Financing Business Expansion: The Strategic Guide to Scaling in 2026

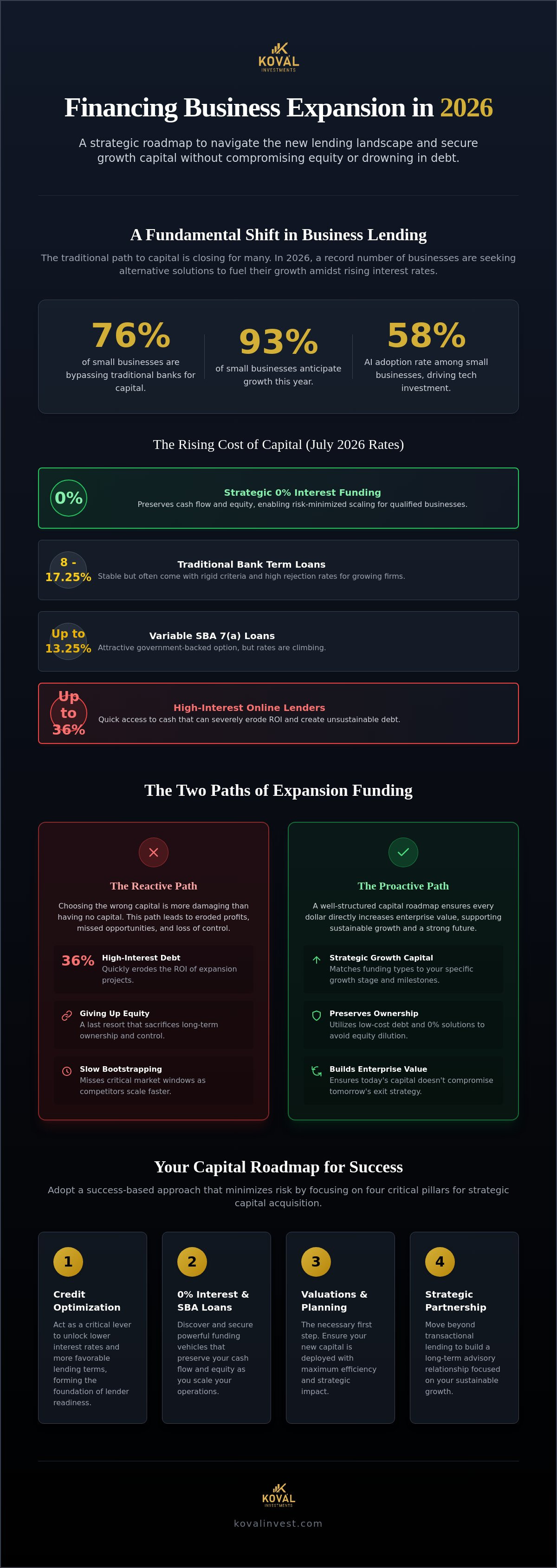

Over 76% of small businesses are bypassing traditional banks for capital in 2026, a record high that reflects a fundamental shift in the lending landscape. You've likely felt the pressure of this transition, especially with variable SBA 7(a) rates climbing as high as 13.25% this July. It is exhausting to see your growth potential limited by high interest rates or the fear that a less than perfect credit profile will lead to an immediate rejection. You want to scale, but you don't want to hand over your hard earned equity or drown in debt service just to reach the next level.

This guide provides a clear path forward for financing business expansion by focusing on strategic capital acquisition and financial optimization. We'll show you how to access 0% interest funding solutions and low-APR capital that traditional lenders often keep behind a veil of complexity. By the end of this article, you'll have a practical roadmap for lender readiness and a strategy to build a long term financial partnership that prioritizes your success without the typical risks. We are moving past the confusion of SBA requirements and toward a model where your business scales on your own terms.

Key Takeaways

- Understand why a proactive capital strategy is essential for growth and how to navigate the shifting interest rate landscape of 2026.

- Learn how credit optimization acts as a critical lever for financing business expansion, helping you unlock lower rates and more favorable lending terms.

- Discover the mechanics of 0% interest funding solutions and SBA loans that preserve your cash flow and equity as you scale operations.

- Identify why professional business valuations and strategic planning are the necessary first steps to ensure your new capital is deployed with maximum efficiency.

- Adopt a success-based approach to capital procurement that minimizes financial risk while building a long-term partnership with strategic advisors.

Financing Business Expansion: Why Capital Strategy is Your Growth Engine

Financing business expansion is the strategic procurement of capital intended to broaden your market reach and strengthen your competitive position. It's the fuel that transforms a stable operation into a market leader. In the fast moving environment of 2026, standing still is a significant risk. With nearly 93% of small businesses anticipating growth this year according to a May report, those who hesitate to secure capital often find their market share captured by more agile competitors. Success depends on distinguishing between expensive debt and Growth capital that aligns with your specific operational milestones.

A well structured plan involves more than just looking at your bank balance. Think of your funding strategy as a Capital Roadmap. This plan ensures that every dollar you borrow or raise directly increases your enterprise value. Instead of reacting to cash flow gaps, you're proactively matching funding types to your growth stage. This methodical approach is what separates a sustainable scale up from a business struggling under the weight of misaligned debt. By aligning your financing business expansion efforts with long term business valuations, you ensure that the capital you bring in today doesn't compromise your exit strategy tomorrow.

The Core Objectives of Strategic Expansion

Scaling requires a clear focus on where your capital will have the most impact. Geographic expansion and market penetration are common goals, but they demand different financial structures. Vertical integration usually requires significant liquid capital to acquire suppliers or distributors, giving you more control over your supply chain. Horizontal integration focuses on acquiring competitors to increase market density. In 2026, many firms are also prioritizing investments in technology and human capital. With AI adoption reaching 58% among small businesses, financing these tools has become a prerequisite for maintaining operational efficiency and staying relevant in a crowded field.

The Cost of Misaligned Funding

Choosing the wrong type of capital can be more damaging than having no capital at all. High interest debt, which can reach up to 36% through some online lenders as of July 2026, quickly erodes the return on investment of even the most successful expansion. While many founders pride themselves on bootstrapping, doing so for too long can cause you to miss critical market windows. When your competitors are scaling with low cost capital, your self funded growth might be too slow to keep pace. However, giving up equity should remain a last resort. For established founders, the goal is to secure funding that supports growth without sacrificing ownership or control of the firm's future.

Evaluating the Best Financing Options for Business Expansion in 2026

Choosing the right vehicle for financing business expansion requires a clear understanding of the current interest rate environment. In July 2026, traditional bank term loans carry average rates between 8% and 17.25%. While these institutional loans offer a sense of stability, their rigid criteria often lead to high rejection rates for growing firms. This friction has led many founders toward alternative business funding solutions. These options provide the agility needed to seize market opportunities that traditional banks might miss. Working capital plays a vital role here, acting as the essential bridge that prevents your operational expenses from outstripping your revenue during a rapid scaling phase.

The choice between traditional and alternative sources isn't always binary. Many successful expansion strategies utilize a hybrid approach. You might use a long-term bank loan for real estate while relying on flexible alternative capital for inventory or short-term payroll spikes. The goal is to build a capital structure that supports your momentum without creating a bottleneck. By diversifying your funding sources, you protect your business from the volatility of any single lending sector.

SBA Loans: The Gold Standard for Scalable Debt

SBA loans remain one of the most attractive paths for founders looking to minimize their cost of capital. When exploring SBA loan programs, it's important to note that the SBA increased the combined exposure cap for 7(a) and 504 loans to $10 million as of July 4, 2026. This change provides significant room for larger scale projects. Deciding between an SBA 7(a) vs. 504 loan depends on your asset needs; the 504 is excellent for fixed assets with rates currently between 6.17% and 6.20%. Because the application process is notoriously rigorous, professional SBA loan assistance is often the difference between a funded project and a stalled application.

Unsecured Working Capital and Lines of Credit

Unsecured funding is a strategic tool for managing "soft costs" such as aggressive marketing campaigns or new executive hires. These expenses don't always provide the collateral traditional lenders demand, making unsecured lines of credit a superior choice. It's also helpful to distinguish between working capital for business acquisition and funding for internal growth. Acquisitions require a heavy upfront injection to ensure a smooth transition, whereas internal growth funding typically supports incremental increases in capacity. If you're unsure which path fits your current trajectory, a strategic planning session can help align your capital procurement with your actual growth milestones.

Many entrepreneurs believe their credit profile is a static obstacle they simply have to accept. This misconception often leads to settling for predatory rates or abandoning growth plans altogether. When you're financing business expansion, your credit score isn't just a number; it's a financial lever. Even minor inaccuracies on a business credit report can trigger automatic rejections from traditional lenders or push you into high-interest alternative products. These errors can cost a business owner thousands of dollars in unnecessary interest over the life of a loan. Founders should distinguish between personal credit repair and business credit profile optimization. While personal repair focuses on removing historical negatives, business optimization involves ensuring your company's data is correctly reported across all major bureaus. This includes verifying that your legal name, address, and industry codes are consistent and accurate. To secure the best terms, many founders now view business credit repair services as a critical pre-funding necessity.The ROI of a Higher Credit Score

A 50-point increase in your score can fundamentally change your financial trajectory. For many, this jump shifts a loan application from the "denied" pile to "prime rate" territory. Credit repair acts as a force multiplier for expansion capital by lowering the hurdle rate for every dollar your business acquires. Beyond interest rates, a healthier profile often unlocks significantly higher funding limits. Lenders are more comfortable extending large Business expansion loans when they see a track record of reliability and a clean financial profile.

Disputing Inaccuracies and Building a Profile

Errors on business credit reports are surprisingly common. Simple mistakes, like an incorrect NAICS code or an outdated lien that was never released, can cause a lender's automated system to flag your business as high risk. You don't want to find these errors while you're in the middle of an application. The optimal timeline for credit optimization is at least 90 days before you intend to apply. This window allows enough time for bureaus to process disputes and update your records. At Koval Investments, we utilize a success-based model to ensure your profile is perfectly aligned with lender requirements before you ever submit an application. This collaborative approach removes the guesswork and positions you as a low-risk, high-value borrower.

Strategic Pathways to Low-Cost Capital: SBA Loans and 0% Interest Solutions

Most founders looking at financing business expansion focus exclusively on debt that carries interest. While SBA loans are excellent, the 0% interest business funding solution represents a superior tool for specific scaling needs. This model utilizes high-limit, interest-free business credit lines that preserve your liquid cash flow during critical growth phases. By accessing capital without the immediate burden of APR, you can deploy funds into areas that generate immediate returns. It's a pragmatic way to scale without the weight of monthly interest payments slowing your momentum.

Qualifying for these interest-free lines requires a methodical approach to profile optimization. Lenders look for specific indicators of stability and creditworthiness that go beyond a simple score. A typical roadmap involves cleaning up your personal and business credit reports, then strategically applying to a sequence of lenders that offer introductory 0% APR periods. These periods often last 12 to 18 months. Compared to traditional SBA loans, which involve interest costs from the first month, 0% funding allows you to reinvest your gross profits directly back into your operations.

Leveraging 0% APR for Rapid ROI Projects

Zero-interest capital is most effective when used for projects with a clear, fast return on investment. This includes bulk inventory purchases, essential equipment upgrades, or aggressive marketing blitzes. It also serves as an excellent "bridge" strategy. If you're currently in the middle of a long SBA approval process, 0% funding provides the immediate liquidity you need to keep moving. Some savvy founders even cycle this capital, moving balances between different interest-free vehicles to avoid interest costs indefinitely throughout their expansion. This approach maximizes your leverage while keeping your overhead at a minimum.

Navigating SBA Requirements with Expert Guidance

While 0% funding is fast, SBA loans remain the anchor for larger, long-term investments. However, the documentation requirements are dense. You'll need clean tax returns, precise P&L statements, and a comprehensive business plan that demonstrates future profitability. Tools like "Lender Match" are often insufficient for complex financing business expansion needs because they don't account for the nuances of your specific industry. A strategic advisor acts as an insider, positioning your firm as low risk to underwriters before you ever submit a file. If you are ready to secure the capital needed to scale, apply for a funding assessment with Koval Investments to review your strategic options.

Executing Your Expansion: From Valuation to Capital Procurement

Successful execution begins with a reality check. Before you commit to financing business expansion, you must understand the current market value of your enterprise. A professional business valuation serves as your baseline. It tells you exactly how much leverage your balance sheet can handle without jeopardizing your operational stability. Without this data, you're essentially guessing your debt capacity, which is a dangerous way to manage a scaling firm. This valuation isn't just a hurdle for lenders; it's a strategic tool that helps you negotiate from a position of strength and clarity.

Strategic planning ensures that your capital is deployed where it will generate the highest return. It is not enough to simply secure the funds; you must have a methodical plan for how that capital will move the needle on your enterprise value. At Koval Investments, we act as a steady hand throughout this entire process. We manage the entire financial stack for our clients, from the credit optimization and 0% interest solutions we've discussed to high-level M&A consulting. Our success-based philosophy means our goals are perfectly aligned with yours. We operate on a win-win model where we only succeed when you secure the results you need, eliminating the financial risk often associated with traditional consulting fees.

Valuation and M&A Consulting

Knowing your current value helps determine how much debt you can safely carry during a growth phase. If you're looking at mergers and acquisitions, this knowledge is even more critical. Expanding through a purchase allows you to acquire market share or proprietary technology instantly, but it requires precise capital deployment. You need to ensure that the cost of financing business expansion doesn't outweigh the synergies gained from the acquisition. We help you prepare for a successful transition or exit as the final stage of your expansion. Even if you aren't planning to sell today, every dollar of capital should be focused on increasing your company's ultimate enterprise value.

Securing Your Capital Partner

Founders often make the mistake of hiring a broker when they actually need a strategic advisor. A broker is focused on a single transaction and a quick commission. An advisor looks at the long-term health of your business and helps you optimize your financial profile for years to come. This ongoing optimization ensures that your firm remains attractive to lenders and investors alike, providing you with a permanent competitive advantage. When you choose a partner who is invested in your outcome, you gain an insider's perspective on the complex landscape of capital procurement. It is about building a relationship that supports your ambitions while respecting your operational constraints. Partner with Koval Investments to secure your expansion funding today.

Secure Your Growth Trajectory with Precision Capital

Scaling a company in 2026 requires more than just a standard bank loan; it demands a sophisticated alignment of your financial profile with the right capital vehicles. You've seen how credit optimization acts as a strategic force multiplier and why 0% interest solutions are essential for protecting your cash flow during aggressive growth phases. Successfully financing business expansion is a methodical process that begins with a clear valuation and ends with a partner who truly understands your long-term objectives. It's about moving from reactive borrowing to proactive capital management that preserves your equity.

At Koval Investments, we provide the steady hand you need to navigate this complex landscape through our success-based consulting model. We specialize in 0% interest funding solutions, comprehensive credit repair, and expert SBA assistance to ensure you scale without unnecessary financial risk. Our goal is to create a win-win partnership where your growth is the primary measure of our success. Access 0% Interest Funding for Your Business Expansion today and take the first step toward a more profitable future. Your vision for the business is achievable, and with the right strategic capital in place, you're ready to lead your market with confidence.

Frequently Asked Questions

How do I qualify for 0% interest business funding for expansion?

Qualifying for interest-free funding requires a strong personal credit profile, typically a score of 680 or higher, and a clean business credit report. Lenders look for specific indicators of stability, such as a consistent address history and correct industry classifications. We help you optimize these data points to meet the internal underwriting standards of institutions offering introductory 0% APR periods, ensuring you access the maximum capital available.

Can I get an SBA loan for business expansion if my credit is less than perfect?

Yes, it's possible to secure an SBA loan with less than perfect credit, but the process requires a more strategic approach to lender selection. While the SBA provides the guarantee, individual banks set their own credit minimums. We focus on credit restoration and profile alignment to move your application into a range that qualifies for prime rates, reducing the financial risk of a potential denial.

What is the difference between working capital and an expansion loan?

Working capital is designed to cover short-term operational costs like payroll or inventory, while an expansion loan typically funds long-term growth projects like real estate or acquisitions. Expansion loans often feature longer repayment terms and lower interest rates to match the slower ROI of major projects. Choosing the correct vehicle is essential for financing business expansion without creating a sudden cash flow bottleneck in your daily operations.

How long does the credit repair process take before I can apply for funding?

Most business owners see significant profile improvements within 90 days, though the exact timeline depends on the number of inaccuracies we need to dispute. It's best to start this process at least three months before you intend to apply for capital. This proactive window gives credit bureaus enough time to verify and update your records, ensuring your profile is lender-ready when you submit your application.

Do I need a professional business valuation before seeking expansion capital?

Yes, a professional business valuation is a critical first step for any founder seeking significant growth capital or considering an acquisition. It provides a concrete baseline for how much debt your company can safely carry and demonstrates your enterprise value to potential lenders. Knowing your exact worth allows you to negotiate loan terms and interest rates from a position of authority rather than guesswork.

What are the most common reasons business expansion loans are denied?

Most denials stem from poor debt-to-income ratios, low credit scores, or simple inconsistencies in business documentation. Automated underwriting systems frequently flag errors like incorrect industry codes or outdated lien filings that haven't been released. We mitigate these risks by performing a thorough pre-funding audit, which aligns your financial profile with current lender requirements before you ever submit a formal file.

Is collateral always required for large-scale business expansion funding?

Collateral isn't always a requirement, especially when utilizing unsecured funding solutions or specialized 0% interest credit lines. While traditional real estate loans usually require asset backing, many alternative capital sources rely on your company's revenue and creditworthiness instead. This flexibility is vital for service-based businesses or firms that don't want to tie up their personal or business assets during a scaling phase.

How can strategic planning reduce the risks of financing a new location?

Strategic planning identifies potential cash flow gaps and ensures your capital procurement matches your actual operational milestones. It helps you avoid the high-interest debt that often erodes the ROI of a new site. By mapping out your expansion, you can align your funding with your long-term valuation goals, ensuring that every dollar spent on financing business expansion contributes directly to your company's enterprise value.