Strategic Steps to Improve Your Business Credit Profile for 2026 Funding

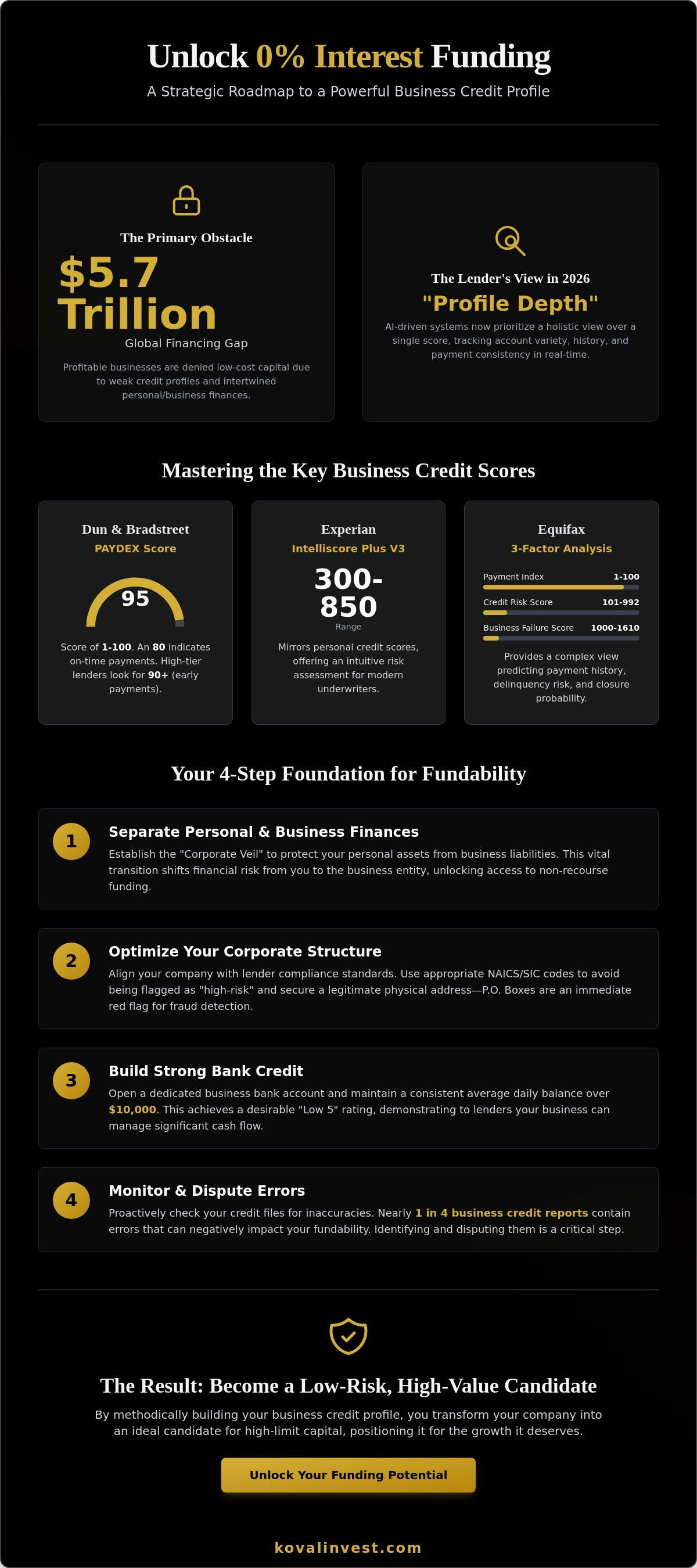

What if the primary obstacle to your company's growth isn't your monthly revenue, but a $5.7 trillion global financing gap that rewards only those who proactively improve business credit profile data? It's incredibly frustrating to build a profitable enterprise only to face SBA loan denials or predatory interest rates because your personal and business finances remain intertwined. You've likely felt the weight of this confusion, wondering why your hard work hasn't yet translated into the low-cost capital you need to scale.

We believe that financial transparency should lead to partnership, not barriers. This article provides the professional-grade steps required to optimize your profile and unlock high-limit, 0% interest funding opportunities. We'll provide a methodical roadmap to help you secure an 80+ Paydex score, separate your personal liability, and master the specific scoring nuances that lenders are looking for in 2026. By following this strategy, you can position your business as a low-risk, high-value candidate for the capital it deserves.

Key Takeaways

- Understand why modern lenders prioritize the overall depth of your financial records rather than just a simple numerical score.

- Ensure your company is legally fundable by selecting the correct industry codes and establishing a clean corporate structure.

- Learn the precise steps to improve business credit profile thickness and reach a Paydex score of 90 or higher.

- Identify and resolve common reporting errors that affect nearly one in four business credit files.

- Master the transition from building a profile to executing a capital strategy that's designed to secure 0% interest funding.

Understanding the Business Credit Profile in the 2026 Lending Landscape

A business credit profile is a comprehensive, multi-bureau record that serves as your company's financial resume. It aggregates data from various sources to show lenders how reliably you manage debt and operational obligations. As we move through 2026, the strategy to improve business credit profile metrics has shifted significantly. Major national banks and alternative lenders no longer rely solely on a single score at the moment of application. Instead, they utilize sophisticated AI-driven monitoring systems that track your profile's performance in real-time. These systems prioritize "profile depth," which evaluates the variety of your accounts, the length of your history, and the consistency of your payment behavior across different economic cycles. Achieving true "credit fundability" is the ultimate goal, signaling to these automated systems that your business is a low-risk partner for high-limit capital.

The Core Components: D&B, Experian, and Equifax

Understanding business credit reports requires looking at how the three primary bureaus interpret your data. Dun & Bradstreet focuses on the PAYDEX score, which ranges from 1 to 100. A score of 80 indicates on-time payments, but high-tier lenders often look for scores closer to 100, which reflect payments made 30 days ahead of schedule. Experian's Intelliscore Plus V3 has adopted a 300-850 range, mirroring personal scores to provide a more intuitive risk assessment for modern underwriters. Equifax provides a more complex view by offering three distinct metrics:

- Payment Index: A 1-100 score reflecting your payment history.

- Credit Risk Score: A range from 101 to 992 that predicts the likelihood of serious delinquency.

- Business Failure Score: A range from 1,000 to 1,610 that forecasts the probability of a company closing within the next 12 months.

These bureaus pull data from trade partners, utility companies, and public records; this creates a holistic view of your operational stability that lenders use to set your borrowing limits.

The Critical Separation of Personal and Business Credit

Many entrepreneurs mistakenly rely on their personal credit to fund business growth, which creates a hard ceiling on their borrowing capacity. Personal debt-to-income ratios are much tighter than business limits, and high utilization on personal cards can damage your individual score. Building a standalone profile allows you to benefit from the "Corporate Veil," which protects your personal assets from business liabilities. When you improve business credit profile depth, you're essentially shifting the financial risk from yourself to the business entity. This transition is vital for moving toward non-recourse funding, where the business's own merit secures the capital. By establishing this separation, you unlock access to 0% interest funding solutions that aren't tied to your personal debt capacity, providing the breathing room needed for strategic expansion.

Establishing a Foundation for High-Limit Business Credit

Building a robust financial identity is a deliberate process that begins long before you submit a loan application. To effectively improve business credit profile scores, you must first align your company with the specific compliance standards that automated lender algorithms use to filter risk. These systems are designed to identify and reject companies that appear unstable or unverified. This starts with your NAICS (North American Industry Classification System) and SIC codes. Some industries, such as real estate investing or transportation, are flagged as "high risk" by banks. Selecting a code that accurately represents your consulting or management activities can significantly impact your approval odds for a 0% interest funding solution.

A dedicated business bank account serves as a non-negotiable cornerstone for your financial foundation. This account creates what is known as "bank credit," which is a measure of your average daily balance over a 90-day period. Most high-limit lenders look for a "Low 5" rating. This means maintaining a consistent balance of at least $10,000. To Establish business credit that carries weight, your bank history must show that the business can handle significant cash flow without falling into the red.

Entity Structuring and Compliance

Lender algorithms check for physical locations to verify legitimacy. P.O. Boxes or UPS Store addresses are immediate red flags for fraud detection. You need a physical office address or a "virtual office" that provides a unique suite number recognized as a commercial location. Additionally, your business must be listed in the 411 directory. While this feels like an old-school requirement, automated underwriting systems still use these directories to verify that a business is legitimate and reachable. Your Secretary of State filings must match your credit records exactly to avoid being flagged as a high-risk entity.

Bureau Registration and Initial Reporting

Consistency is the most overlooked factor when you aim to improve business credit profile data. Your business name, address, and phone number (NAP) must match perfectly across your Secretary of State filing, your IRS EIN records, and your Dun & Bradstreet profile. Even a small discrepancy, like using "St." on one document and "Street" on another, can create fragmented credit files. This fragmentation prevents your positive payment history from aggregating correctly.

Securing your D-U-N-S number through Dun & Bradstreet is the final step in this foundational phase. This nine-digit identifier is the standard for tracking your company's financial health. Once your EIN is correctly linked to your D-U-N-S number, your "firmographic" data becomes the anchor for all future reporting. This ensures that every on-time payment you make is credited to the correct entity, building the "thickness" required for high-limit approvals.

Strategic Tradeline Management and Payment Performance

Tradelines are the individual credit accounts listed on your business report, and they're the primary tool used to improve business credit profile thickness. Each account provides a specific data point that lenders use to assess your reliability. A "thin" profile with only one or two accounts suggests a lack of experience, whereas a "thick" profile demonstrates a history of managing multiple obligations simultaneously. To reach the highest tier of creditworthiness, you must master the "Early Payment Strategy." While paying on the due date earns you a Paydex score of 80, paying 15 to 20 days early is what triggers scores of 90 or higher. This proactive approach signals to automated systems that your business possesses superior cash flow management and lower default risk.

Successfully managing your profile requires a balance between vendor terms and revolving credit. Vendor accounts, often referred to as Net-30 or Net-60 terms, allow you to buy supplies and pay later. These are excellent for building initial "thickness" without high interest costs. Revolving credit, such as business credit cards, provides more flexibility and often comes with higher limits. Combining both types of credit shows that your business can handle different debt structures. This variety is a key indicator of financial maturity that many entrepreneurs overlook when they first consult an SBA guide to establishing business credit for growth.

Selecting the Right Vendor Tradelines

Not all creditors report your positive payment history, which can leave your profile stagnant despite your best efforts. You should prioritize "Tier 1" vendors that report to Dun & Bradstreet and Experian without requiring a personal guarantee. These vendors are usually the easiest to secure when you're just starting. The "magic number" to trigger a reliable business credit score is typically five reporting tradelines. If you're working with "invisible" creditors who don't report, your on-time payments won't help you improve business credit profile data or qualify for larger loans.

Optimizing Debt-to-Credit Ratios

Lenders view high-limit tradelines as a vote of confidence from other financial institutions. A single $50,000 limit is often more valuable than ten $5,000 limits because it demonstrates that a creditor has trusted you with significant capital. You should periodically request limit increases on your existing accounts to lower your overall utilization percentages. Business credit utilization is the percentage of your total available revolving credit currently in use, and maintaining this ratio below 30% is the optimal threshold for 2026 funding approvals. By keeping your balances low relative to your limits, you prove that you don't rely on debt to survive, making you a much more attractive candidate for 0% interest capital.

Identifying and Disputing Business Credit Report Errors

Industry data suggests that nearly 25% of business credit reports contain inaccuracies that can lead to higher interest rates or outright loan denials. These errors often stem from fragmented files, where a single business has multiple records under slightly different names, addresses, or suite numbers. This fragmentation prevents a unified view of your financial health. It makes it nearly impossible to accurately improve business credit profile metrics because your positive payment history is split across incomplete records. A fragmented file might show your on-time payments on one record while a separate, outdated record remains stagnant, effectively hiding your true creditworthiness from potential lenders.

Conducting a professional audit of your reports is the only way to ensure your data is working for you rather than against you. You must look beyond the surface level scores to find the hidden data points that trigger red flags in automated underwriting systems. If your profile is currently holding you back, our team can help you navigate the credit restoration process to secure the capital your business requires.

The Audit Process for Major Bureaus

Your audit should begin with a thorough check for outdated UCC filings. These filings act as liens on your business assets and can block new funding if they remain on your report long after a debt has been satisfied. You also need to verify that closed accounts aren't still showing as open with high balances, as this artificially inflates your debt load. One of the most common business credit report errors involves incorrect SIC or NAICS codes. If your business is misclassified in a high-risk category, such as real estate investing or transportation, you might face automatic denials regardless of your actual score.

Professional Credit Restoration Tactics

Disputing inaccurate data requires a methodical approach backed by concrete supporting evidence. While the business credit world lacks some of the consumer protections found in personal credit, bureaus still have a professional obligation to maintain accurate records. You should provide bank statements, canceled checks, or official lien release documents to prove your case. For many entrepreneurs, the complexity of this process justifies seeking professional credit repair for business owners to ensure disputes are handled correctly the first time. If you're under a tight deadline for a specific funding round, knowing how to fix credit for SBA loan requirements can accelerate your path to approval and help you improve business credit profile depth quickly.

Leveraging Your Improved Profile for 0% Interest Funding

Once you've successfully managed your tradelines and cleared reporting errors, the focus shifts from preparation to active execution. The ultimate reward for the effort to improve business credit profile data is the ability to access high-limit, unsecured capital. A "thick" profile, characterized by multiple reporting accounts and aged history, allows you to utilize a strategy known as credit card stacking. This involves securing multiple business credit lines with 0% introductory APRs simultaneously. Because these accounts are tied to your EIN and don't report to your personal credit, you can access substantial working capital for 12 to 18 months without incurring interest costs or damaging your personal debt-to-income ratio.

Transitioning from building credit to executing a capital procurement strategy requires a shift in mindset. You're no longer just a business owner seeking a loan; you're a strategic partner presenting a low-risk opportunity to a lender. A strong, verified profile is the non-negotiable key to unlocking 0% interest business funding. At this stage, Koval Investments steps in as your advocate to navigate the complexities of bank appetites and underwriting nuances, ensuring you reach the finish line of a funded account.

Preparing for SBA Loan Approval

Even though the SBA has sunsetted certain mandatory scoring requirements, most lenders still use the FICO Small Business Scoring Service (SBSS) to pre-screen applications. While the minimum score was raised to 165 in June 2025, many tier-one lenders in 2026 look for a score of 180 or higher to offer the most competitive terms. Your business credit profile feeds directly into this score. Aligning your data with professional SBA loan assistance requirements ensures that your application passes the initial automated filters. We also recommend conducting business valuations during this phase. This provides a clear picture of your company's worth, which strengthens your position when negotiating large-scale debt acquisition for acquisitions or real estate.

Accessing Unsecured Working Capital

The goal for most high-growth companies is to secure high-limit revolving lines of credit without providing collateral. This level of funding is only available to those who have built a profile that stands on its own merit. Our approach is rooted in a "Success-Based" philosophy, meaning we're equally invested in the outcome of your funding round. We focus on the practicalities of moving from an improved profile to a liquid bank account. By leveraging your 80+ Paydex score and clean bureau records, we help you execute a procurement plan that prioritizes speed and low-cost capital. This collaborative effort ensures your business has the fuel it needs to scale without the burden of high-interest debt.

Securing Your Financial Future Through Strategic Credit Management

Building a fundable business is a methodical journey that requires more than just timely payments. It's about engineering a profile that speaks the language of modern bank algorithms. By establishing a compliant entity and managing reporting tradelines with precision, you've already done the heavy lifting to improve business credit profile depth. You now understand that a thick profile isn't a vanity metric; it's the specific key that unlocks non-recourse capital and high-limit revolving lines.

Since 2018, Koval Investments has focused on national capital procurement through a success-based philosophy. We only win when you get funded. Our expertise in navigating SBA loan requirements and 0% APR stacking allows us to act as your steady hand in a complex financial landscape. We're ready to help you navigate the final mile of your funding journey. Access your 0% interest funding solution with Koval Investments today and take the definitive step toward your company's next phase of growth. Your vision deserves the capital to match.

Frequently Asked Questions

How long does it take to improve a business credit profile?

It typically takes between 90 and 180 days to see significant movement in your scores. This timeline allows enough time for new vendor tradelines to report and for credit bureaus to update their records. Consistency is the most important factor; making early payments every month will steadily improve business credit profile data and demonstrate your company's reliability to automated systems.

Can I build business credit without a personal guarantee?

Yes, you can build a standalone profile by starting with "Tier 1" vendors that don't require a personal guarantee (PG). These vendors report your payment history to bureaus like Dun & Bradstreet based solely on your EIN. Once you've established a "thick" profile with several reporting accounts, you can qualify for larger revolving lines and 0% interest funding without linking your personal assets to the debt.

Does my personal credit score affect my business credit profile?

Your personal credit often plays a role in the early stages of building your business identity. Many lenders use a blended score or check your personal FICO to assess initial risk, especially for new entities. However, the ultimate goal of our strategy is to separate these two profiles entirely. Once your business credit is strong enough, it should stand on its own merit without impacting your personal borrowing capacity.

What is a good business credit score for an SBA loan in 2026?

A FICO SBSS score of 180 or higher is considered excellent for securing competitive SBA loan terms in 2026. While the minimum required score was raised to 165 in June 2025, many top-tier lenders look for 180 to minimize their risk. Additionally, maintaining a Dun & Bradstreet Paydex score of 80 or above shows lenders that you consistently pay your bills on time or ahead of schedule.

How many tradelines do I need to get a high-limit business credit card?

You generally need at least five reporting tradelines to generate a reliable score and qualify for high-limit accounts. Lenders look for a mix of vendor terms and revolving credit to see how you handle different debt structures. Having a variety of accounts helps improve business credit profile thickness, which signals to underwriters that your business is mature enough to manage significant capital responsibly.

What happens if there is an error on my Dun & Bradstreet report?

If you find an inaccuracy, you must file a formal dispute through the bureau's online portal and provide supporting evidence. Errors often include "fragmented" files where your data is split across multiple records or outdated liens that should have been removed. Providing clear documentation, such as bank statements or official lien releases, is necessary to correct these mistakes and ensure your profile reflects your true financial health.

Is it worth paying for professional business credit repair services?

Professional services are a strategic investment if you need to accelerate your path to funding or have complex errors to resolve. Experts understand the nuances of bureau reporting and can often fix issues in a fraction of the time it takes to handle them yourself. This allows you to focus on running your business while a partner ensures your profile is optimized for the highest possible funding limits.

How does 0% interest business funding actually work?

This funding solution involves "stacking" business credit cards that offer introductory 0% APR periods for 12 to 18 months. These lines are typically unsecured and tied to your business entity, meaning they don't appear on your personal credit report. It's a powerful way to access working capital for growth or equipment without the immediate burden of interest costs, provided you have the profile depth to qualify.