Acquiring a Business with No Money Down: The 2026 Strategic Guide

In 2026, the most successful acquisitions aren't funded by personal savings accounts, but by the strategic alignment of existing business assets and professional credit structures. You might feel that a lack of personal liquidity or a fluctuating credit score is an insurmountable wall standing between you and your goals. It's a common concern that entering a high-stakes deal without a massive cash reserve is a recipe for financial ruin. However, acquiring a business with no money down is actually a matter of technical deal architecture rather than personal wealth. We understand the pressure of wanting to scale without risking your family's future, and we've seen how the right framework turns that anxiety into a calculated growth strategy.

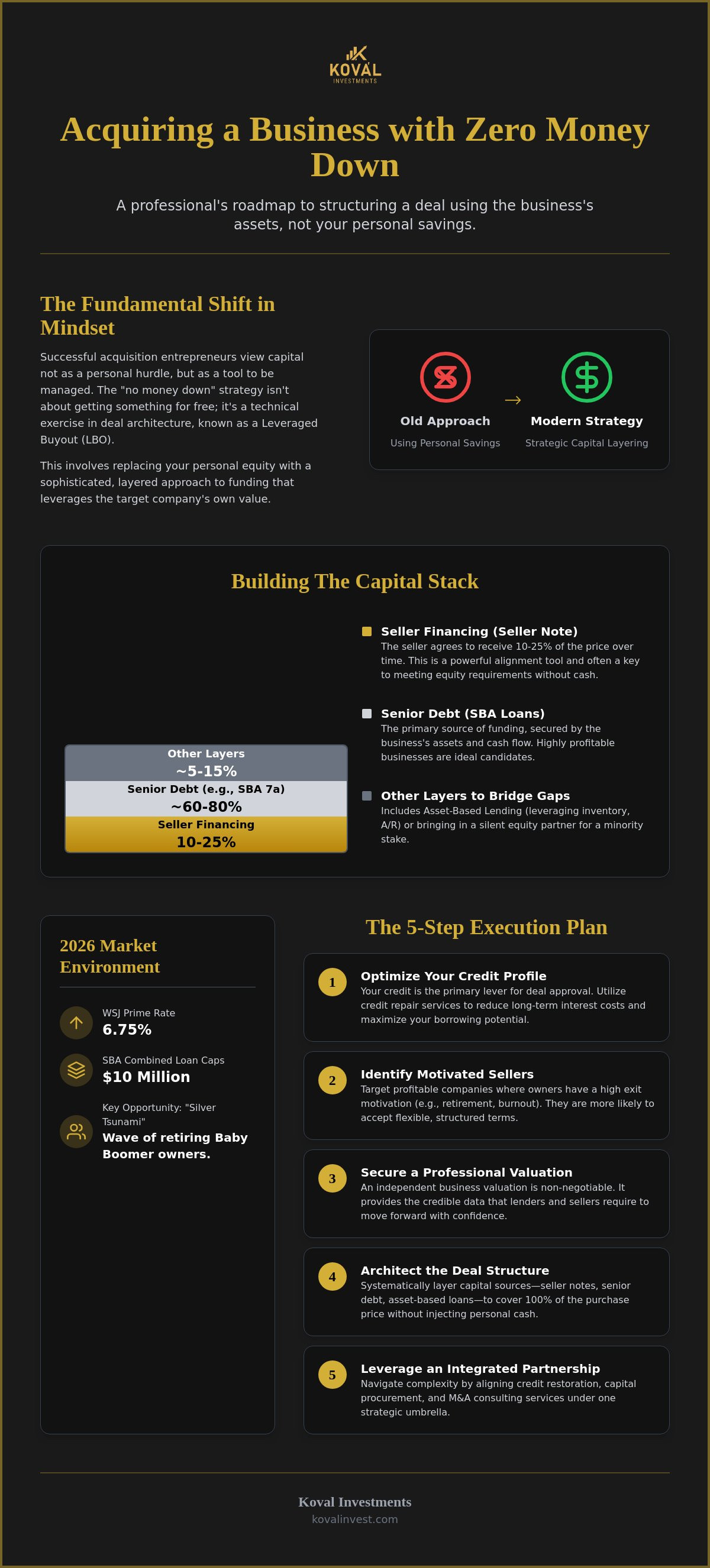

This guide provides a professional roadmap to securing a profitable enterprise using sophisticated financing layers. You'll discover how to navigate the current lending environment, where the Wall Street Journal Prime Rate sits at 6.75% and SBA combined loan caps have recently increased to $10 million. We'll break down how to utilize 0% interest funding solutions, seller financing, and credit repair services to build a capital stack that requires zero personal equity. By the end of this article, you'll understand the specific debt structures and partnership strategies needed to transition from an aspiring owner to a confident CEO.

Key Takeaways

- Redefine your approach by viewing acquiring a business with no money down as a strategic exercise in capital layering rather than a search for a free asset.

- Master the use of seller financing and SBA 7(a) loan structures to meet equity requirements while keeping your personal cash reserves intact.

- Recognize your credit profile as the primary lever for deal approval and learn how credit repair services can significantly reduce your long-term interest costs.

- Build a disciplined execution plan that prioritizes professional business valuations and targets sellers with high exit motivation, such as those facing retirement or burnout.

- Leverage an integrated partnership that aligns credit restoration, capital procurement, and M&A consulting to navigate the complexities of a successful acquisition.

The Reality of Acquiring a Business with No Money Down in 2026

Successful entrepreneurs don't view capital as a personal hurdle; they view it as a tool to be managed. Acquiring a business with no money down is a professional strategy that replaces personal equity with technical deal structure. In technical terms, this is often executed as a Leveraged Buyout (LBO), where the buyer's personal cash outlay at the closing table is zero. It's a common misconception that 'no money down' means there is no money involved in the transaction. On the contrary, the money is very much there, but it's the business's assets and future cash flows doing the heavy lifting rather than your personal bank account.

The core of this strategy lies in orchestrating what professionals call the 'Capital Stack.' This is a layered approach to funding where different sources of capital, such as seller notes, senior debt, and mezzanine financing, are stacked together to cover 100% of the purchase price. In 2026, this approach has become even more viable due to the 'Silver Tsunami.' We're currently seeing a massive wave of Baby Boomer business owners reaching retirement age. Many of these owners are more concerned with a smooth transition and the preservation of their legacy than they are with receiving a massive upfront cash payment, making them ideal partners for structured acquisitions.

Dispelling the Myths of Zero-Down Deals

You might think that only distressed or failing businesses can be bought without personal capital. That isn't the case. In fact, highly profitable companies with stable, predictable cash flows are often the best candidates because their performance provides the security lenders need. It's also vital to distinguish between a 'no-money-down' deal and a 'no-collateral' deal. While you aren't bringing your own cash, the business's inventory, real estate, or accounts receivable often serve as the collateral. Ultimately, seller motivation is the engine of these deals. A founder facing burnout or health concerns is often willing to accept flexible terms to ensure their employees are taken care of and the business continues to thrive.

Why 2026 is the Year of the Acquisition Entrepreneur

Current market shifts have created a unique opening for individual buyers. While large institutional firms are often bogged down by the complexities of massive portfolios, agile buyers can leverage alternative business funding solutions to move faster than traditional banks allow. These specialized funding vehicles prioritize the target business's operational health over the buyer's personal liquidity. Acquisition Entrepreneurship is the fastest path to wealth in the current economy because it allows you to skip the high-risk startup phase and step directly into a profitable, cash-flowing operation.

Core Financing Structures for Zero-Down Acquisitions

Structuring a successful acquisition requires more than just finding a lender; it requires layering disparate capital sources into a cohesive whole. Achieving the goal of acquiring a business with no money down involves moving beyond a single loan and toward a multi-faceted financial architecture. By combining various SBA financing options with private capital and seller participation, you can bridge the gap between the purchase price and your available liquidity. Asset-based lending also plays a pivotal role. This allows you to leverage the target company's accounts receivable, inventory, and equipment to generate immediate working capital or to secure a portion of the acquisition debt. If a gap still remains, bringing in a silent equity partner for a minority stake can provide the final piece of the puzzle without requiring you to touch your personal savings.

Mastering the Seller Note

The seller note is often the most flexible component of your capital stack. In a typical 'Seller Carry' arrangement, the owner agrees to receive 10% to 25% of the purchase price over several years. This isn't just a way to defer payment; it's a powerful alignment tool. You can structure part of this note as an 'earnout,' where payments are contingent on the business meeting specific performance milestones. This protects you from overpaying for projected growth that doesn't materialize. For the seller, this is often a tax-advantaged exit strategy. It allows them to treat the sale as an installment sale, potentially spreading their capital gains tax liability over several years rather than facing a massive bill at closing. If you're unsure how to present these options, our team can provide the strategic planning necessary to frame a win-win proposal.

The SBA 7(a) Strategy for 2026

The SBA 7(a) program remains the gold standard for acquisition financing, especially with the updated 2026 guidelines. As of July 4, 2026, borrowers can now hold up to $10 million in total SBA-backed financing, a significant increase that allows for larger, more profitable acquisitions. The key to a zero-down deal is the 10% equity injection requirement. In many cases, a seller note that is placed on full standby for at least 24 months can be used to satisfy a portion of this requirement. However, lenders will scrutinize your Debt Service Coverage Ratio (DSCR). They generally require a ratio of 1.25x or higher to ensure the business's cash flow can comfortably cover all debt payments plus your salary. Leveraging SBA loan assistance is essential here, as it helps you navigate the complex underwriting process and ensures your financial projections meet these rigorous standards.

The Credit Optimization Unlock: Preparing for Maximum Leverage

Your personal credit profile acts as the ultimate gatekeeper for 100% financed acquisitions. While previous sections detailed how to layer debt, those layers only hold together if the borrower's creditworthiness meets institutional standards. Acquiring a business with no money down requires a credit profile that speaks louder than your current personal liquidity. Lenders view your score as a proxy for operational discipline; a high score suggests you'll manage their capital with the same rigor you apply to your personal obligations. To reach an 'M&A-ready' status, you need a profile characterized by high limits, low utilization, and a clean history that supports both SBA requirements and unsecured funding limits.

At Koval Investments, we operate on a success-based philosophy. We understand that your success is our success, so we focus on building a borrower profile that lenders can't ignore. This collaborative approach ensures that we aren't just looking for a loan, but are instead preparing you to lead a profitable enterprise with the strongest financial foundation possible. By aligning your credit profile with the specific needs of acquisition lenders, we remove the friction that typically stalls zero-down deals.

Why Credit Repair is a Mandatory First Step

Lenders price risk based on your score, which means credit health directly dictates your profit margins. The math is simple but impactful: a 50-point score increase can save hundreds of thousands in interest over a 10-year term. Beyond the interest rate, utilizing professional business credit repair services builds a level of trust with underwriters that is difficult to achieve otherwise. It demonstrates a proactive approach to financial management and ensures that minor errors don't prevent you from accessing millions in capital. Credit optimization is a strategic investment in your long-term deal-making power rather than a temporary fix for past mistakes.

Accessing 0% Interest Funding for Operating Capital

Securing the business is only the first half of the battle; you also need liquidity to manage the transition. We often utilize 0% interest business funding to provide buyers with immediate operating capital on day one. These unsecured lines of credit are accessible to those with an optimized credit profile and can be used to fund the 'soft costs' of an acquisition, such as legal fees and accounting audits. By using 0% APR periods strategically, you can cover these essential expenses without dipping into the business's cash flow during the critical first few months of ownership. This creates a safety net that protects both your personal finances and the stability of your new acquisition.

Structuring the Deal: A Step-by-Step Execution Plan

Acquiring a business with no money down requires a disciplined approach to the deal funnel. You aren't just looking for any profitable company; you're looking for a specific set of circumstances where the owner's goals align with a structured payout. This process moves from identifying the right target to securing the liquidity needed to keep the doors open after the keys are handed over. We follow a methodical progression to ensure every deal is both viable and sustainable.

- Step 1: Identify High-Intent Sellers. Focus on owners motivated by retirement, burnout, or health concerns. These 'Silver Tsunami' sellers often prioritize a reliable successor over a single lump-sum payment.

- Step 2: Perform a Professional Business Valuation. You must ensure the purchase price is supported by historical cash flow. Overpaying is the most common reason leveraged deals fail.

- Step 3: Draft a Detailed Letter of Intent (LOI). Your LOI should clearly specify the financing split. A common 2026 structure involves an 80% SBA loan paired with a 20% seller note.

- Step 4: Secure Post-Closing Liquidity. It's essential to arrange working capital for business acquisition early in the process. This ensures you have the cash flow to manage operations from day one without straining the business's existing reserves.

Strategic Business Valuation

Understanding the difference between Seller’s Discretionary Earnings (SDE) and EBITDA is vital for small to mid-market deals. SDE includes the owner's salary and benefits, which is the standard metric for businesses with less than $1 million in earnings. EBITDA is more common as you scale. A professional valuation prevents you from overpaying by grounding the price in tangible performance data. Our M&A consultants act as a bridge during this phase, negotiating the gap between a seller's emotional attachment and the buyer's requirement for a realistic return on investment. If you're ready to evaluate a potential target, you can get a professional business valuation to ensure your offer is based on facts rather than assumptions.

Mitigating Risk in Leveraged Buyouts (LBOs)

The 'Golden Rule' of a zero-down acquisition is that the business must be able to pay for itself and your salary simultaneously. This means the cash flow must comfortably exceed the debt service requirements. To protect your interests, we often structure 'standby' periods on seller notes. This allows you to defer payments to the seller for the first 24 months, preserving cash flow during the critical transition phase. We also utilize 'clawback' provisions in the purchase agreement. These provisions allow you to adjust the final purchase price if undisclosed liabilities or financial discrepancies are discovered after the closing date, ensuring you don't inherit the previous owner's mistakes.

Navigating Your Acquisition with Koval Investments

The transition from an aspiring entrepreneur to a business owner requires more than just a list of potential targets. It requires a partner who understands how to bridge the gap between your current financial position and the capital requirements of a high-value acquisition. At Koval Investments, we specialize in the technical orchestration of these deals. We don't just provide a single service; we provide an integrated ecosystem that combines Credit Restoration, Capital Procurement, and M&A Consulting into a singular, results-oriented path. This holistic approach is why acquiring a business with no money down becomes a repeatable process rather than a one-time stroke of luck.

Our success-based philosophy ensures that our objectives remain perfectly aligned with yours. We aren't interested in high-volume, transactional relationships that offer little long-term value. Instead, we prioritize the quality of the engagement and the ultimate success of the closing. This partnership model means we're equally invested in the outcome, providing a steady, reliable hand through the complexities of the financial landscape. We act as an extension of your team, navigating the nuances of debt structures so you can focus on the operational future of your new enterprise.

The Koval Advantage: Beyond Just Funding

The value of a seasoned strategic partner lies in the ability to vet deal structures before they reach the closing table. We provide the 'straight-talk' advisory necessary to determine if a business's cash flow can truly support the leverage you plan to use. If a target business includes property assets, we can facilitate access to specialized real estate investment funding to further strengthen your capital stack and optimize your interest rates. This level of insider knowledge helps you avoid common pitfalls and ensures that the business you buy is a platform for growth rather than a financial burden. We believe in transparency and ease of understanding, moving at a pace that allows for thorough comprehension of every strategic move.

Your Path to Ownership Starts with a Strategy

Many entrepreneurs fail because they spend all their energy searching for 'deals' without first building a 'profile' that lenders trust. Acquiring a business with no money down is only possible when your financial foundation is prepared for maximum leverage. We encourage you to stop searching for the perfect business and start building the perfect strategy. Our collaborative approach is designed to be a win-win venture, framing our services as a shared investment in your future success. When you're ready to move from ambition to execution, we're here to provide the steady guidance and technical expertise required to cross the finish line.

Schedule your strategic funding consultation with Koval Investments today to assess your acquisition readiness and begin building your roadmap to ownership.

Executing Your 2026 Acquisition Strategy

Transitioning into business ownership requires a fundamental shift in perspective. We've seen that acquiring a business with no money down is not a matter of luck; it's the result of combining professional credit optimization with sophisticated debt layering. By utilizing seller financing and modern SBA structures, you can preserve your personal liquidity while stepping directly into a cash-flowing enterprise. The current market, driven by a wave of retiring owners, offers a unique window for those ready to act as acquisition entrepreneurs.

At Koval Investments, we provide the steady hand you need to navigate these complex financial waters. Our success-based philosophy ensures that our goals are perfectly aligned with your closing. With our expert M&A and SBA loan consultants by your side, you gain access to comprehensive credit optimization strategies designed to unlock maximum leverage. We don't just help you find funding. We architect the entire capital stack to ensure your new business thrives from day one. Secure the Capital You Need for Your Next Acquisition and take the first step toward building your legacy. Your future as a CEO is closer than you think.

Frequently Asked Questions

Is it actually possible to buy a business with no money down in 2026?

Yes, it's entirely possible through a strategy called capital layering. This involves combining different funding sources, such as SBA loans and seller notes, to cover the full purchase price. By acquiring a business with no money down, you're leveraging the target company's assets and future cash flow rather than your personal savings. This approach is increasingly common as the "Silver Tsunami" of retiring owners creates a market full of sellers open to flexible terms.

What is the minimum credit score required for a business acquisition loan?

Most institutional lenders and SBA providers look for a personal credit score of at least 680 to 700. While a score in this range is often the baseline for approval, higher scores typically unlock more favorable interest rates and higher loan ceilings. If your score is currently below this threshold, professional credit repair services can help you reach the necessary level to qualify for maximum leverage in a zero-down deal.

How do I find sellers who are willing to offer seller financing?

You can find these opportunities by targeting owners who are motivated by factors beyond a quick cash exit, such as retirement or burnout. In many mid-market transactions, seller financing is a standard component that covers 10% to 25% of the deal. The key is to present the offer as a win-win scenario, highlighting the tax advantages and the steady interest income the seller will receive over time.

Can I use an SBA loan for a 100% financed business purchase?

You can achieve 100% financing by pairing an SBA 7(a) loan with a seller standby note. While the SBA generally requires a 10% equity injection, they allow a portion of this to come from a seller note that is on "full standby" for at least 24 months. This structure satisfies the lender's equity requirements while allowing you to complete the transaction without putting your own capital on the line.

What happens if the business I buy fails and I have no money down?

If the business fails, you remain legally responsible for the debt used to acquire it. Most acquisition loans, including SBA-backed options, require a personal guarantee, which means your personal assets could be at risk if the business cannot meet its obligations. This is why professional due diligence and a rigorous business valuation are essential steps to ensure the company's cash flow is stable and sustainable.

How much does a professional business valuation cost for an acquisition?

The cost of a professional valuation depends on the size of the business and the complexity of its financial records. These assessments are a mandatory part of the M&A process and are used by lenders to ensure the purchase price is justified by the company's earnings. While we don't quote specific fees, a valuation is a critical investment that protects you from overpaying for a leveraged asset.

Do I need to have experience in the industry of the business I am buying?

Lenders prefer to see direct industry experience, but it isn't always a strict requirement if you have strong transferable skills. If you're entering a new field, you can strengthen your profile by demonstrating a history of successful management or by keeping the existing management team in place. Showing that the business can operate smoothly under your leadership is vital for securing high-leverage financing.

How long does the process of acquiring a business with no money down typically take?

The entire process typically takes between 90 and 180 days from the initial search to the final closing. This timeline includes approximately 30 to 60 days to identify a target and sign a Letter of Intent, followed by 60 to 90 days for deep due diligence and bank underwriting. Having a strategic partner can often streamline these stages by ensuring your credit and capital structures are prepared in advance.