders like hard money providers, but it comes at a premium. These lenders prioritize the property's value and your exit strategy over your personal history. However, your interest rates will likely be at the higher end of the 9.5% to 14% range. Improving your score remains the most effective way to lower your cost of debt and access flexible 0% interest options.

What are the requirements for 0% interest business funding for real estate?

Securing 0% interest business funding generally requires a personal credit score of 700 or higher and a clean credit report. Lenders look for a history of responsible credit management and low debt utilization. This capital is unsecured, meaning it doesn't require property as collateral. It serves as an excellent tool for gap funding, allowing you to bridge the distance between your senior loan and the total purchase price of a new asset.

How does hard money differ from traditional real estate investment funding?

Hard money differs from traditional lending by focusing on the asset's value rather than the borrower's personal income. Traditional bank loans are slow, often taking over 45 days to close, and involve extensive red tape regarding your personal financial history. Hard money lenders can often close in 10 to 18 days. While the interest rates are higher, the speed and flexibility allow you to win deals in a competitive acquisition market.

Is it possible to fund a real estate deal with no money down using business credit?

It's possible to achieve a no money down deal by strategically using 0% business credit to cover your down payment. You use the unsecured business capital to satisfy the 20% to 25% equity requirement of a senior lender or a DSCR loan provider. This approach allows you to acquire property without depleting your personal savings. It’s a sophisticated method used by professional investors to maintain high levels of liquidity while scaling their portfolios.

How long does it take to secure funding for a real estate project?

The timeline depends on the specific funding for real estate investors you choose. Traditional institutional loans usually take 30 to 60 days due to rigorous underwriting. DSCR loans are faster, typically closing within 21 to 30 days. Hard money lenders are the quickest, with some able to fund a project in as little as 10 to 18 days. Planning your capital stack early ensures you can meet the closing dates required by your purchase contract.

Do I need an LLC to get funding for real estate investors?

While you can buy property in your own name, having an LLC is often necessary to access the best commercial funding products. Most DSCR and business credit lenders require the borrower to be a legal entity rather than an individual. This structure protects your personal assets from liability and helps you build a separate business credit profile. It also aligns with the new 2026 reporting rules for entity-based residential transfers.

What is the difference between residential and commercial real estate financing options?

Residential financing for 1 to 4 units is typically based on your personal debt-to-income ratio and credit history. Commercial financing for 5 or more units focuses on the property’s ability to generate net operating income. Commercial loans often have different terms, such as shorter amortization periods or balloon payments. Understanding these differences is essential as you transition from single-family homes into multi-family or commercial assets to accelerate your portfolio growth.