Bad Credit Business Financing with No Collateral: A Strategic Guide for 2026

What if the rejection letter from your bank wasn't the end of your expansion plans, but actually the first step toward a more sophisticated capital strategy? Many entrepreneurs assume that bad credit business financing no collateral is either a myth or a debt trap, leaving them to feel like growth is held hostage by a FICO score. It's frustrating when your company's actual revenue and future potential are ignored because you lack a deed to commercial property or a perfect credit history. We understand that high-interest rate anxiety can make the search for capital feel like an exhausting hunt for a partner who truly understands your trajectory.

This guide demonstrates how to secure unsecured capital even with a challenged history while building a bridge toward the 0% interest funding solutions that high-tier enterprises use to scale. You'll discover how to leverage your current cash flow for immediate operations and follow a strategic path to significantly better terms. We'll explore the 2026 lending environment, compare high-speed revenue-based options, and outline a clear method for restoring your credit profile to unlock institutional-grade capital and long-term stability.

Key Takeaways

- Learn why modern lenders in 2026 prioritize your business revenue and cash flow over traditional physical assets, allowing for faster expansion without pledging collateral.

- Evaluate the true cost of capital by comparing immediate funding expenses against the high cost of inaction and missed market opportunities.

- Identify which bad credit business financing no collateral options, such as MCAs or unsecured lines of credit, best suit your current operational needs.

- Master the strategic steps to audit your credit profile and craft a compelling capital narrative that addresses past challenges while highlighting future potential.

- Discover the roadmap to graduate from high-interest bridge loans to 0% interest funding solutions through targeted credit optimization and professional advisory.

Understanding Bad Credit Business Financing with No Collateral in 2026

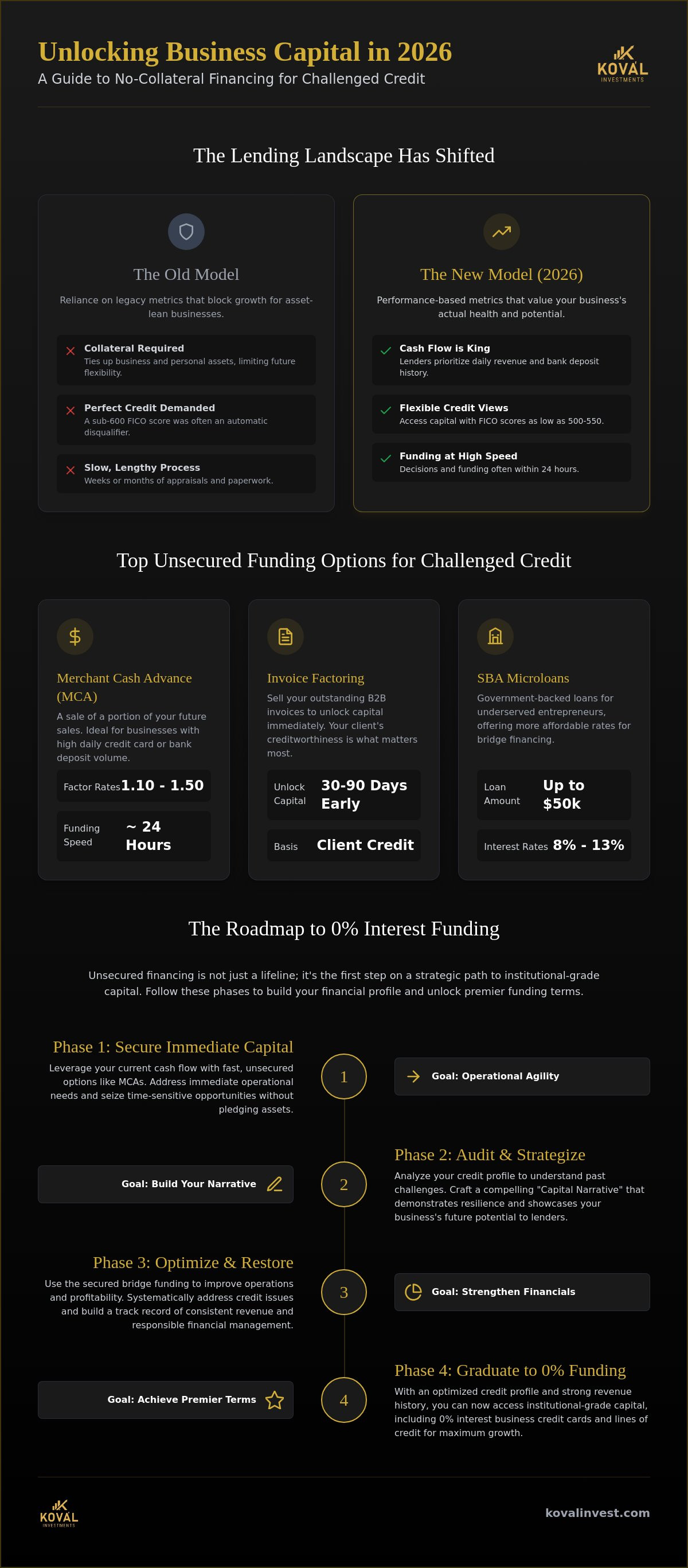

Traditional banking often feels like a relic. For years, the standard approach to business lending required a perfect credit score and a stack of property deeds. In 2026, the landscape has shifted toward performance-based metrics. Bad credit business financing no collateral is a model where lenders prioritize your company's daily revenue and operational character over physical assets. Instead of asking what you own, modern lenders ask how your business performs. This shift allows entrepreneurs with FICO scores as low as 500 to 550 to access the capital they need to scale without the burden of asset pledges.

The no-collateral model is currently the fastest-growing segment for small and medium businesses. This growth is driven by a fundamental change in how risk is calculated. With the WSJ Prime Rate sitting at 6.75% and the 30-Day SOFR at 3.68% as of July 2026, the cost of traditional debt remains a significant consideration. However, the real barrier for many isn't just the interest rate, but the lack of real estate or equipment to secure a loan. By focusing on bank deposit history and monthly revenue, lenders provide a lifeline to businesses that are rich in cash flow but lean on tangible assets.

Procuring strategic capital requires a psychological shift. It's no longer about simply "getting a loan" to survive; it's about using specific financial tools to accelerate growth. Many owners believe a sub-600 credit score is an absolute wall. That's a myth. In the current economy, your "Capital Narrative"—the story of why your credit was challenged and how you've built a resilient revenue stream—carries more weight than a three-digit number from a bureau.

Unsecured vs. Secured Financing: A Strategic Comparison

Secured financing relies on collateral to mitigate lender risk, but the hidden cost is the restriction it places on your future. Tying up your assets can prevent you from securing additional funding later if a major opportunity arises. Unsecured funding is a credit-based commitment without asset pledges. While unsecured business financing may carry higher initial rates, it protects your long-term flexibility. Lenders view these applications by analyzing your business's ability to generate future receivables, making it a "win-win" for companies with strong sales but challenged credit profiles.

Why Business Owners Choose No-Collateral Options

Speed is the primary differentiator. Because there are no lengthy appraisals or title searches required, bad credit business financing no collateral can often be finalized in as little as 24 hours. This agility is vital for capturing time-sensitive inventory discounts or launching marketing campaigns. Furthermore, these options preserve your personal assets. Keeping your home and vehicles separate from business liabilities ensures that your family's security isn't tied to the unpredictable cycles of commerce. It's a pragmatic approach that aligns your funding with the day-to-day realities of operational growth.

Top Unsecured Funding Options for Challenged Credit Profiles

Identifying the right vehicle for capital is a matter of matching your business's specific needs with the available market tools. For many founders, bad credit business financing no collateral is best achieved through a Merchant Cash Advance (MCA). This isn't a traditional loan; it's a sale of a portion of your future credit card sales or bank deposits. Because the provider is purchasing future receivables, they prioritize your daily sales volume over your personal FICO score. Factor rates for these advances typically range from 1.10 to 1.50, and funding can often reach your account within 24 hours.

Invoice factoring provides another strategic path for B2B companies. By selling your outstanding accounts receivable to a third party, you can unlock liquid capital that would otherwise be trapped for 30, 60, or 90 days. This method relies on the creditworthiness of your clients rather than your own. While many founders assume federal assistance is out of reach, SBA-backed loans through the microloan program offer up to $50,000 for underserved entrepreneurs. These loans often feature interest rates between 8% and 13%, making them a significantly more affordable bridge than high-interest alternative debt.

Revenue-Based Financing: The Modern Alternative

Revenue-based financing is gaining momentum because it aligns the lender's success directly with yours. Instead of a fixed monthly payment that might strain your cash flow during a slow week, repayments are calculated as a percentage of your gross revenue. If your sales dip, your payment decreases. This flexibility makes it an ideal choice for businesses with monthly revenues of $10,000 to $15,000 that need capital for marketing or inventory but don't want the rigid pressure of a term loan. It's a pragmatic solution for those seeking bad credit business financing no collateral without the fear of default during seasonal lulls.

Unsecured Lines of Credit for Growth

An unsecured line of credit functions as a financial safety net. You only pay interest on the funds you actually draw, which provides immense flexibility for managing unexpected operational costs. Having an open line of credit is particularly advantageous when using working capital for business acquisition, as it allows you to move quickly on a competitor's assets or a sudden expansion opportunity. By maintaining consistent, on-time repayments, you can often negotiate for higher credit limits over time. A steady hand like Koval Investments can help you determine which of these vehicles aligns with your long-term valuation goals.

Evaluating the ROI: When Does Bad Credit Financing Make Sense?

Many entrepreneurs hesitate to pursue bad credit business financing no collateral because they focus solely on the interest rate. This is often a narrow view that ignores the "Cost of Inaction." If waiting six months to improve your credit score means losing a prime contract or a significant inventory discount, the interest you "saved" is actually a loss in potential revenue. The true expense of capital should always be measured against the growth it enables. When you use capital as a tool rather than a crutch, a higher-cost bridge loan becomes a strategic investment in your company's future valuation.

We advocate for a "Win-Win" philosophy where initial funding acts as a catalyst. By using this capital to hit specific operational milestones, you demonstrate a track record of performance that traditional banks can't ignore. This performance, paired with a commitment to credit optimization, creates a clear path to trigger better future rates. It's a methodical progression: you take the capital available today to build the credit profile required for 0% interest solutions tomorrow. It's about moving from survival to strategic procurement.

Avoiding debt traps requires a steady hand and a sharp eye for predatory terms. Before signing any agreement, you must identify red flags like hidden fees or aggressive daily repayment structures that don't align with your cash flow. Transparency is the foundation of a healthy financial partnership. A reliable advisor helps you navigate these complexities, ensuring that the capital you secure supports your trajectory rather than hindering it.

Calculating Your Strategic Return

ROI in the context of unsecured funding is the net profit generated minus the total cost of capital. Consider a practical scenario. If you utilize a 15% interest loan to secure a bulk inventory discount of 30%, the $15,000 cost on a $100,000 draw is immediately offset by $30,000 in savings. You've effectively generated a 15% net gain before making a single sale. Projecting revenue increases from marketing spend follows the same logic. If a $20,000 campaign funded by unsecured capital is projected to generate $60,000 in new contracts, the cost of that capital is a minor fraction of the total return.

Mitigating Risk in Unsecured Lending

Don't let the math confuse you; understanding the difference between factor rates and APR is essential. A factor rate of 1.25 means you pay back $1.25 for every $1 borrowed, which is a fixed cost regardless of how fast you pay it back. This is different from an annual percentage rate that compounds over time. Identifying alternative business funding solutions that offer no prepayment penalties and transparent schedules provides a safer cushion for scaling. We focus on these success-based outcomes, ensuring that your funding strategy remains as agile as your operations.

Strategic Steps to Qualify and Optimize Your Financial Profile

Securing bad credit business financing no collateral is a tactical maneuver, not a desperate one. Most competitors treat a low FICO score as a permanent brand, but we view it as a temporary state that can be managed through precise action. The first step is a thorough audit of your business and personal credit reports. Inaccuracies are frequent. Removing these errors can provide an immediate lift to your standing and change how lenders perceive your risk profile.

You also need to prepare a Capital Narrative. This document explains the context of your credit history while detailing your future growth plan. Lenders in 2026 are increasingly looking for founders who can demonstrate a clear ability to pay through optimized cash flow. By showing consistent bank deposits and a healthy debt-to-income ratio, you prove that your business is a steady hand despite past personal credit challenges. Utilizing professional business credit repair services is often the most efficient way to remove these barriers and accelerate your access to capital.

The Role of Credit Restoration in Capital Procurement

Credit restoration is the bridge between high-interest bridge loans and institutional-grade capital. Disputing errors is the fastest way to jump a credit tier. A 50-point increase in your score doesn't just look better; it can save you thousands in interest over the life of your financing. This preparation is especially vital when positioning your profile for SBA loan assistance. By fixing historical issues now, you ensure that you meet the stringent requirements for federal programs that offer the most competitive terms in the market.

Demonstrating Business Health Beyond the Score

Your bank statements often tell a more compelling story than your credit report. Lenders prioritize businesses with consistent daily or weekly deposits, as this indicates a reliable revenue stream. A professional business valuation can also give lenders confidence in your unsecured request by highlighting the underlying worth of your operations. If you're ready to start this optimization process, a consultation with Koval Investments can help you identify the specific levers to pull for your unique situation. Use this checklist to prepare for your no-collateral application:

- Six months of business bank statements showing consistent activity

- Most recent tax return and a current year-to-date P&L statement

- Your prepared Capital Narrative explaining growth milestones

- Proof of minimum monthly revenue (typically $10,000 to $15,000)

The Koval Advantage: Moving Toward 0% Interest Funding

While the market for bad credit business financing no collateral offers immediate relief, we believe entrepreneurs deserve a destination beyond high-interest debt. Most lenders are content to keep you in a cycle of high-cost renewals. At Koval Investments, we operate as a strategic partner rather than a transactional service provider. Our focus is on a success-based outcome where we align our expertise with your long-term growth. This means we don't just help you secure a bridge loan; we architect the path to graduate you into institutional-grade capital.

The core of our approach is the integration of credit repair services with aggressive capital procurement. By cleaning up your profile as you utilize initial working capital, we prepare your business for our 0% interest business funding solution. This transition is the ultimate win-win. You get the cash flow you need today to maintain operations, while we work alongside you to unlock interest-free capital that can be used for significant scaling or debt consolidation. It's a methodical shift from paying for access to capital to using capital that pays for itself.

Our 0% Interest Funding Solution

We specialize in accessing interest-free capital for periods up to 18 months. This isn't a traditional bank loan but a sophisticated credit-based strategy that leverages your restored financial profile. For example, consider a founder whose challenged credit initially limited them to high-factor MCAs. By implementing a targeted credit restoration plan, we can help a business jump two credit tiers in a matter of months. In one instance, a client with a history of defaults was restored to qualify for $150,000 at 0% interest. They used these funds to retire their high-interest debt, which immediately improved their net margins and overall business valuation.

Your Long-Term Strategic Partner

Our relationship doesn't end when the funds hit your account. We provide comprehensive support, including business valuations and mergers and acquisitions consulting, to ensure you're building a sellable asset. Strategic planning is a continuous process. As the 2026 financial landscape evolves, having a steady hand to navigate shifting interest rates and lending regulations is a major competitive advantage. We invite you to experience this collaborative approach by engaging in a professional consultation today. There is no financial risk to explore how our success-based philosophy can transform your capital strategy from a burden into a competitive edge.

Architecting Your Financial Future Beyond 2026

Securing capital in a complex economy requires more than just a loan application; it demands a comprehensive strategy. We've explored how bad credit business financing no collateral serves as a vital bridge for immediate operations while you work to optimize your long-term profile. By prioritizing your business's revenue performance over static credit scores, you can unlock the liquidity needed to scale without risking your personal assets. The shift from high-interest debt to 0% interest solutions isn't just possible; it's a methodical process of restoration and procurement.

Since 2018, we've acted as a steady hand for entrepreneurs navigating these financial landscapes. Our success-based philosophy ensures that our interests remain perfectly aligned with your growth. We specialize in 0% interest funding solutions and expert strategic advisory designed to move you from survival to significant valuation increases. If you're ready to stop reacting to credit challenges and start proactively building your capital narrative, we invite you to take the next step.

Secure Your Strategic Funding Consultation with Koval Investments and discover the win-win potential of a partnership focused on your long-term success. Your business's future isn't defined by your past credit history, but by the strategic choices you make today.

Frequently Asked Questions

Can I get a business loan with a 500 credit score and no collateral?

Yes, you can secure funding with a 500 credit score through alternative lenders who prioritize revenue over personal FICO scores. These providers typically look for a minimum of $10,000 to $15,000 in monthly revenue to offset the perceived risk. While traditional banks will likely decline this profile, revenue-based financing or Merchant Cash Advances provide a viable path for immediate capital without the need to pledge physical assets like real estate.

What is the fastest way to get unsecured business funding in 2026?

Merchant Cash Advances and revenue-based financing are the fastest options, often providing capital in as little as 24 hours. Because these methods don't require property appraisals or complex collateral valuations, the underwriting process is significantly more efficient than traditional bank loans. Most digital-first lenders in 2026 utilize automated bank verification and real-time cash flow analysis to speed up approvals for businesses needing quick operational capital to capture growth opportunities.

Do unsecured business loans require a personal guarantee?

Yes, most unsecured business loans for founders with challenged credit require a personal guarantee even when no physical collateral is pledged. This legal agreement means you remain personally responsible for the debt if the business cannot fulfill its obligations. It's a standard risk-mitigation tool used by lenders to offer bad credit business financing no collateral without the security of property. This ensures the lender has some recourse while allowing you to keep your assets separate.

How does credit repair help me get better business loan rates?

Credit repair improves your rates by moving you into higher lending tiers where risk-based pricing is more favorable. Even a modest 50-point increase can shift your profile from a high-cost alternative lender to a more affordable institutional provider. Removing inaccuracies and optimizing your credit utilization creates the leverage needed to negotiate for traditional terms. This optimization is a key part of graduating from high-interest bridge loans toward our strategic 0% interest funding solutions.

What are the typical interest rates for bad credit business financing?

Interest rates vary widely based on the specific vehicle, with SBA Microloans generally ranging from 8% to 13% in 2026. Alternative term loans for bad credit often carry APRs between 15% and 35%. Merchant Cash Advances utilize factor rates rather than standard interest, which can result in effective APRs of 40% to 150% depending on your repayment speed. Understanding these costs is essential for calculating the return on investment for your strategic capital.

Is an SBA loan possible with bad credit and no assets?

An SBA loan is possible through the Microloan program, which provides up to $50,000 without the heavy collateral requirements of standard 7(a) loans. While the SBA generally prefers some form of security, they allow for flexibility with smaller amounts for underserved founders. Success in this area often depends on a strong Capital Narrative and a clear plan for using the funds to generate revenue. Credit restoration is also a vital step in meeting SBA eligibility.

What is the difference between a factor rate and an interest rate?

A factor rate is a fixed multiplier applied to the total loan amount, whereas an interest rate is an annual percentage that compounds on the remaining balance. For example, a 1.20 factor rate on $10,000 means you pay back exactly $12,000 regardless of how quickly you repay. Interest rates allow for savings if you pay early, but factor rates provide a predictable, fixed cost of capital that is common in the alternative lending space.

How much funding can I get without collateral?

You can typically secure between $2,500 and $1,000,000 without collateral, depending on your business's monthly revenue and cash flow history. Most alternative lenders will offer a funding amount equal to 10% to 15% of your annual gross sales. For higher limits, such as the $500,000 available through SBA Express loans, lenders will look for strong operational performance and consistent bank deposits. Your ability to demonstrate a healthy debt-to-income ratio also influences these limits.