How to Build Business Credit for a New Company: A Strategic 2026 Funding Guide

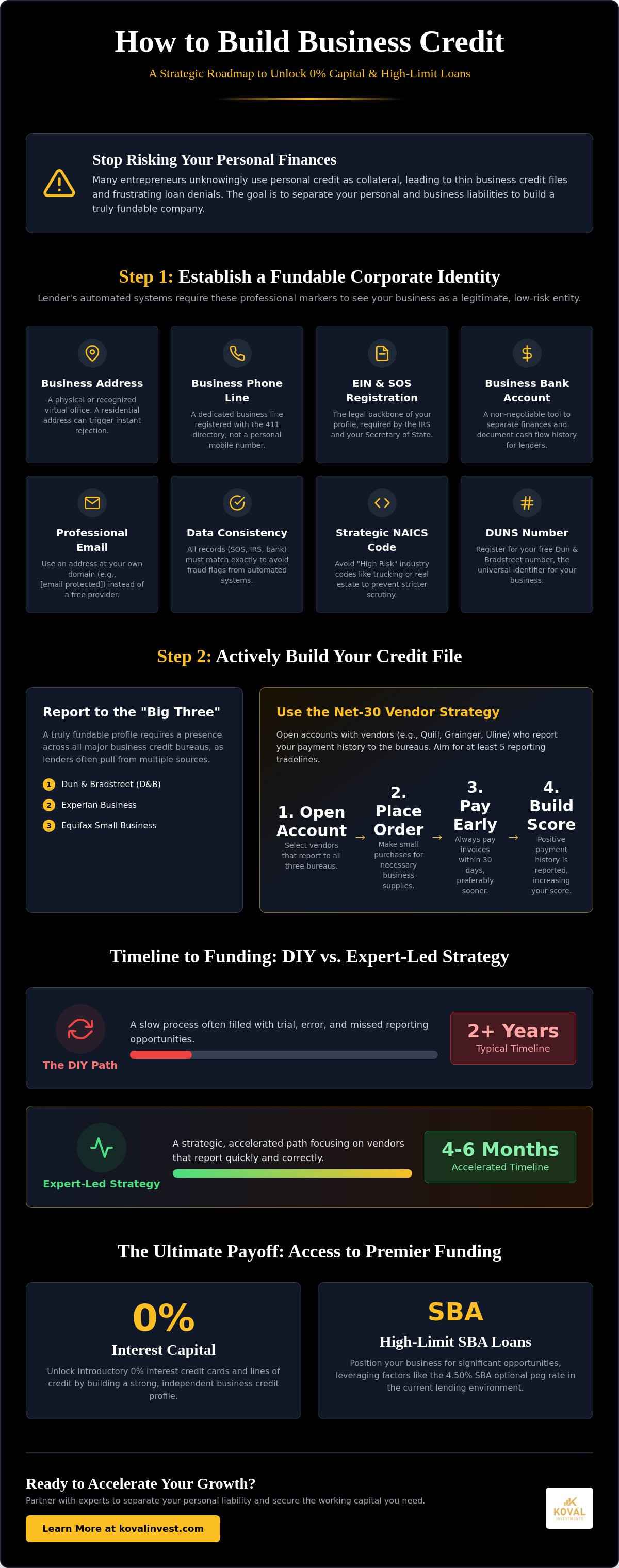

Your personal credit score shouldn't be the primary collateral for your company's growth, yet many entrepreneurs unknowingly risk their family's financial security while learning how to build business credit for a new company. It's a common trap that leads to thin credit files and frustrating loan denials just when you need capital the most. You likely understand that keeping your personal and business liabilities separate is the goal, but the path to getting there often feels obscured by conflicting advice about which vendors actually report to the bureaus.

This guide provides a clear, strategic roadmap to unlock 0% interest capital and high-limit SBA loans. We've designed this process to help you move beyond the limitations of personal guarantees and toward a fundable business profile. We'll walk through the essential steps to establish your corporate identity, choose the right net-30 vendors, and leverage the 2026 lending environment, where the SBA optional peg rate of 4.50% offers significant opportunities for businesses with the right credit positioning.

Key Takeaways

- Establishing a fundable identity is the prerequisite for credit, requiring professional markers like a dedicated business address and phone line to satisfy 2026 lender standards.

- Learn how to build business credit for a new company by utilizing the Net-30 strategy to seed initial reporting with D&B, Experian, and Equifax.

- Compare the traditional two-year DIY timeline against expert-led strategic restoration that can accelerate your path to capital in as little as four to six months.

- Understand how your personal credit profile acts as a temporary bridge to unlock high-limit SBA loans and 0% interest funding solutions.

- Discover how a success-based partnership can separate your personal liability from business expenses while securing the working capital needed for growth.

The Foundation: Establishing a Fundable Corporate Identity

A fundable corporate identity is much more than a legal formality; it's the specific set of data points that tell a lender's automated system your business is a legitimate, low-risk entity. When you're learning how to build business credit for a new company, you have to look beyond just filing paperwork. Lenders in 2026 rely heavily on digital verification. This means a residential address or a mobile phone number listed as your primary business contact can lead to an instant rejection. You need a physical office space or a recognized virtual office, paired with a dedicated business line that's registered with the 411 directory.

Your Employer Identification Number (EIN) and Secretary of State (SOS) registration form the legal backbone of your profile. However, the real verification happens at the bank. A dedicated business bank account is non-negotiable. It separates your personal life from your professional one and provides the documented cash flow history that lenders require for high-limit SBA loans. Without this clear separation, you'll struggle to prove that your company is a standalone entity capable of managing its own debt.

Lender Compliance: Beyond the Legal Minimums

Automated underwriting systems are designed to find reasons to say "no." To pass these checks, your professional presence must be consistent across every platform. This includes using a professional email address hosted on your own domain rather than a free provider. Every record at the SOS, IRS, and your bank must match exactly, down to the punctuation in your business name. Discrepancies often trigger fraud flags that halt applications. Additionally, your NAICS industry code matters. Categorizing your business under a "General" classification is often safer than "High Risk" labels like trucking or real estate, which can lead to stricter scrutiny and lower credit limits.

The Role of the DUNS Number and D&B Profile

A DUNS number acts as the Social Security Number for your business, allowing global lenders to track your financial reliability. While Dun & Bradstreet often suggests expensive "credit builder" packages, you can register for this number for free. Once your profile is active, it becomes part of the wider network of business credit reports that banks use to assess your risk. You should monitor this file closely to identify and fix business credit report errors early. Taking these foundational steps is the only way to master how to build business credit for a new company without getting stuck in the "thin file" trap.

Establishing Your Credit Profile: The Primary Reporting Agencies

Once your corporate identity is verified, you must actively feed data to the reporting agencies that determine your creditworthiness. While many founders focus exclusively on Dun & Bradstreet, a truly fundable profile requires a presence across the "Big Three" bureaus: D&B, Experian Business, and Equifax Small Business. Each bureau uses different scoring models, and lenders often pull from multiple sources before making a decision. Relying on just one score is a strategic error that can lead to unexpected denials when you apply for higher-tier capital.

The most effective method for how to build business credit for a new company is the "Net-30" strategy. This involves opening accounts with vendors that allow you to pay for goods or services within 30 days of the invoice date. These vendors act as your initial references. According to the U.S. Small Business Administration, maintaining a positive payment history with these partners is a core requirement for securing larger loans later. However, you must be vigilant. Many popular vendors do not report to all three bureaus, and some don't report at all. Always verify a vendor's reporting habits before placing an order, or you'll waste months waiting for a score that never appears.

Strategic Vendor Selection for New Companies

Starter vendors typically include office supply companies, shipping providers, or industrial equipment retailers like Quill, Grainger, or Uline. You should aim to establish at least five reporting trade lines to create a robust profile that looks mature to automated systems. Timing is everything. It usually takes three to six months of consistent activity to generate a usable PAYDEX score. To maximize this score, pay your invoices early. D&B's model specifically rewards businesses that settle debts before the due date, which can be the difference between a mediocre score and a top-tier rating.

Experian and Equifax: The Secret to Unsecured Funding

Experian and Equifax are the primary bureaus used by banks to evaluate applications for 0% interest business funding solutions. These reports often include more detailed financial data, such as credit card utilization and public records. You should check these reports regularly for inaccuracies, as even a minor clerical error can trigger an instant denial. By following strategic steps to improve your business credit profile, such as diversifying your credit mix with both vendor accounts and revolving lines, you position your company as a sophisticated borrower. If you're ready to accelerate this process, our strategic planning services can help you identify which reporting paths lead to the fastest capital access.

DIY Building vs. Expert Strategic Restoration: A Comparison

Choosing the path of least resistance often leads to the longest wait times. When founders research how to build business credit for a new company, they usually encounter a standard DIY checklist: get an EIN, open a bank account, and wait for net-30 vendors to report. While this process is technically sound, the timeline for a DIY approach usually spans 12 to 24 months before significant capital becomes accessible. In contrast, an expert-led strategic restoration can condense this window to just 4 to 6 months. This isn't about cutting corners; it's about knowing which specific levers to pull to satisfy lender underwriting criteria on the first attempt.

The Limitations of the DIY Checklist

Standard checklists provide a skeleton, but they lack the muscle required for complex funding scenarios. Most online templates used for disputes or credit building are easily recognized by automated bureau systems. This often triggers "frivolous" dispute flags, which can freeze your progress for months. Relying on professional credit repair for business owners offers a distinct advantage because it utilizes specific legal leverage under the Fair Credit Reporting Act (FCRA) that automated tools simply can't replicate. While the SBA guide to establishing business credit provides the necessary rules, it doesn't explain how to navigate the nuances of a rejected application or a stalled reporting line.

Evaluating Strategic Credit Repair Experts

There's a fundamental difference between a "dispute mill" and a strategic restorer. Dispute mills often charge recurring monthly fees to send out generic letters with no clear end date. A strategic restorer operates on a success-based model. This aligns the advisor's incentives with your specific funding goals. If you don't get the results needed for capital access, the partnership hasn't succeeded. This level of accountability is vital when you're looking for how to fix credit for SBA loan approval. Professional consultants bring insider knowledge regarding which lenders are currently active and which specific data points they prioritize in 2026. This expertise significantly increases the success rate of SBA loan approvals compared to founders who apply blindly using only a DIY profile. Mastering how to build business credit for a new company through this professional lens isn't just about the credit score; it's about the speed to funding and the ultimate return on your time.

Optimizing Your Profile for 0% Interest and SBA Funding

For a new entity, your personal credit history remains the most reliable predictor of future financial behavior in the eyes of lenders. While the ultimate goal of learning how to build business credit for a new company is to separate your personal and business liabilities, your personal FICO score acts as the essential bridge to initial capital. Banks rarely grant high-limit, unsecured lines to a company with zero years of tax returns without looking at the founder's track record. To unlock the most competitive 0% APR business credit card stacks, you generally need a personal FICO score of 720 or higher, with a clean history and no recent bankruptcies or late payments.

Your debt-to-credit ratio is equally critical. Even with a high score, having personal credit cards maxed out suggests a high risk of default to automated underwriting systems. High-limit approvals usually require personal utilization to be below 30%, though staying under 10% is the gold standard for 2026 funding. By optimizing these personal metrics, you can secure initial business lines using a "soft pull" on the business side, preventing an accumulation of hard inquiries that would otherwise lower your score and signal desperation to other lenders.

The Personal Guarantee (PG) Strategy

A personal guarantee is often the only way to jumpstart high-limit lines for a startup. When used strategically, a PG allows you to leverage your personal strength to build the business's independent profile. The path to PG-removal begins as your business credit file matures through the vendor reporting stages we discussed previously. Once your company demonstrates consistent revenue and a strong PAYDEX score, you can transition toward non-recourse funding. This transition is a core component of the SBA loan assistance we provide, ensuring you meet the specific 2026 metrics where lenders look for a balanced mix of personal reliability and business cash flow.

Advanced Optimization: Statement Snapshots and Timing

Maximizing your capital raise requires precise timing. One effective "insider" tactic is the statement date trick. By paying your balances in full a few days before the statement closing date, rather than the due date, you ensure that the bureau sees a 0% utilization snapshot. This allows you to apply for multiple lines in a short window while your scores are at their peak. Credit stacking is a strategic method for securing multiple 0% interest lines simultaneously to provide a massive pool of working capital. If you want to see how these pieces fit together for your specific situation, our 0% Interest Funding Solution provides the direct roadmap to high-limit access without the typical trial and error of DIY applications.

Partnering with Koval Investments for Accelerated Growth

Understanding how to build business credit for a new company is only the first step toward true financial independence. While the DIY methods discussed in this guide provide a solid foundation, many founders find that the gap between establishing a profile and actually securing high-limit capital is wider than expected. Koval Investments acts as your strategic partner, bridging this gap by providing the expertise and insider connections needed to move from a "thin file" to a fundable enterprise in months rather than years. We don't just offer advice; we provide a comprehensive framework that integrates Credit Repair Services with our proprietary 0% Interest Funding Solution.

Our firm operates on a success-based philosophy. We view our consulting as an investment in your company's long-term fundability rather than a traditional expense. This approach ensures that our objectives are perfectly aligned with yours. If you don't secure the capital required to scale, we haven't fulfilled our role as your advisor. This commitment to results is what allows us to navigate complex financial landscapes with calm reliability, providing a steady hand as you move through the critical stages of growth, from initial vendor lines to sophisticated SBA loans and working capital.

The Koval 'Win-Win' Funding Model

We minimize your financial risk by focusing on results-based milestones. This collaborative process extends beyond simple credit building. We offer a holistic view of your business's health, including:

- Strategic Planning: Aligning your credit profile with your specific industry goals.

- Business Valuations: Understanding the true worth of your company to better position you for M&A or exit strategies.

- Mergers and Acquisitions Consulting: Helping you leverage your established credit to acquire competitors or expand into new markets.

Having a seasoned partner ensures that you avoid the common pitfalls that lead to loan denials. We handle the technical nuances of lender compliance so you can focus on operational efficiency.

Next Steps: Securing Your 2026 Capital

The journey of how to build business credit for a new company concludes when your enterprise is fully scalable and decoupled from your personal assets. To reach this stage, you need a clear roadmap based on your current credit health. We prepare new companies specifically for the 2026 lending environment, where precision in your application data is the difference between a 4.50% SBA peg rate and high-interest alternative debt. Our team analyzes your current standing and identifies the fastest path to unsecured working capital. If you're ready to stop guessing and start growing, secure your success-based credit consultation with Koval Investments today.

Accelerate Your Path to Corporate Fundability

Establishing a fundable identity and seeding your profile with reporting vendors are the essential first steps in learning how to build business credit for a new company. However, the true competitive advantage lies in the strategic optimization of your profile to bridge the gap between a new entity and a scalable enterprise. By aligning your personal credit strength with business credit maturity, you unlock access to high-limit SBA loans and unsecured capital that remains separate from your personal assets.

Since 2018, Koval Investments has specialized in 0% interest capital procurement, offering a comprehensive advisory that spans credit repair, SBA navigation, and long-term strategic planning. Our success-based model ensures a true partnership where we only win when you successfully secure the funding your vision requires. You don't have to navigate the complexities of 2026's financial landscape alone. Unlock 0% interest funding for your new company with Koval Investments and take the next step toward a fundable future with the right strategic backing.

Frequently Asked Questions

How long does it take for a new company to build business credit?

It typically takes three to six months of consistent payment activity to establish an initial PAYDEX score with Dun & Bradstreet. While you can see movement in your file relatively quickly, building a comprehensive profile capable of securing high-limit SBA loans or unsecured working capital often requires six to twelve months of strategic reporting. The timeline depends heavily on how quickly your chosen vendors report your data to the major bureaus.

Can I build business credit for a new company without using my SSN?

You can establish a basic credit file using only your EIN, but most lenders require a personal guarantee for high-limit funding during the startup phase. Your personal credit acts as a bridge while the company is young. Once your business credit profile is mature and you've demonstrated strong annual revenue, you can transition to non-recourse funding solutions that don't rely on your SSN or personal assets as collateral.

What is the fastest way to get a business credit score for a new LLC?

The fastest way to generate a score is by opening Net-30 accounts with "starter vendors" that report to the bureaus immediately. By purchasing essential supplies and paying the invoices as soon as they are received, you can trigger an initial score within 90 days. This is a foundational step in how to build business credit for a new company because it provides the data points automated underwriting systems need to see.

Do I need a business bank account to build business credit?

A dedicated business bank account is mandatory for lender compliance and cash flow verification. Lenders in 2026 use your bank history to confirm that your company is a separate legal entity and can handle debt obligations. Without a business account, you cannot prove the financial separation required to protect your personal assets or qualify for competitive interest rates on professional lines of credit.

Which vendors report to business credit bureaus for new companies?

Common reporting vendors include Grainger, Quill, and Uline, which are known for offering Net-30 terms to new entities. These companies typically report your payment history to Dun & Bradstreet and Experian Business. It's vital to confirm a vendor's reporting status before ordering, as some only report negative data, which won't help you establish a positive score or build your profile's maturity.

Is it better to build business credit DIY or hire an expert?

DIY methods are suitable for basic setup, but hiring an expert can accelerate your path to funding by several months. Professional consultants understand the specific underwriting criteria of 2026 lenders and can help you avoid "thin file" rejections. If you need capital immediately, an expert-led strategy ensures your profile is optimized for high-limit approvals and 0% interest funding solutions from the start.

How does my personal credit score affect my new company's ability to get credit?

Your personal credit score is the primary metric lenders use to gauge risk before your company has a multi-year track record. A personal FICO score of 720 or higher is generally required to access the most competitive 0% interest capital stacks. Your personal history serves as the initial evidence of your financial reliability, making it a critical component of how to build business credit for a new company.

What is a good business credit score for a new company in 2026?

A PAYDEX score of 80 or higher is the standard benchmark for a healthy business credit profile. For Experian Business and Equifax Small Business, you should aim for scores above 75 to demonstrate low risk to potential creditors. These scores indicate that your company pays its bills on or before the due date, which is the most important factor for securing long-term working capital and SBA loans.