Common Business Credit Report Errors: A 2026 Checklist for Repair and Funding Success

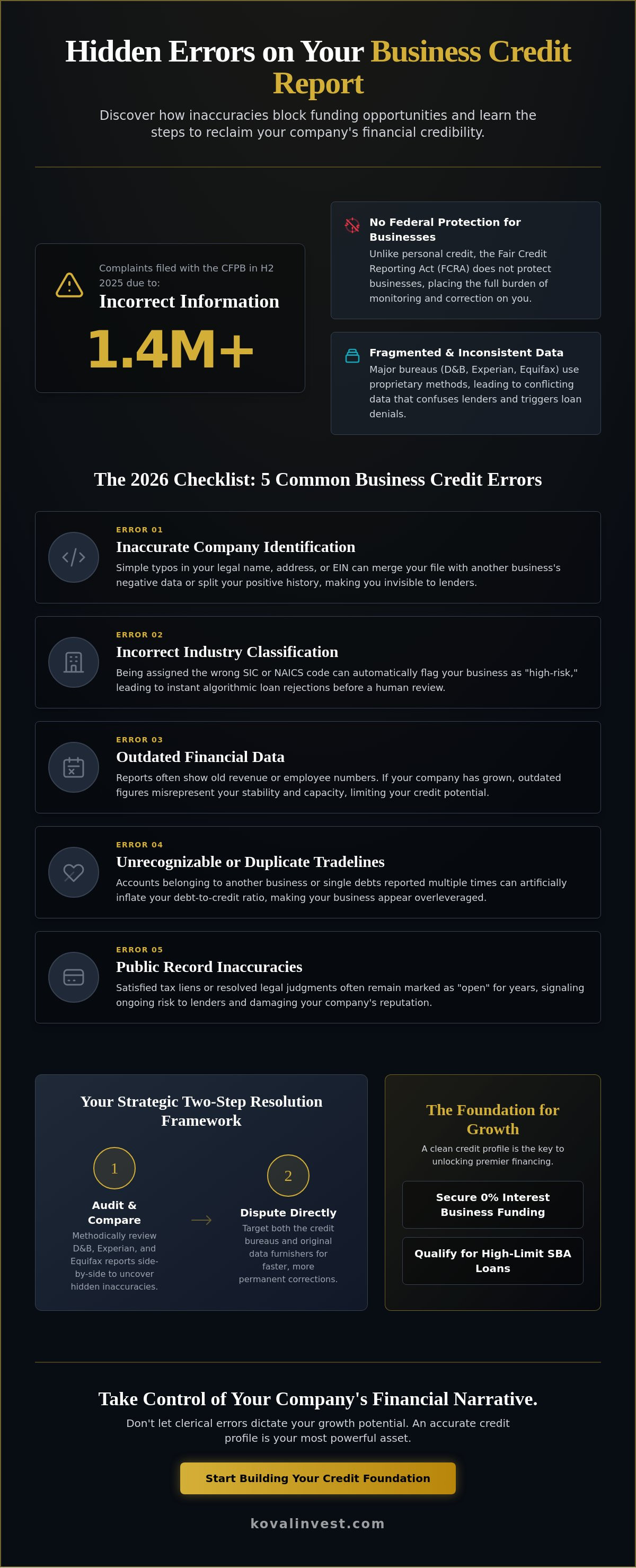

Did you know that in the second half of 2025, incorrect information accounted for over 1.4 million credit reporting complaints filed with the CFPB? If you've faced an unexplained loan denial or high interest rates despite strong revenue, your company is likely suffering from business credit report errors that misrepresent your risk profile to lenders. Unlike personal credit, there's no federal law like the FCRA to protect your business. This means the burden of monitoring and correcting your data falls entirely on your shoulders.

We understand the frustration of seeing conflicting scores across Dun & Bradstreet, Experian, and Equifax while your scaling plans remain on hold. You've worked hard to build a profitable enterprise, and a clerical mistake shouldn't stand in the way of your progress. This article will show you how to identify and resolve the most damaging inaccuracies on your profile to unlock 0% interest funding and SBA loan eligibility. We'll provide a 2026 checklist for auditing your files, managing bureau-specific dispute timelines, and positioning your business for the higher credit limits you need to scale effectively.

Key Takeaways

- Understand how fragmented data across major bureaus creates inconsistencies that lead to unexplained loan denials and high interest rates.

- Identify the five most common business credit report errors, ranging from high-risk industry codes to simple clerical typos in your company identification.

- Learn a methodical audit process to compare Dun & Bradstreet, Experian, and Equifax reports side-by-side to uncover hidden inaccuracies.

- Follow a strategic two-step dispute resolution framework that targets both the credit bureaus and the original data furnishers for faster results.

- Discover how a clean credit profile serves as the essential foundation for securing 0% interest business funding and qualifying for SBA loans.

What Are Business Credit Report Errors and Why Do They Occur?

Business credit report errors are more than just simple clerical mistakes. They represent a fundamental misalignment between your company's actual performance and its reported risk profile. These inaccuracies include outdated financial data, incorrect legal names, or even accounts that don't belong to your entity at all. Essentially, any piece of data that is incomplete or inaccurate can negatively impact your company's perceived creditworthiness, making you look like a higher risk to lenders than you actually are.

The primary reason these errors occur is the fragmented nature of the commercial data industry. Each credit bureau operates as an independent entity with its own proprietary data collection methods. Unlike the consumer world where reporting is largely standardized, business data is often inconsistent. One bureau might receive data from a specific vendor while another does not. This leads to conflicting information across different profiles, causing confusion for both owners and lenders. These errors often stay hidden for months or years, only surfacing when a loan application is denied or an interest rate comes back unexpectedly high.

The Difference Between Personal and Business Credit Errors

A major challenge for business owners is the lack of Fair Credit Reporting Act (FCRA) protections for corporate entities. While consumers have a legal right to a mandated timeline for dispute resolution, businesses don't. Commercial bureaus rely on voluntary data reporting from vendors. If a vendor stops reporting your positive payment history, your score might drop through no fault of your own. Additionally, business identity theft is significantly harder to spot than personal theft. There are no automatic alerts for new corporate credit inquiries, meaning a fraudulent account could exist on your profile for a long time before you notice it.

The Ripple Effect on Your Business Valuation

Your credit health is a key indicator of your company's operational stability. During Mergers and Acquisitions (M&A), poor credit scores can lead to lower valuations as buyers perceive higher financial risk. Accurate reporting is essential for strategic planning and long-term expansion. If you're preparing for a transition or seeking investment, a clean report is a prerequisite for a professional business valuation. Maintaining an error-free profile ensures that your business is positioned as a reliable, stable asset for future growth.

The 2026 Checklist: 5 Common Business Credit Report Errors

Maintaining a high score is only part of the equation. Lenders make decisions based on the raw data behind the scenes. If that data is flawed, even a profitable company can look like a liability. It's essential to monitor your business credit reports to ensure your profile reflects your current operational reality. Here are the five most common business credit report errors we see in 2026.

- Inaccurate Company Identification: Small typos in your legal name, address, or Employer Identification Number (EIN) can cause your credit history to split into multiple files or merge with another business's negative data.

- Incorrect Industry Classification: This is a frequent issue where a business is assigned the wrong Standard Industrial Classification (SIC) or North American Industry Classification System (NAICS) code.

- Outdated Financial Data: Reports often display revenue figures or employee counts from several years ago. If your company has grown significantly, these old numbers can make you appear less stable than you are.

- Unrecognizable Tradelines: Accounts that don't belong to your business or single accounts that are double reported can skew your debt to credit ratios.

- Public Record Inaccuracies: Tax liens or legal judgments that have been fully satisfied often remain marked as "open" on bureau files.

Industry Code Errors: The Silent Loan Killer

Many entrepreneurs don't realize that banks use SIC and NAICS codes to automate the initial stages of loan approval. If your code flags you as a high risk industry, your application might be rejected by an algorithm before a human ever sees it. For instance, a marketing consultant accidentally labeled under "financial services" will face much stricter scrutiny and higher interest rates. You should verify your classification across Dun & Bradstreet, Experian, and Equifax to ensure you aren't being unfairly penalized. If you find your codes are misaligned, our credit repair services can help you navigate the correction process with the bureaus.

Tradeline Discrepancies and Payment History

Your PAYDEX score and other credit metrics rely heavily on the promptness of your payments. Common errors include on time payments being reported as late or, more frequently, positive payment history not being reported at all. Since reporting is voluntary, your largest vendors might not be sharing your data. This missing information can significantly lower your score. Ensuring these tradelines are present and accurate is vital for building the credit depth required for large scale funding and long term growth.

How to Audit Your Business Credit Profile for Inaccuracies

A comprehensive audit requires more than a cursory glance at your PAYDEX score. Identifying business credit report errors requires a methodical approach across all three major bureaus: Dun & Bradstreet, Experian Business, and Equifax Small Business. Each of these entities maintains a separate file on your company, and they rarely communicate with one another. You should pull your full reports from all three to ensure you have a complete view of your financial standing.

Once you have your reports, create a side-by-side comparison spreadsheet. List every tradeline, inquiry, and public record across three columns. This visual layout makes it much easier to spot inconsistencies, such as an account appearing on Experian but not D&B, or a balance that doesn't match your internal records. Focus specifically on the 'UCC Filings' section. These filings represent security interests lenders have in your assets. Often, a loan is paid off, but the lender fails to terminate the UCC filing, which can block you from securing new capital. Similarly, review the 'Inquiry' section for any credit pulls you didn't authorize, as these can be early warning signs of identity theft or clerical mix-ups.

Cross-Bureau Data Reconciliation

It's common to find that your D&B report looks perfect while Equifax shows a default. This happens because vendors choose which bureaus they report to. You must ensure your EIN and legal address match exactly across all platforms. Even a small variation, like "Street" versus "St.", can cause a bureau to create a duplicate, "thin" file that lacks your positive history. Data fragmentation is the primary cause of bureau discrepancies, occurring when credit bureaus collect and interpret information from different sources at different times. If you discover inaccuracies, you have the right to dispute an error on your credit report, but the process is more manual for businesses than for individual consumers.

Preparing Your Evidence File

Before you contact a bureau, you need a robust evidence file. Gather bank statements, cancelled checks, and lien release documents that prove your side of the story. Organize these documents by account number and bureau to keep your communication clear and professional. Bureaus are more likely to act quickly when they're presented with undeniable, well-organized proof. Many entrepreneurs find this process overwhelming, which is why credit repair for business owners has become a vital tool. These services automate the audit and evidence-gathering phases, ensuring that your business credit report errors are handled with the precision required to restore your funding eligibility.

Strategic Dispute Resolution: How to Fix Business Credit Errors

Resolving inaccuracies on a commercial profile requires a tactical, two-pronged approach. You can't simply click a "dispute" button and expect a permanent fix. To effectively resolve business credit report errors, you must simultaneously address the credit bureau and the data furnisher. The data furnisher is the original creditor or vendor that provided the information. If you only notify the bureau, the furnisher might accidentally report the same incorrect data the following month, causing the error to reappear on your file.

A successful resolution follows a methodical timeline. Once your evidence is gathered, follow these steps:

- Step 1: Send a formal written dispute to the credit bureau including specific evidence for every claim.

- Step 2: Send a concurrent notification to the data furnisher to ensure they update their internal records.

- Step 3: Track the 30-day investigation window. While business bureaus aren't strictly bound by the FCRA, most maintain a policy of responding within this timeframe.

- Step 4: Escalate any unresolved disputes through professional consulting or legal channels if the bureau remains unresponsive.

- Step 5: Perform a fresh credit pull after 45 days to verify the correction has been permanently applied.

Online vs. Certified Mail Disputes

While online portals are convenient, certified mail with a return receipt remains the gold standard for commercial disputes. Online forms often limit the amount of evidence you can upload and force you to choose from a pre-set list of reasons. A physical letter allows you to provide a nuanced explanation of complex transactions. It also creates a legal paper trail that bureaus cannot easily dismiss. When you send a physical evidence pack, you're signaling that your company takes its financial reputation seriously. This level of professional preparation often leads to faster results.

What to Do If the Dispute Is Denied

If a bureau denies your request, don't accept the decision as final. You should immediately request a "Method of Verification." This forces the bureau to disclose how they confirmed the data and who they spoke with at the creditor's office. Often, this reveals a breakdown in communication that you can then address directly. During this time, you can add a "Consumer Statement" to your business file. It's a temporary fix that allows you to explain the discrepancy to potential lenders in 100 words or less. If these hurdles are delaying your growth, leveraging the expertise of a professional SBA loan consultant can help you bypass credit roadblocks. We specialize in navigating these complex financial landscapes to ensure your path to capital remains open. Our team can help you manage the technicalities of credit repair services so you can focus on scaling your operations.

Leveraging a Clean Credit Profile for 0% Interest Funding

A clean credit profile is the primary driver behind your company's ability to secure institutional capital on favorable terms. Once you've successfully navigated the process of resolving business credit report errors, the financial landscape shifts from defensive management to offensive growth. Lenders view an error-free report as a direct indicator of operational precision and financial reliability. This trust allows you to unlock 0% interest business funding, providing a significant competitive advantage by lowering your overall cost of capital during critical expansion phases.

This optimization is especially vital when seeking working capital for business acquisition. In a competitive M&A environment, your ability to move quickly and secure unsecured funding without personal collateral can make or break a deal. A pristine credit profile ensures that you aren't tied down by high interest rates or restrictive covenants that eat into your margins. Instead, you're positioned as a stable, low-risk entity capable of handling larger credit limits and more complex financial structures. By fixing the past, you're effectively clearing the path for future scaling and strategic acquisitions.

Qualifying for SBA Loans with Optimized Credit

The SBA 7(a) loan program is one of the most sought-after funding vehicles, but its entry requirements are rigorous. Banks rely heavily on the FICO SBSS score, which aggregates data from your business and personal reports to assess risk. Most institutions require a minimum score of 155 for streamlined processing. Removing a single outdated judgment or an incorrect industry code can boost your score enough to move your application from manual review to the "automatic approval" zone. If you're preparing an application, our guide on how to fix credit for SBA loan approval provides the technical roadmap you need to meet these strict federal thresholds.

The Path to 0% APR Capital

Pristine credit reports are the gatekeepers to 0% introductory APR capital. Banks only offer these aggressive rates to businesses that show no signs of financial distress or reporting inconsistencies. Even minor business credit report errors can cause a lender to slash your credit limit or deny the 0% offer entirely. Once your reports are cleared, you can strategically stack multiple 0% interest lines to create a massive pool of interest-free working capital. We encourage you to book a consultation to see how our success-based approach helps clients secure six-figure funding. Our philosophy ensures that our interests are perfectly aligned with your growth; we only win when you do. Partnering with Koval Investments provides the strategic planning and credit repair services necessary for a total financial overhaul, turning your credit profile into a reliable engine for long-term success.

Scaling Your Business with a Pristine Credit Profile

Your company's financial reputation is its most valuable asset, yet it remains vulnerable to systemic inaccuracies. The lack of federal oversight means that the responsibility for identifying business credit report errors rests solely on your shoulders. By implementing a methodical audit of the major bureaus and following a strategic dispute resolution process, you transform your credit file from a liability into a powerful tool for growth. A clean profile isn't just about a higher score; it's the foundation for accessing the low-cost capital required to scale your operations without unnecessary financial friction.

At Koval Investments, we act as your steady partner in this complex financial landscape. We specialize in success-based credit restoration and are dedicated specialists in 0% interest business funding. Whether you need expert SBA loan consulting or a comprehensive strategy for unsecured capital, our team ensures your interests are always prioritized. Secure your 0% interest funding by optimizing your credit today with Koval Investments. It's time to stop letting clerical mistakes dictate your company's future and start building the legacy your hard work deserves.

Frequently Asked Questions

How long does it take to fix an error on a business credit report?

Fixing an error typically takes between 30 and 45 days, though specific bureaus move at different speeds. Dun & Bradstreet often resolves disputes in 10 to 14 days, while Experian aims for 30 days. Equifax can be significantly slower, sometimes taking six months or longer to complete an update. It's essential to track your submission and follow up to ensure your scaling plans aren't delayed.

Can business credit report errors affect my personal credit score?

Business credit report errors generally don't impact your personal score directly because they are distinct financial profiles. However, if you've personally guaranteed a loan, an error that causes a reported default could spill over into your personal history. Maintaining a clear separation between these entities is a core part of strategic planning for any growing enterprise.

Will a business credit bureau automatically fix errors if I provide proof?

Bureaus won't automatically update your profile simply because you've provided evidence. They must first verify your claims with the original data furnisher. If the creditor fails to respond or disputes your proof, the bureau may leave the incorrect data in place. This is why it's critical to notify both the bureau and the creditor simultaneously to ensure your records are synchronized.

What is the most common error found on Dun & Bradstreet reports?

Duplicate files and fragmented data are the most common issues found on Dun & Bradstreet reports. These errors usually occur when vendors report your information using slight variations of your legal name or address. This creates multiple "thin" files that don't reflect your full creditworthiness. Resolving these duplicates is essential for consolidating your positive payment history into a single, strong PAYDEX score.

Do I need a lawyer to dispute business credit report errors?

A lawyer isn't required to dispute inaccuracies on your commercial profile. Most business owners successfully resolve disputes by following a structured, evidence based process or by partnering with a trusted advisor. Legal counsel is typically only necessary in extreme cases where a bureau's persistent negligence causes documented financial loss that cannot be resolved through standard dispute channels.

How often should I audit my business credit profile for inaccuracies?

We recommend auditing your profile at least once every quarter to ensure accuracy. Regular monitoring allows you to catch business credit report errors before they interfere with a major funding round. If you're preparing for an SBA loan or seeking 0% interest funding, you should perform a deep audit at least 90 days before submitting your application.

Can an incorrect SIC code really lead to a loan denial?

Yes, an incorrect SIC or NAICS code can trigger an immediate, automated loan denial. Banks use these classification codes to filter out industries they consider high risk. If a clerical error labels your consulting firm as a gambling or cannabis business, your application will likely be rejected by the lender's software before a human ever reviews your actual financial performance.

What happens if a creditor refuses to correct the information they reported?

You'll need to bypass the creditor and present your evidence directly to the credit bureau's investigation department. If the creditor refuses to correct the data, your bank statements and cancelled checks serve as the final word. You can also add a 100 word statement to your report to explain the situation to future lenders while you work on a permanent fix.