How to Dispute a Collection on Your Credit Report: A Strategic Guide for 2026

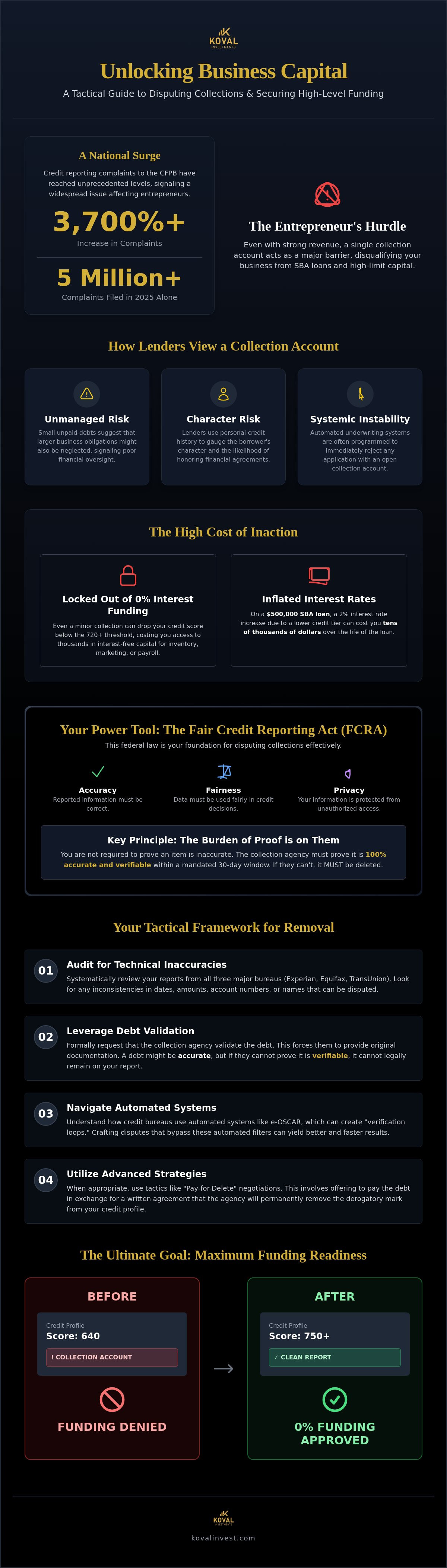

Did you know that credit reporting complaints to the CFPB skyrocketed by over 3,700% recently, reaching more than five million in 2025 alone? If you're an entrepreneur looking to scale, learning how to dispute a collection on your credit report isn't just about cleaning up the past; it's a strategic move for your future capital. It's frustrating to watch an outdated collection account stand between your business and the 0% interest funding you've earned. You likely feel the weight of complex legal jargon and the fear that one wrong move might reset the statute of limitations.

This guide provides a tactical framework to navigate these complexities with confidence. You'll master the process of removing inaccurate collections to optimize your financial profile for high-level capital procurement. We'll explore the current 2026 FCRA response timelines, the critical 30-day dispute window, and the exact steps to position yourself for institutional-grade credit limits and sustainable growth.

Key Takeaways

- Understand how a single collection account can disqualify your business from SBA loans and high-limit capital procurement despite strong revenue.

- Master the tactical steps of how to dispute a collection on your credit report by auditing technical inaccuracies across all three major bureaus.

- Learn to utilize debt validation and pay-for-delete strategies to permanently remove derogatory marks from your financial profile.

- Discover the "verification loop" used by credit bureaus and how to navigate automated systems like e-OSCAR for better results.

- Position your credit report for maximum funding readiness to qualify for 0% interest funding solutions and strategic business growth.

The Strategic Impact of Collections on Capital Procurement

Many entrepreneurs mistakenly believe that high business revenue can compensate for a damaged personal credit profile. In reality, institutional lenders view your personal credit as a direct reflection of your fiscal responsibility. A single collection account, regardless of the amount, signals "unmanaged risk" to automated underwriting systems. This perception can lead to an immediate rejection for high-level capital, such as SBA loans or unsecured business lines of credit. When you understand how to dispute a collection on your credit report, you aren't just performing administrative cleanup; you're removing a barrier to institutional-grade funding.

Viewing credit optimization as a high-ROI business investment is the hallmark of a savvy owner. The capital you can't access because of a $100 collection could represent the difference between scaling your operations or stagnating. In 2026, lenders have become increasingly selective. They prioritize "clean" files that demonstrate a history of resolving financial obligations. By proactively managing your report, you position your business as a safe bet for significant capital injections. To a lender, a collection suggests:

- A lack of financial oversight: Small debts that go to collection imply that larger business debts might be neglected.

- Character risk: Lenders use personal credit to gauge the likelihood of a borrower honoring their agreements.

- Systemic instability: Automated filters often reject any application with an open collection, regardless of other positive factors.

Collections and the 0% Interest Funding Barrier

Securing a 0% interest business funding solution requires a near-pristine credit report. These lenders often operate on a "threshold effect" where a score drop from a minor collection can disqualify you. Even a $50 utility bill from years ago can pull a score below the 700 or 720 requirement. This small oversight effectively locks you out of thousands of dollars in interest-free capital that could have been used for inventory, marketing, or payroll.

The Cost of Inaction: Higher Interest Rates

The financial impact of a collection account extends beyond simple denials; it manifests in the interest rates you're offered. On a $500,000 SBA loan, a mere 2% increase in your interest rate due to a lower credit tier can cost you tens of thousands of dollars over the life of the loan. This is why professional credit repair is a prerequisite for effective SBA loan assistance. Utilizing the protections found in the Fair Credit Reporting Act (FCRA) allows you to challenge inaccuracies and avoid the "verification loops" that often trap DIY applicants. Taking the time to learn how to dispute a collection on your credit report ensures your business isn't overpaying for the capital it needs to thrive.

Your Rights Under the Fair Credit Reporting Act (FCRA)

The Fair Credit Reporting Act (FCRA) is the primary federal legislation that governs how consumer financial data is collected, stored, and shared. For any business owner, understanding this law is the foundation of learning how to dispute a collection on your credit report effectively. The FCRA is built upon a triad of rights: accuracy, fairness, and privacy. This means that any entity reporting information about you must ensure the data is correct, used fairly for credit decisions, and kept private from unauthorized parties. Without these protections, the credit reporting system would lack the integrity required for modern capital markets.

One of the most powerful aspects of the FCRA is that the burden of proof rests entirely with the furnisher of the information, which is typically the collection agency. You aren't legally required to prove a debt is inaccurate; the agency must prove it is accurate and that they have the right to report it. Once you file a formal dispute, the credit bureaus generally have a 30-day investigation window to verify the claim. This timeline is mandated by federal law. If the bureau or the furnisher fails to confirm the details within this timeframe, the item must be deleted from your profile immediately.

Accuracy vs. Verifiability

There is a significant legal distinction between information being "accurate" and it being "verifiable." A collection might technically belong to you, but if the agency lacks the original contract or a complete payment history to verify it, it cannot remain on your report. Missing documentation is a common vulnerability for third-party debt buyers who purchase accounts in bulk. Federal law requires that reported data meet both standards. If you're looking for professional guidance to navigate these nuances, our team at Koval Investments can help align your credit profile with institutional requirements.

The Danger of Online Bureau Portals

While credit bureaus promote their online dispute tools as a convenience, they often serve the bureau's interests more than yours. Clicking through an online portal frequently involves agreeing to terms that can limit your right to future appeals or secondary disputes. Professional consultants almost exclusively use certified mail with return receipts to maintain a strict paper trail. This physical record is essential if the bureau fails to follow the guidelines for Disputing Errors on Your Credit Reports. A physical record prevents the bureau from claiming they never received your request and provides the leverage needed for higher-level escalations. Mastering how to dispute a collection on your credit report requires this methodical, documented approach to ensure your rights are fully protected.

The Step-by-Step Tactical Dispute Process

Transitioning from legal theory to tactical execution requires a methodical approach. Understanding how to dispute a collection on your credit report involves more than just sending a letter; it requires a surgical analysis of the data provided by the bureaus. This process begins with obtaining your files from Equifax, Experian, and TransUnion. While many consumers rely on third-party apps, you need the raw data found in your official disclosures to see the technical details that automated systems often hide. Once you have these reports, you can begin a multi-step audit designed to identify the leverage needed for a permanent deletion.

The tactical process follows a logical progression:

- Step 1: Audit all three major bureau reports to find inconsistencies between them.

- Step 2: Identify technical inaccuracies such as incorrect dates, balances, or account numbers.

- Step 3: Draft a factual dispute letter that focuses on these unverified data points.

- Step 4: Submit your package via certified mail with a return receipt requested to establish a legal timeline.

- Step 5: Review the investigation results within 30 to 45 days and plan your secondary escalation if the item isn't removed.

Auditing for Technical Inaccuracies

Technical inaccuracies are often the most effective path to a successful deletion. You should look for mismatches in the "Date of Last Activity" or the "Original Creditor" name across the different bureaus. A small typo in an account number or a balance that differs by even a few dollars is enough to challenge the integrity of the entire reporting. If one bureau reports a collection as "open" while another reports it as "closed," you have found a clear violation of the accuracy requirements. Cross-referencing these files allows you to pinpoint exactly where the furnisher has failed to maintain consistent records.

Drafting the Factual Dispute Letter

When you dispute an error on my credit report, you must avoid "templated" language. Credit bureaus use automated scanning systems like e-OSCAR to categorize disputes. If your letter looks like a generic form found online, it's likely to be rejected as "frivolous." Instead, be concise and factual. State exactly which account is incorrect, why it's incorrect, and demand that the bureau provide the proof or delete the entry. Every valid dispute package must include a copy of your government-issued ID, a current utility bill or bank statement for residency proof, and a clearly marked copy of the credit report showing the specific entry in question. Following this methodical path is the most reliable way to learn how to dispute a collection on your credit report while protecting your future funding eligibility.

Advanced Tactics: Debt Validation and Pay-for-Delete

While factual audits are a primary defense, advanced strategies like debt validation and pay-for-delete agreements offer additional leverage for business owners. When you analyze how to dispute a collection on your credit report, you'll find that some debts are technically accurate in their balance but legally unverified in their ownership. Debt validation is the process of demanding that a collection agency provide specific evidence of their right to collect. This isn't just a simple computer printout; it requires proof of the original contract and the chain of title for the debt. If the collector cannot produce these documents, they must cease collection activities and remove the entry from your report.

A critical component of this strategy is avoiding any action that acknowledges the debt. Simply calling a collector to discuss an old account can inadvertently reset the statute of limitations in some jurisdictions. This "clock" determines how long a creditor has the legal right to sue you for a balance. By maintaining a professional distance and communicating only through written, certified mail, you protect your legal standing. You should view these interactions as a formal negotiation where your credit score is the most valuable asset on the table.

Executing a Pay-for-Delete Agreement

A pay-for-delete agreement is a specialized negotiation where you offer to pay a portion of the debt in exchange for its complete removal from your credit report. The golden rule here is simple: get the agreement in writing before sending a single penny. Verbal promises from collection agents are generally unenforceable and often lead to the debt being marked as "paid collection," which still damages your score. Your written offer should explicitly state that payment is contingent upon the total deletion of the account from all three bureaus. This approach ensures a win-win outcome where the collector receives funds and you regain your financial eligibility.

The Debt Validation Clock

Timing is everything when you use the law to your advantage. Under the Fair Debt Collection Practices Act, you have a 30-day window after receiving the initial validation notice to dispute the validity of the debt. If you file your dispute within this period, the collector must stop all collection efforts until they provide verification. Proper validation must include the original creditor's name and the specific amount owed. For complex cases involving high-stakes funding, utilizing professional business credit repair services can ensure these timelines are met with precision. If you're ready to clear these hurdles and unlock institutional capital, consider our Credit Repair Services to start your strategic optimization journey.

Professional Credit Optimization for Funding Readiness

While the tactical steps outlined in this guide provide a solid foundation for how to dispute a collection on your credit report, high-stakes funding environments often demand a higher level of precision. Simple errors might be fixed with a basic letter, but persistent derogatory marks often trigger the "verification loop." This is an automated cycle where credit bureaus use the e-OSCAR system to scan dispute letters and issue standardized rejections without conducting a manual review. For a busy entrepreneur, these repetitive rejections represent more than just a nuisance; they are a significant delay in accessing the capital required for expansion.

Professional optimization bridges the gap between a basic consumer dispute and a strategic financial correction. At Koval Investments, we operate on a success-based philosophy that aligns our objectives with your growth. This model ensures that our partnership is a collaborative venture focused on tangible results rather than a traditional expense. We navigate the complexities of bureau algorithms and furnisher requirements so you can remain focused on your daily operations. Our role is to act as a steady hand, ensuring every communication is designed to maximize your eligibility for institutional capital.

Success-Based Credit Restoration

The "insider" advantage comes from understanding how to structure disputes so they bypass automated filters and reach human investigators. This methodical approach is far more efficient for business owners who cannot afford to wait months for a single deletion. By viewing credit repair as a partnership, we create a low-pressure environment where the goal is mutual benefit. We take on the administrative burden and the technical nuances, providing a steady hand in a complex financial landscape. This specialized oversight ensures that your file is handled with the integrity and thoroughness required for long-term success.

From Credit Repair to Capital Injection

A clean credit report is not the final destination; it's the prerequisite for a 0% interest funding application. Once your personal profile is optimized, you can move toward a strategic roadmap for business expansion. This transition allows you to move beyond basic credit lines and explore alternative business funding solutions that offer higher limits and more favorable terms. The final step is securing the capital needed for long-term growth, whether that involves inventory, equipment, or acquisitions. Knowing how to dispute a collection on your credit report is the first move in a larger game designed to secure your business’s financial future and unlock the doors to institutional-grade capital.

Strategizing Your Path to Institutional Capital

Mastering the tactical steps of how to dispute a collection on your credit report is more than a simple administrative fix; it's a fundamental business investment. By auditing your reports for technical errors and leveraging your rights under the FCRA, you remove the "unmanaged risk" signals that block institutional lenders. Whether you're navigating debt validation or negotiating pay-for-delete agreements, each action moves you closer to the pristine profile required for high-limit funding. A clean report is the cornerstone of your financial reputation and the gatekeeper to your business's future growth.

Transitioning from a damaged report to a funding-ready state requires precision and a steady hand. At Koval Investments, we specialize in a success-based approach that ensures our goals are perfectly aligned with yours. Our expertise in 0% interest capital procurement and specialized SBA loan advisory provides the "insider" advantage needed to bypass automated rejection loops. Schedule a Strategic Consultation to Optimize Your Credit for Funding and take the final step toward securing the capital your business deserves. Your expansion is within reach, and we're ready to partner with you to make it a reality.

Frequently Asked Questions

Does disputing a collection lower your credit score?

Disputing a collection does not lower your credit score. The investigation process itself is neutral; your score only changes if the bureau removes the negative item or updates its details. If the dispute is successful, you'll likely see a score increase as the derogatory mark is purged from your profile. If the bureau verifies the item as accurate, your score simply remains where it was before the dispute.

How long does it take for a collection to be removed after a dispute?

You should expect a resolution within 30 to 45 days. The Fair Credit Reporting Act generally gives bureaus 30 days to investigate a claim, though this can extend to 45 days if you provide additional information during the process. Once the investigation concludes, the bureau must notify you of the results within five business days. This timeline ensures a methodical review of your submitted evidence.

Can I remove a collection that is actually mine?

You can remove a collection that belongs to you if the reporting is inaccurate or unverifiable. Federal law requires that every detail, from the balance to the date of last activity, is 100% correct. If a collector can't provide the original contract or proof of ownership, they must delete the entry regardless of whether you once owed the debt. Accuracy and verifiability are the legal standards.

What happens if the credit bureau verifies the collection as accurate?

If a bureau verifies a collection, you have the right to request the specific method of verification they used. You can also file a secondary dispute focusing on different technical inaccuracies or move toward a debt validation request with the collection agency. Persistent follow-up is often necessary to break through automated verification loops. We often help clients navigate these secondary escalations to ensure a thorough review.

Is it better to pay a collection or dispute it first?

It's generally better to dispute a collection first. Paying a collection without a prior agreement often validates the debt and changes the status to a "paid collection," which still damages your score on many models. Disputing allows you to challenge the legal right of the agency to report the item at all. This strategy preserves your leverage for a potential pay-for-delete negotiation later if necessary.

What is the "1-2 punch" method for credit disputes?

The "1-2 punch" method involves sending a debt validation letter to the collector and a dispute letter to the credit bureau simultaneously. This tactical approach forces both parties to coordinate their records within a strict legal timeframe. If the collector fails to verify the debt to you but tells the bureau it's verified, they've committed a violation. This creates significant pressure for the item's removal.

Can a collection agency sue me while a debt is in dispute?

A collection agency can still file a lawsuit, but their ability to pursue active collection is restricted during the initial dispute window. If you dispute the debt within 30 days of receiving their first notice, they must stop all collection efforts until they provide verification. Most agencies avoid the expense of legal action while a formal dispute is pending. This pause gives you time to build your defense.

Does a paid collection still hurt my credit score in 2026?

A paid collection can still negatively impact your credit score depending on the scoring model a lender uses. While newer models ignore paid collections, many institutional lenders in 2026 still rely on older versions for business funding. Learning how to dispute a collection on your credit report for total removal remains the most effective strategy. Total deletion ensures your profile meets the requirements for high-level capital procurement.