How to Secure 0% Financing for Business Acquisition in 2026

What if you could bypass the 9% interest rates currently standard for SBA 7(a) loans and acquire your next company using entirely interest-free capital? For many entrepreneurs, the goal of securing 0% financing for business acquisition feels out of reach in a market defined by high borrowing costs and rigid lending standards. You've likely felt the pressure of high interest rates eating into your projected ROI, or perhaps you've struggled with the strict 10% down payment requirements that the SBA continues to mandate in 2026.

It's a common challenge, but it shouldn't stop you from scaling your portfolio. We believe that strategic acquisition requires a more sophisticated approach than traditional bank debt offers. This guide provides a clear roadmap to interest-free capital by leveraging credit optimization and unsecured funding stacks. You'll learn how to combine 0% APR business credit with seller participation to minimize your personal risk and maximize cash flow. We will explore the specific steps to build a funding structure that works for your long-term success rather than against it.

Key Takeaways

- Understand how a strategic funding stack provides a pathway to interest-free capital, even when traditional market rates remain high.

- Discover how to leverage 0% financing for business acquisition to protect your cash flow and minimize the need for personal liquid capital at closing.

- Learn the advantages of using unsecured credit lines to safeguard your assets while avoiding the strict collateral requirements of standard SBA loans.

- Identify the specific credit optimization and valuation steps necessary to qualify for elite, interest-free funding structures in today's market.

- Explore a collaborative, success-based approach to capital procurement that prioritizes your long-term ROI and operational stability.

The Reality of 0% Financing for Business Acquisition

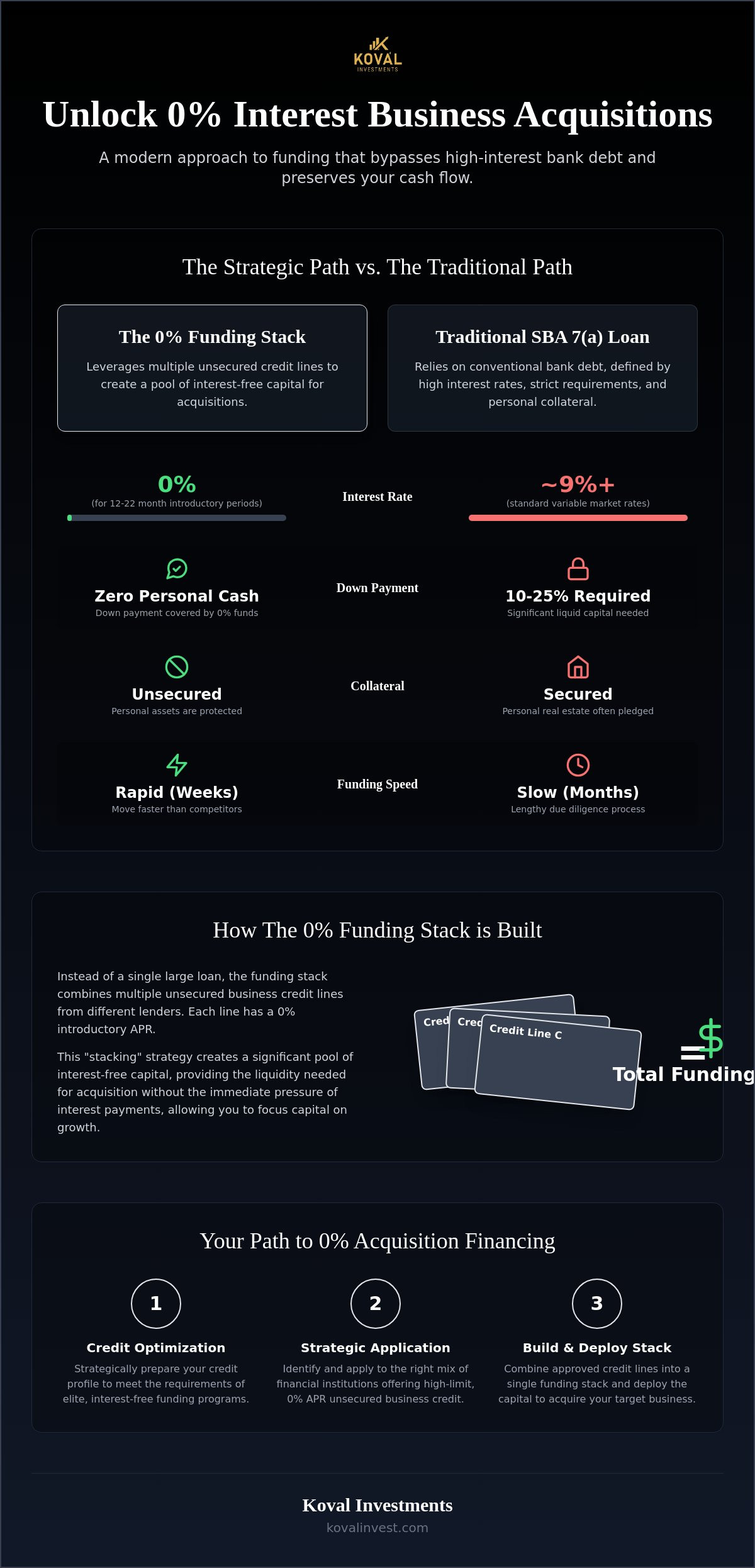

Many entrepreneurs assume that interest-free capital is a myth in the mergers and acquisitions space. However, 0% financing for business acquisition is a practical reality when you transition away from traditional bank models. It involves leveraging introductory 0% APR periods on business credit to fund either the full purchase price or the critical down payment. This strategy allows you to use the bank's money without the heavy burden of interest during the most sensitive phase of the business transition.

Traditional institutions prioritize fixed or variable interest to mitigate their risk. With SBA 7(a) rates hovering around 9% to 9.5% in mid-2026, banks aren't interested in providing interest-free terms. This high-rate environment favors buyers who can navigate alternative structures. This strategic use of capital is a specialized form of a Leveraged Buyout (LBO), where the buyer's creditworthiness and the business's potential serve as the foundation for the funding. By utilizing unsecured business credit lines, you can move faster than competitors who are bogged down by months of bank due diligence.

Why Interest-Free Capital is the Ultimate M&A Lever

Cash flow is the lifeblood of any new acquisition. When you avoid the 9% interest drag of a standard term loan, you preserve capital for immediate operational improvements or marketing. Most SBA loans require you to pledge personal real estate as collateral, which creates significant personal exposure. Choosing an unsecured path protects your home while reducing the total cost of ownership over the life of the investment. It's about maintaining a lean balance sheet from day one.

The 0% Interest Funding Solution vs. Traditional Debt

Our 0% Interest Funding Solution focuses on actual 0% APR periods rather than deferred interest, which can be predatory if not managed correctly. These funds are often used to cover the 10% to 25% down payment required by larger institutional lenders, effectively eliminating the need for personal liquid cash. It's a more surgical approach to debt. A 0% funding stack is a combination of multiple unsecured lines optimized to provide maximum liquidity without interest charges. This structure ensures you aren't over-leveraged while you work to increase the profitability of your new entity.

The 0% Funding Stack: How It Works for Buyers

Securing 0% financing for business acquisition is rarely the result of a single loan from a traditional bank. Instead, successful buyers utilize a "funding stack." This strategy involves combining multiple unsecured business credit lines to create a significant pool of interest-free capital. By spreading the acquisition cost across several 0% APR introductory offers, you can fund a purchase without the immediate burden of 9% interest rates. This methodical approach allows you to leverage the bank's money while your new business scales its profitability.

The primary advantage of this stack is its unsecured nature. Traditional lenders often require you to pledge personal real estate or specific business assets as collateral. In contrast, the 0% funding stack relies on your credit profile and business viability. This protection ensures that your personal wealth remains insulated from the risks inherent in a new acquisition. It's a collaborative way to grow, where the capital is tied to your strategic execution rather than your home equity.

Unsecured Business Credit Lines Explained

In 2026, many leading financial institutions offer introductory periods ranging from 12 to 22 months with 0% APR on purchases. These lines are the engine of the funding stack. By identifying the right mix of lenders, you can access substantial liquidity for the acquisition. Some buyers also use a "cycling" strategy. This involves using the business's monthly cash flow to pay down the principal on one line while utilizing another, effectively extending the interest-free window. This requires disciplined financial management but offers a massive ROI advantage over traditional debt.

Bridging the Gap: 0% Capital and SBA Loans

One of the most effective ways to use these funds is to cover the equity injection required for the SBA 7(a) program. While the SBA provides the majority of the acquisition capital, they still mandate a minimum 10% down payment from the buyer. Using interest-free credit lines for this 10% allows you to acquire the business with zero out-of-pocket cash. For a deeper look at how to structure these deals, you can explore our guide on SBA loan assistance. This combination ensures your debt-to-income ratio stays healthy while you focus on post-acquisition growth.

Success in this area depends heavily on the sequence of your applications. If you apply for multiple lines of credit in the wrong order, you risk triggering fraud alerts or damaging your credit score, which can halt the entire process. Capital procurement services are essential for mapping out this timeline. Our team at Koval Investments specializes in architecting these specific lending sequences to ensure you receive the maximum possible funding with the lowest possible risk.

Comparing 0% Acquisition Capital vs. Traditional SBA Loans

Choosing the right capital structure is often more important than the purchase price itself. While the SBA 7(a) loan is a common choice, current market conditions in 2026 have made it an expensive one. With the Prime Rate holding at 6.75%, most SBA acquisition loans now carry total interest rates between 9.0% and 9.5%. Choosing 0% financing for business acquisition allows you to sidestep these heavy interest payments entirely during your first 12 to 22 months of ownership. This shift in strategy can be the difference between a struggling transition and a high-growth takeover.

Speed is another critical factor where the two models diverge. Traditional bank committees often require three to six months to finalize an acquisition loan, which can cause sellers to lose patience or seek other buyers. A 0% funding stack, however, can often be assembled in just a few weeks. This agility allows you to move faster on high-value opportunities. For a broader look at the landscape of financing a business acquisition, it's clear that those who diversify their capital sources often secure better terms than those relying on a single lender.

Cost of Capital Analysis

The financial impact of interest-free capital is most visible when you look at your monthly debt service. During the first 18 months of ownership, every dollar saved on interest is a dollar that can be reinvested into the company's marketing, equipment, or staff. This significantly accelerates your break-even point and improves your overall ROI. While a $250,000 interest-free stack allows every dollar of your payment to reduce the principal balance, a $250,000 SBA term loan at 9.5% interest results in over $35,000 in interest expenses alone during that same period.

Risk Mitigation and Asset Protection

One of the hidden dangers of traditional bank debt is the "blanket lien." Most SBA lenders require a lien on all business assets and often a personal guarantee backed by your primary residence. This creates a high-stakes environment where your personal life is directly tied to the business's performance. Unsecured 0% financing for business acquisition provides a layer of protection by decoupling your personal assets from the transaction. This strategy ensures that your home and other investments remain insulated from business risks. To understand how this fits into a broader growth plan, you should review our guide on Alternative Business Funding Solutions. By limiting the lender's reach, you maintain the flexibility needed to scale your portfolio with confidence.

Step-by-Step: How to Qualify for 0% Acquisition Financing

Securing 0% financing for business acquisition isn't a matter of luck or timing. It's a structured process that begins long before you sign a purchase agreement. While many lending platforms suggest a simple "apply and see" approach, elite funding stacks require a higher level of preparation to ensure you access the maximum possible limits without triggering bank fraud alerts. Following a logical progression allows you to build a capital base that supports your growth without the drag of immediate interest expenses.

- Step 1: Conduct a professional business valuation of the target entity to confirm it can support the eventual principal repayment.

- Step 2: Optimize your personal and business credit profiles to meet the rigorous standards of top-tier lenders.

- Step 3: Execute a coordinated "funding run" where multiple applications are submitted in a specific, strategic sequence.

- Step 4: Deploy the capital for the acquisition or use it to cover the required down payment for a larger loan.

- Step 5: Implement strategic planning for post-acquisition growth to maximize cash flow during the interest-free window.

The Critical Role of Credit Optimization

A 720+ FICO score is the essential baseline for high-limit 0% APR offers in 2026. Lenders are increasingly selective, and even minor inaccuracies on your report can suppress your borrowing power by tens of thousands of dollars. You must identify and remove these errors before initiating any applications. If your profile isn't quite there yet, you can learn more about the process in our guide on Mastering Business Credit Repair Services. Clean credit doesn't just get you approved; it determines the total volume of capital you can secure for your acquisition.

Business Valuation and Strategic Alignment

A professional business valuation serves a dual purpose. It helps you negotiate a fair price with the seller while allowing you to align your funding stack with the business's projected cash flow. You need to verify that the target entity can support the eventual principal repayment once the introductory interest-free period expires. This due diligence phase is where professional consulting provides the most value, as it prevents you from over-leveraging a business that lacks the margins to sustain its debt. Success depends on selecting an acquisition target that is fundamentally sound and ready for scale.

If you're ready to see how your current credit profile aligns with these requirements, schedule a strategy session with our team today to begin your capital procurement journey.

Partnering with Koval Investments for Your Acquisition

Choosing a partner for your next venture is a decision that impacts your financial trajectory for years. At Koval Investments, we operate on a success-based philosophy. This means our objectives are perfectly aligned with yours; we only win when you successfully secure your capital. Unlike large institutional banks that treat you as a transaction number, we provide a personalized experience that bridges the gap between high-level financial strategy and the day-to-day realities of business ownership. We act as a steady hand, guiding you through complex financial landscapes with calm reliability.

Our role extends beyond simple capital procurement. We offer expert Mergers and Acquisitions Consulting to ensure the business you intend to buy is a sound investment. We analyze cash flows and operational efficiency to verify that the 0% financing for business acquisition you receive is deployed into a vehicle capable of scaling. This holistic approach minimizes your risk while maximizing your post-acquisition cash flow. We believe in building long-term relationships based on integrity and pragmatism rather than high-volume transactions.

From Credit Repair to 0% Interest Funding

The process begins with a deep dive into your current financial standing. We don't just look at a surface-level score; we examine the underlying data. We identify and fix credit report errors that would otherwise block you from accessing top-tier 0% financing for business acquisition. Once your profile is optimized, we architect a custom 0% funding stack tailored to the specific needs of your deal. For a comprehensive breakdown of this methodology, you can read The Ultimate Guide to 0% Interest Business Funding. This ensures you have the liquidity required to close without the immediate drag of interest payments.

Next Steps: Securing Your Interest-Free Capital

The path to interest-free capital is methodical and deliberate. It starts with an initial consultation where we assess your goals and financial profile. From there, we create a 90-day roadmap to acquisition readiness. This timeline allows for credit restoration, business valuation, and the strategic sequencing of applications. We serve as your mentor and insider, navigating the complexities of the lending environment alongside you. This methodical approach reinforces our image as a careful partner that values thoroughness over quick, superficial wins. If you're ready to buy, contact Koval Investments for a strategic funding consultation.

Strategic Capital for Your Next Acquisition

The financial environment of 2026 requires a departure from traditional, high-interest debt models that often hinder growth. Specialized 0% interest funding stacks provide a superior alternative to standard bank loans, allowing you to preserve cash flow during the critical first year of ownership. By focusing on credit optimization and the strategic sequencing of applications, you can secure the liquidity needed to close deals faster while protecting your personal assets from unnecessary risk.

Your success depends on a clear roadmap and a partner who understands the nuances of 0% financing for business acquisition. Our success-based funding philosophy ensures that we're fully invested in your outcome, providing expert M&A and valuation consulting to verify the strength of your target entity. We align your capital needs with your long-term goals to ensure your transition is smooth and profitable. If you're ready to scale your portfolio with interest-free capital, secure your 0% acquisition funding with Koval Investments. We look forward to helping you navigate these complex structures with confidence and precision.

Frequently Asked Questions

Is it really possible to get 0% financing for a business acquisition?

Yes, it's entirely possible to secure 0% financing for business acquisition by utilizing a coordinated funding stack. This approach doesn't rely on a single bank loan but instead combines multiple introductory 0% APR business credit lines. By sequencing applications correctly, you can access substantial capital to fund a purchase without incurring interest during the first year or more of operations. This strategy requires a robust credit profile and a clear plan for principal repayment.

What credit score do I need for 0% interest business funding?

You generally need a personal FICO score of 720 or higher to qualify for the most competitive 0% interest business funding offers. While some lenders may consider scores as low as 680, the highest credit limits and longest introductory periods are reserved for those with elite credit profiles. Maintaining a low credit utilization ratio and a clean payment history is essential for maximizing your borrowing power during the acquisition phase.

Can I use 0% financing for an SBA loan down payment?

Yes, you can use 0% financing to cover the equity injection required for an SBA 7(a) loan. SBA lenders typically mandate a minimum 10% down payment from the buyer's own funds. By leveraging a 0% interest funding stack, you can provide this capital without depleting your personal liquid savings. This combination allows you to acquire a larger business while keeping your cash reserves intact for post-acquisition growth and operational needs.

How long do 0% interest periods typically last for business credit?

In the 2026 lending market, 0% introductory periods for business credit lines typically last between 12 and 22 months. The specific duration depends on the lender's current policies and your overall creditworthiness. Some specialized cards offer shorter windows of 9 to 12 months, while premium business lines can extend nearly two years. It's vital to map out your repayment schedule to ensure the principal is addressed before the standard market rates apply.

Do I need collateral for 0% interest acquisition capital?

You typically don't need collateral to secure 0% interest acquisition capital through our funding solutions. These credit lines are unsecured, meaning they are granted based on your credit profile and business viability rather than physical assets like real estate or equipment. This structure offers a significant advantage over traditional bank debt, as it protects your personal and business assets from blanket liens while providing the liquidity needed for your transaction.

What happens after the 0% interest period ends?

Once the introductory 0% interest period ends, any remaining balance will begin accruing interest at the card's standard market APR. It's critical to have a clear exit strategy, which may include paying down the balance using the business's increased cash flow or refinancing into a longer-term loan. Some entrepreneurs also choose to cycle their debt into new 0% offers if their credit profile remains strong, effectively extending their interest-free window.

How much 0% funding can I realistically qualify for?

Most qualified individuals can realistically secure between $50,000 and $250,000 in 0% funding through a professionally managed stack. The total amount depends on several factors, including your personal credit score, the age of your business entity, and your existing banking relationships. For larger acquisitions, this capital is often used alongside other financing methods, such as seller notes or SBA loans, to complete the total purchase price without personal cash.

Can I use 0% financing to buy a franchise?

Yes, 0% financing is an excellent tool for buying a franchise, particularly for covering franchise fees and initial working capital. Franchise acquisitions often require a significant upfront investment before the business becomes profitable. Using interest-free capital during the setup and launch phase allows you to scale more quickly without the immediate pressure of monthly interest payments. This approach ensures more of your early revenue stays within the business to support growth.