How to Strategically Remove Errors from Your Credit Report in 2026

A single clerical error on your credit report isn't just a minor typo; it's a direct tax on your company's growth potential. You've likely felt the sting of a funding denial because of outdated data or experienced the frustration of an automated rejection from a bureau that refuses to acknowledge your documentation. Understanding the impact of credit repair on business funding is the first step toward reclaiming your leverage, especially when inaccuracies force you into SBA 7(a) fixed rates as high as 14.75% while your competitors access cheaper capital.

You deserve a partner who understands that credit restoration is a strategic maneuver, not just a clerical task. This guide provides the exact steps to identify, dispute, and permanently remove credit report inaccuracies to unlock high-level capital for your operations. We'll preview the 2026 FCRA dispute timelines and provide a methodical framework to clean your profile, helping you qualify for 0% interest funding and the most competitive market rates available today. By following this logical progression, you can move from the frustration of rejection to the confidence of a clean, fundable credit profile.

Key Takeaways

- Identify the specific inaccuracies, such as mixed files or outdated collections, that frequently trigger automatic loan denials for entrepreneurs.

- Understand the direct impact of credit repair on business funding and how a clean profile serves as the primary unlock for 0% interest capital.

- Recognize the risks associated with automated online dispute portals, which can sometimes lead to waiving your legal rights under the FCRA.

- Learn a methodical approach to auditing all three major bureaus while gathering the irrefutable evidence needed to bypass automated verification loops.

- Discover how to transition from basic error removal to a success-based strategy that integrates credit restoration with strategic capital procurement.

The Financial Impact of Credit Report Errors on Your Business Goals

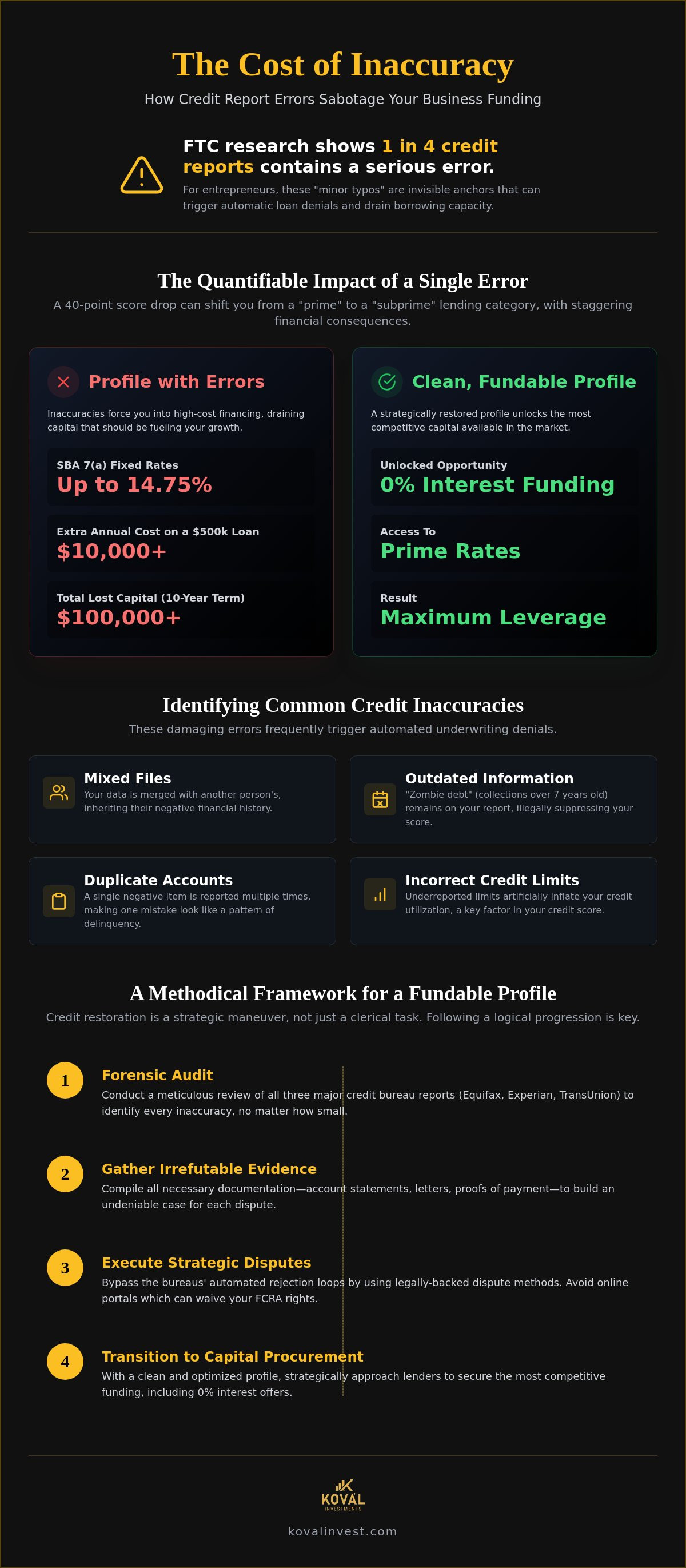

A credit report error is technically defined as any information on your profile that is inaccurate, incomplete, or unverifiable. While this sounds like a minor administrative hurdle, the reality is far more consequential for your bottom line. Research from the Federal Trade Commission has historically shown that one in four credit reports contains a serious error that could trigger an automatic loan denial. For an entrepreneur, these errors act as invisible anchors that drag down your borrowing capacity and limit your operational agility. The Fair Credit Reporting Act (FCRA) provides you the legal right to challenge these inaccuracies, yet many owners leave their profiles unmonitored until a denial letter arrives.

The impact of credit repair on business funding becomes quantifiable when you look at interest rate tiers. A single erroneous late payment or a "mixed file" can cause a 40-point drop in your credit score. In the current July 2026 lending environment, where SBA 7(a) fixed rates can reach as high as 14.75%, that drop might move you from a "prime" category to a "subprime" one. On a $500,000 loan, even a two percent increase in your interest rate results in an additional $10,000 in annual interest expenses. This is capital that should be reinvested in your team or technology, not lost to a data entry mistake at a credit bureau.

How Errors Block Access to Interest-Free Capital

Lenders offering 0% interest business funding operate with razor-thin margins and have zero tolerance for risk. Their underwriting algorithms are designed to filter out any profile with charge-offs, collections, or recent late payments. If your report contains an error that mimics these red flags, you'll likely face an automatic decline before a human underwriter ever reviews your file. These algorithms don't account for "explanations" or "context"; they simply process the data provided. Cleaning your report isn't just about fixing the past; it's a strategic investment in your future borrowing capacity.

The ROI of a Clean Credit Profile

Consider the lifetime cost of a $500,000 SBA loan over a ten-year term. The difference between a clean profile and one marred by errors can easily exceed $100,000 in total interest payments. When you engage in SBA loan assistance, the first step is often ensuring your credit reflects your true financial behavior. Credit optimization establishes a stable financial foundation that allows you to leverage alternative business funding solutions with confidence and precision. Beyond the math, there's a significant psychological benefit. You can approach investors and lenders with the certainty that your profile represents your business's true strength, removing the anxiety of a potential surprise denial during the due diligence phase.

Identifying Common Inaccuracies That Drain Your Borrowing Power

Identifying errors requires more than a casual glance at your credit score; it demands a forensic analysis of the data points that lenders use to judge your reliability. One of the most damaging issues is the "mixed file" phenomenon. This occurs when a credit bureau merges your financial data with that of another individual who shares a similar name or geographical history. If that person has a history of defaults, those liabilities appear on your report, instantly tanking your score. Understanding the impact of credit repair on business funding begins with recognizing that these clerical overlaps are common and often go unnoticed until a funding application is denied.

Duplicate accounts and outdated information also create significant drag on your profile. It's common for a single negative item, like a medical bill or a utility collection, to be sold to multiple debt buyers. Each buyer may report the item as a new entry, making one mistake look like a pattern of delinquency. Additionally, federal law generally requires that late payments and collections age off your report after seven years. If a bureau fails to purge this "zombie debt," your profile remains artificially suppressed. For business owners, incorrect credit limits are particularly toxic. Many business credit cards report balances but fail to report the actual credit limit. This makes you look 100% leveraged to an automated underwriting system, even if you're only using a fraction of your available capital.

Account Status and Payment History Errors

Inaccuracies often hide in the status of your accounts. You might find closed accounts still listed as open, which can negatively affect your debt-to-income ratio. Worse yet, some debt buyers engage in "re-aging," where they change the date of the last activity on an old debt to illegally extend its life on your report. When you attempt to dispute an error on your credit report, you're fighting these systemic inaccuracies that directly hinder your growth. If you're unsure which errors are hurting your profile most, a strategic credit audit can provide the clarity needed to proceed.

Identity and Clerical Mistakes

Clerical mistakes at the bureau level can lead to data leaks between your personal and business profiles. Incorrect Social Security Numbers or Employer Identification Numbers (EIN) can cause accounts to be misattributed to your business. We also frequently see public records that haven't been updated. A satisfied tax lien or a dismissed bankruptcy might still show as "active" or "unpaid" on your report. These errors signal a high level of risk to lenders, regardless of your actual cash flow or business performance. Correcting these identity-based mistakes is a fundamental step in ensuring the impact of credit repair on business funding is both positive and permanent.

DIY Dispute Process vs. Professional Financial Optimization

Many entrepreneurs assume that correcting a credit report is a simple administrative task they can handle on a Saturday afternoon. While the Federal Trade Commission provides resources to correct mistakes in your credit report, the reality for high-stakes business owners is far more complex. The DIY approach often leads to a cycle of automated rejections because bureaus prioritize efficiency over accuracy. When you use a bureau's online portal, you aren't just submitting a claim. You're often agreeing to fine-print terms that waive your right to future legal action under the FCRA. This loss of leverage can be devastating if the bureau refuses to correct a legitimate error that's blocking your access to capital.

The true impact of credit repair on business funding is realized when the process moves from reactive to proactive. A professional approach treats your credit profile as a strategic asset rather than a list of numbers. This shift in perspective is what separates a business that barely qualifies for high-interest loans from one that commands 0% interest capital. It's about moving beyond clerical fixes to a state of total financial readiness.

The Pitfalls of the DIY Approach

Bureaus use sophisticated algorithms to flag dispute letters. If a letter looks like a generic template or lacks specific legal phrasing, it's often labeled as "frivolous" and ignored. This is the "frivolous trap," and it can stall your progress for months. Beyond the risk of rejection, there's a heavy time cost. A CEO shouldn't spend 20 hours a month fighting an automated verification loop. Every hour spent on administrative disputes is an hour taken away from scaling operations or securing new clients. Amateur disputes also lack the professional leverage required to force a bureau to perform a manual review, which is often necessary for complex errors like mixed files.

Why Strategic Advisory Wins

This is where professional business credit repair services offer a distinct advantage. These services utilize the "Reasonable Investigation" standard to force compliance from both bureaus and furnishers. They don't just send letters; they build a comprehensive case based on federal law. A strategic partner provides holistic optimization, fixing existing errors while simultaneously building a roadmap for capital procurement. This success-based philosophy ensures that your advisor is equally invested in your funding outcome. It transforms credit repair into a collaborative venture that reduces your financial risk and accelerates your path to premium funding solutions.

A Strategic Step-by-Step Guide to Removing Credit Inaccuracies

Correcting your credit profile is a methodical operation that requires precision and persistence. You must start by auditing all three major bureaus-Equifax, Experian, and TransUnion-to identify inconsistencies. If one bureau reports a late payment that the other two do not, you have documented evidence of a reporting error. This level of detail is vital because the impact of credit repair on business funding often hinges on these small, overlooked discrepancies. You aren't just looking for big mistakes; you're looking for any data point that doesn't align across all three platforms.

Once you've identified the errors, you must gather irrefutable evidence. This includes bank statements, cancelled checks, or court documents that prove the current reporting is false. You're proving the bureau's data is wrong with physical documentation. Your dispute letter should never be a general complaint. Instead, it must cite specific violations of the Fair Credit Reporting Act (FCRA). Specifically, you should hold the bureau to the "Reasonable Investigation" standard. This legal requirement forces the bureau to do more than just use an automated system to "verify" the debt with the creditor.

Always send your correspondence via Certified Mail with a return receipt requested. This creates a legal paper trail that holds the bureau accountable to the 30-day investigation timeline. If the bureau responds by claiming the item is verified without providing proof, use the Method of Verification (MOV) demand. Under the FCRA, you have the right to know exactly how they verified the data, the name of the person they contacted, and the specific documents used in the investigation. Most bureaus struggle to provide this level of detail, which often leads to the permanent removal of the item.

Auditing for Success

Spotting cross-bureau discrepancies is the fastest way to prove an error is illegitimate. It's equally important to check the data furnisher, which is the original bank or creditor that provided the information to the bureau. If the bank's internal records don't match the bureau's report, you've found the source of the conflict. This level of scrutiny is essential because using working capital for business acquisition requires a perfectly audited report to ensure your leverage remains intact during the underwriting process.

The Follow-Up Strategy

Bureaus often respond with a generic form letter designed to discourage further action. Don't accept this as a final answer. If a bureau ignores the law or fails to investigate properly, you can escalate the matter to the Consumer Financial Protection Bureau (CFPB). When a bureau remains stubborn despite your evidence, it's often time to involve a professional advisor who can break the deadlock. If you're ready to move beyond automated rejections, you can partner with a strategic advisor to review your profile and build a path toward 0% interest capital.

From Error Removal to 0% Interest Funding: The Koval Path

Removing a collection or correcting a mixed file is a significant win, but it's only 50% of the battle for high-limit capital. A clean report is the foundation, yet the true impact of credit repair on business funding is measured by the actual dollars deposited into your account. Many owners stop once their score improves, missing the opportunity to leverage that new credibility into low-cost capital. At Koval Investments, we recognize that credit restoration is a means to an end, not the end itself. Our approach integrates forensic credit cleaning with a sophisticated capital procurement strategy.

We operate on a success-based philosophy, which means our goals are perfectly aligned with yours. We don't view ourselves as a distant service provider; we're a strategic partner invested in your expansion. This collaborative model reduces your financial risk and ensures that every dispute we file is designed to satisfy the specific underwriting requirements of top-tier lenders. Once your report is optimized, we move immediately into a 0% interest business funding strategy that prioritizes your cash flow and long-term stability.

The Bridge to Capital

A clean report allows for the strategic sequencing of credit applications, a process that most DIY attempts completely ignore. We understand the internal thresholds of major lenders and the specific algorithms used for SBA loan approvals. By timing your applications and selecting the right mix of lenders, we can maximize your total funding amount while keeping your interest rates at 0% for as long as possible. A partner who understands both the nuances of credit law and the current appetite of banking institutions is the difference between a small line of credit and the significant capital needed for major acquisitions or equipment purchases.

Partnering for Long-Term Expansion

Our relationship doesn't end once the errors are gone. We provide the strategic planning necessary for your next phase of corporate growth, whether that involves real estate investment or mergers and acquisitions. You gain an "insider" advantage by accessing capital sources and lending programs that aren't typically advertised to the general public. We help you navigate the complex financial landscape with a steady hand, ensuring your business remains fundable as you scale. If you're ready to stop fighting bureaus and start securing capital, optimize your profile and secure 0% interest funding with Koval Investments today.

Maximizing Your Borrowing Power for 2026

Your credit profile should function as a strategic asset rather than a source of frustration. By moving beyond the clerical task of error removal and toward a methodical capital plan, you position your company to lead in a competitive market. The long-term impact of credit repair on business funding is measured in the thousands of dollars saved through lower interest rates and the expansion opportunities created by interest-free capital. It's about ensuring that every data point on your report accurately reflects your true financial reliability.

We invite you to experience a different kind of financial partnership. Koval Investments provides a collaborative, low-pressure advisory focused entirely on your success. Our success-based philosophy ensures that our expertise in SBA and 0% interest capital is fully dedicated to your growth; we only win when you get funded. It's time to stop managing mistakes and start securing the resources your vision requires. Let's build a fundable future together.

Secure your 0% interest funding by optimizing your credit with Koval Investments

Frequently Asked Questions

How long does it actually take to remove an error from a credit report?

Credit bureaus generally have 30 days to investigate a dispute according to federal law. This timeline can extend to 45 days if the dispute is filed after you receive a free annual credit report. Once the investigation is complete, the bureau must notify you of the results within five business days. While the legal window is clear, the actual impact of credit repair on business funding may take an additional billing cycle to manifest as lenders update their internal records.

Can I remove a verified error if it is still inaccurate?

Yes, you have the right to continue challenging an item even if the bureau claims it has been "verified." Verification often involves a simple automated check between the bureau and the creditor that fails to address the root of your dispute. You can demand the Method of Verification (MOV) to see exactly how the bureau confirmed the data. If they cannot provide specific documentation or the name of the person they contacted, the item must be removed regardless of its previous status.

Will removing errors automatically increase my credit score?

Removing a negative error typically increases your credit score, though the exact point jump depends on your overall profile. If you remove a recent collection or a "mixed file" that wasn't yours, you'll likely see a substantial improvement. For business owners, the goal isn't just a higher score but a cleaner profile that meets the zero-tolerance thresholds of 0% interest lenders. Even a small score increase can move you into a better interest rate tier for SBA loans.

Is it better to dispute credit report errors online or by mail?

Disputing by mail is the most effective strategy for entrepreneurs who want to maintain their legal leverage. Online portals are designed for bureau efficiency and often force you to waive your right to future legal action under the FCRA. Sending a physical letter via Certified Mail creates a documented paper trail. This evidence is vital if you need to prove the bureau failed to meet its 30-day investigation deadline or ignored your submitted evidence.

What is the Reasonable Investigation standard under the FCRA?

The Reasonable Investigation standard requires bureaus to do more than just relay information from a creditor. They must actually review the evidence you provide, such as cancelled checks or bank statements, to determine if the reporting is accurate. If a bureau simply accepts a creditor's automated response without looking at your documentation, they haven't met this legal requirement. This standard is the primary tool used to force bureaus to correct complex clerical errors.

Does disputing an error hurt my credit score while the investigation is active?

Disputing an item does not lower your credit score while the investigation is ongoing. However, many lenders will not finalize a loan approval if they see an active dispute remark on your report. This can temporarily stall the impact of credit repair on business funding applications. It's often best to complete the dispute process and have the remarks removed before you begin a strategic sequencing of capital applications.

What happens if a credit bureau refuses to remove an obvious mistake?

If a bureau remains stubborn despite clear evidence, you should escalate the case to the Consumer Financial Protection Bureau (CFPB). Filing a formal complaint often triggers a more thorough manual review by the credit bureau's legal or compliance department. If the error persists after a CFPB complaint, you may need to involve a professional advisor. A strategic partner can identify technical legal violations that force a bureau to comply with the law.

Can a professional credit repair service remove legitimate negative items?

No service can legally remove accurate, timely, and verifiable negative information from your report. Professional credit repair focuses on identifying items that are inaccurate, incomplete, or cannot be proven by the creditor. It's common for "legitimate" negatives to be reported with the wrong date, an incorrect balance, or a missing credit limit. In these instances, the item is technically inaccurate and must be corrected or deleted to ensure your profile is fundable.